Bullish Portfolio

Bullish Portfolio

Introduction to 2026 Retirement Planning

Retirement planning in 2026 requires a structured, repeatable approach rather than scattered tactics. This checklist centers on Roth IRA and 401k accounts to help investors coordinate contributions, review asset allocation, manage taxes, and measure progress against long-term goals. Whether you are early in your career or nearing retirement, following an organized process builds confidence and reduces costly mistakes. Many individuals struggle with knowing exactly when to review accounts or how to adjust strategies as income changes, which is why a comprehensive annual framework proves invaluable.

Readers searching for this topic want actionable steps they can repeat each year. The guidance below includes contribution timing strategies, annual reviews, and a printable 12-month checklist. It also features three real-world investor scenarios and answers common questions about contribution errors. By breaking the process into monthly actions, investors gain clarity on everything from maximizing employer matches to rebalancing portfolios after market shifts.

Implementing this checklist consistently helps create a sustainable retirement savings habit. It emphasizes coordination between tax-advantaged accounts while accounting for life changes that may affect eligibility or contribution capacity. The result is a clearer path toward financial independence.

Understanding Roth IRA and 401k Basics for 2026

Roth IRAs offer tax-free growth and qualified withdrawals, while traditional 401k accounts provide upfront tax deductions. Many investors benefit from using both vehicles strategically. Coordination between the two accounts helps manage current and future tax brackets effectively. For instance, younger workers with lower current tax rates often prioritize Roth contributions, whereas those in peak earning years may lean toward traditional 401k deferrals to reduce taxable income now.

Key decisions include deciding how much to contribute to each account type and when to make those contributions throughout the year. Regular reviews ensure your choices align with evolving income, tax laws, and retirement timelines. Understanding the differences also involves knowing income limits for direct Roth IRA contributions and the availability of backdoor strategies for higher earners.

Contribution Timing and Annual Limits

Timing contributions can impact compounding and cash flow. Spreading contributions across the year rather than making a single lump-sum deposit often reduces market timing risk. Investors should also consider employer matching deadlines in their 401k plans. For example, contributing evenly each month allows dollar-cost averaging, which can smooth out volatility compared to waiting until December.

Always verify current IRS guidelines for contribution rules and eligibility. The IRS website provides official resources on retirement account limits and deadlines. Additionally, the Department of Labor offers guidance on 401k plan features such as automatic enrollment and matching formulas that can influence timing decisions.

Monthly Versus Lump-Sum Approaches

Monthly contributions suit those with steady paychecks, while lump sums work well after bonuses or tax refunds. Both methods have merits, but the key is consistency to avoid missing contribution windows.

Asset Allocation Reviews

Annual allocation reviews help maintain appropriate risk levels as you age or as market conditions shift. Rebalancing may involve adjusting stock, bond, and international holdings within both Roth IRA and 401k accounts. A common strategy is the glide path approach, where equity exposure gradually decreases closer to retirement.

Consider your time horizon and risk tolerance when making changes. Many investors use target-date funds or low-cost index funds to simplify allocation decisions while staying diversified. Documenting your target allocation percentages and reviewing them quarterly prevents drift caused by market gains in one asset class.

Tax-Year Coordination Strategies

Aligning contributions with tax years maximizes benefits. For example, front-loading contributions early in the year can accelerate tax-free growth in a Roth IRA. Backdoor Roth strategies may also apply for high earners, subject to IRS rules. Tracking your modified adjusted gross income helps determine eligibility and prevents over-contribution issues.

Coordinate traditional 401k contributions with expected taxable income to optimize deductions. Review withholding throughout the year to avoid surprises at tax time. Integrating these steps with estimated tax payments ensures smoother cash flow management.

Performance Benchmarking Against Retirement Goals

Compare portfolio growth to specific retirement income targets rather than broad market indexes alone. Track metrics such as projected annual withdrawal amounts and savings rate progress. Setting measurable milestones, like reaching a certain multiple of salary saved by age 40, provides motivation and direction.

Use online retirement calculators from reputable sources like the Social Security Administration to model different scenarios and adjust plans accordingly. Review historical performance data alongside forward-looking assumptions about inflation and returns to refine expectations.

Printable 12-Month Retirement Planning Checklist

- January: Review prior-year contribution room and make catch-up contributions if eligible. Update any automatic transfers.

- February: Confirm employer 401k match and adjust contribution percentage. Calculate how close you are to the annual maximum.

- March: Rebalance Roth IRA asset allocation based on market movements. Review fund expense ratios.

- April: File taxes and decide on any IRA contribution deadline actions. Consider converting traditional IRA funds if appropriate.

- May: Evaluate investment performance and benchmark progress against your retirement income target.

- June: Review beneficiary designations on all accounts. Update for any family changes.

- July: Assess tax withholding and adjust 401k contributions if needed. Check for plan amendments.

- August: Research any new retirement plan options at work. Explore rollover possibilities if changing jobs.

- September: Increase contributions if cash flow allows. Revisit emergency fund levels to protect retirement savings.

- October: Review healthcare costs and long-term care planning. Adjust HSA contributions if paired with high-deductible insurance.

- November: Perform year-end tax projection and plan final contributions. Meet with a tax advisor if complex situations exist.

- December: Maximize remaining contribution room before year-end deadlines. Finalize any charitable giving strategies tied to retirement accounts.

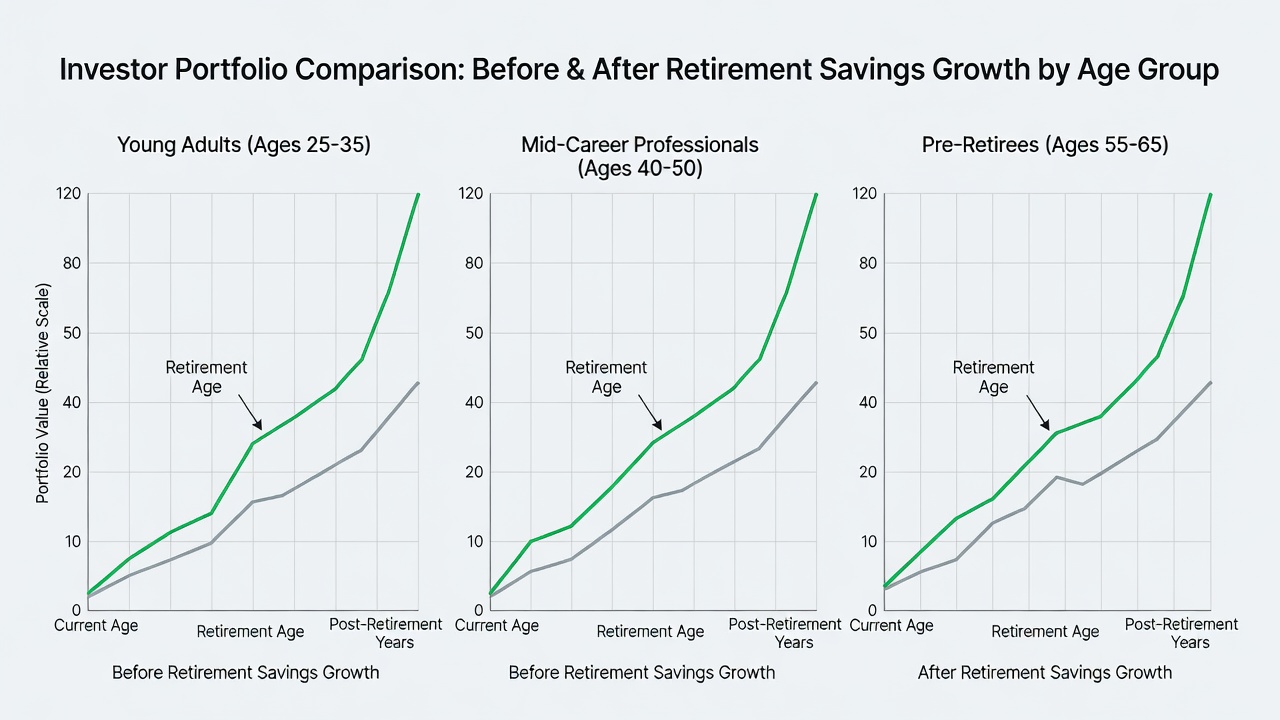

Three Real-World Investor Scenarios

Scenario 1: Mid-career professional. Before implementing the checklist, contributions were sporadic and allocation was overly aggressive. After following the 12-month process for two years, the investor increased total retirement savings by 35% and reduced volatility through rebalancing. Regular monthly reviews also helped capture additional employer match dollars that had previously been left on the table.

Scenario 2: High-income earner nearing 50. Previously missed catch-up contributions. Using the checklist, the investor began systematic Roth IRA contributions and coordinated 401k deferrals, resulting in a projected 22% higher retirement income stream. The structured approach also clarified when to use mega backdoor Roth options within the plan.

Scenario 3: Recent college graduate. Started with minimal knowledge. The structured monthly checklist helped establish consistent 401k contributions and an initial Roth IRA, building a foundation that projects to compound significantly over 30 years. Early automation of transfers reduced the temptation to skip months during tight cash-flow periods.

Common Mistakes to Avoid

- Ignoring required minimum distributions timing once retirement begins.

- Failing to update beneficiaries after major life events such as divorce or remarriage.

- Overlooking plan loan rules that can disrupt long-term compounding.

- Not coordinating spousal IRA contributions when one partner has low or no earned income.

Short FAQ: Common Contribution Errors

Q: What happens if I exceed annual limits? Excess contributions may incur penalties unless corrected by the IRS deadline. File Form 5329 to request a waiver if the error was unintentional.

Q: Can I contribute to both a Roth IRA and 401k in the same year? Yes, subject to separate eligibility and income rules for each account. The limits are independent.

Q: How do I fix a missed employer match? Increase future contributions and confirm the plan allows true-up contributions at year-end. Many plans true up automatically if you reach the match threshold later in the year.

Updating the Checklist for Life Events

Major life changes such as marriage, job transitions, or inheritance require checklist adjustments. Review contribution amounts, beneficiary forms, and asset allocation whenever income or family circumstances shift. Revisit the full process at least annually or after any significant event to keep your retirement plan on track.

Consistent use of this 2026 retirement planning checklist supports steady progress toward financial security through disciplined Roth IRA and 401k management. Adjust the monthly actions as needed while preserving the overall structure for repeatable success.

No comments yet. Be the first!