Bullish Portfolio

Bullish Portfolio

Introduction to Tax-Advantaged Compounding

Aspiring millionaires know that consistent investing alone is not enough. The real accelerator lies in tax-advantaged accounts that let your money grow without the drag of annual taxes. In 2026, vehicles like Roth IRAs, traditional 401(k)s, and Health Savings Accounts (HSAs) remain powerful tools for achieving financial independence (FI). This guide explores how these accounts turbocharge compounding returns while helping you avoid common pitfalls.

How Tax Shelters Supercharge Growth

Taxes erode returns in taxable brokerage accounts. In contrast, tax-advantaged accounts defer or eliminate taxes on gains, dividends, and interest. This means every dollar stays invested longer, creating exponential growth over decades. For example, $10,000 invested annually at an 8% average annual return in a tax-sheltered account can exceed $1 million by 2056, assuming consistent contributions and no withdrawals.

Roth IRA: Tax-Free Growth and Withdrawals

The Roth IRA allows after-tax contributions with completely tax-free qualified withdrawals in retirement. Eligibility depends on modified adjusted gross income limits, but backdoor Roth strategies remain available for high earners. Contribution limits for 2026 follow inflation adjustments announced by the IRS.

Traditional 401(k) and Employer Matches

Traditional 401(k)s provide immediate tax deductions on contributions. Always maximize employer matching—it's free money that compounds tax-deferred. Many plans now offer Roth 401(k) options too. Vesting schedules and early withdrawal penalties require careful planning.

HSAs: The Triple Tax-Advantaged Account

Health Savings Accounts offer unmatched benefits: tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. After age 65, funds can be used for any purpose without penalty (though non-medical withdrawals are taxable). This makes HSAs ideal for long-term compounding.

Step-by-Step Contribution Strategies for 2026

- Maximize employer 401(k) match first.

- Fund an HSA if eligible for high-deductible health plan coverage.

- Contribute to a Roth IRA up to annual limits.

- Consider backdoor Roth conversions for excess income.

- Automate contributions to maintain consistency.

Real-World Compounding Example

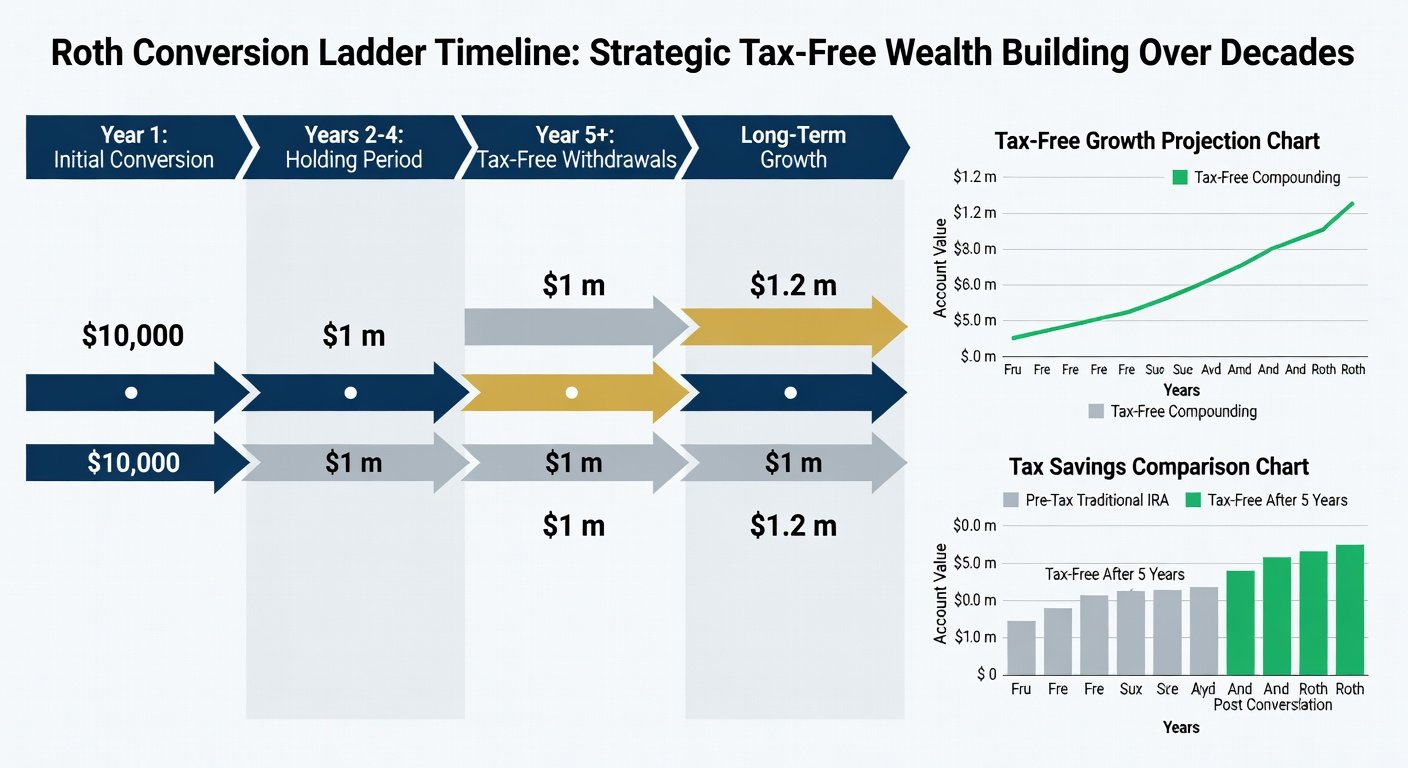

Imagine contributing $10,000 annually starting in 2026 at an 8% return. By 2056, the account balance surpasses $1.2 million entirely due to compounding within tax shelters. This illustrates the FI accelerator effect when taxes are removed from the equation.

Account Comparison: Pros, Cons, and Eligibility

- Roth IRA: Tax-free growth, income limits apply, flexible for heirs.

- 401(k): High contribution limits, employer match, required minimum distributions apply.

- HSA: Triple tax advantage, investment options vary by provider.

Roth Conversion Ladders and Early Access

For early retirees, Roth conversion ladders provide penalty-free access to converted funds after five years. This strategy bridges the gap before traditional retirement age while managing tax brackets.

Penalty Pitfalls to Avoid

Early withdrawals before 59½ typically incur 10% penalties plus taxes. Exceptions exist for first-time homebuyers, education, and medical expenses. Always consult IRS Publication 590 for current rules.

Interactive Calculator Tool Prompt

Use an online compound interest calculator with tax-sheltered options enabled. Input your annual contribution, expected return rate, and time horizon to project FI milestones.

Frequently Asked Questions

Can I access funds before retirement?

Yes, through Roth conversion ladders or HSA medical expense rules, with proper planning.

What are the 2026 contribution limits?

Limits are indexed for inflation; check the latest IRS announcements for exact figures.

Are there income restrictions?

Roth IRAs have phase-outs, but strategies like mega backdoor Roths expand access.

Conclusion

Tax-advantaged compounding remains the cornerstone of accelerated wealth building in 2026. By strategically using Roth IRAs, 401(k)s, and HSAs, you can reach millionaire status on the path to financial independence with greater efficiency. Start today, stay consistent, and let compounding do the heavy lifting.

For official guidance, visit IRS.gov and SEC.gov.

No comments yet. Be the first!