Bullish Portfolio

Bullish Portfolio

Introduction to Joint Retirement Planning in 2026

Married couples and partners face unique opportunities when coordinating retirement accounts like Roth IRAs and 401(k)s. Effective planning allows households to maximize tax-advantaged growth while managing combined tax brackets and eligibility rules. This guide explores practical tactics for 2026, focusing on long-term tax-free income and balanced risk. Understanding how these accounts interact helps couples avoid common mistakes and build a resilient financial future together. With evolving tax laws and changing life circumstances, proactive coordination becomes essential for achieving secure retirements that support both partners equally.

Core Rules for Roth IRAs and 401(k)s in Couples

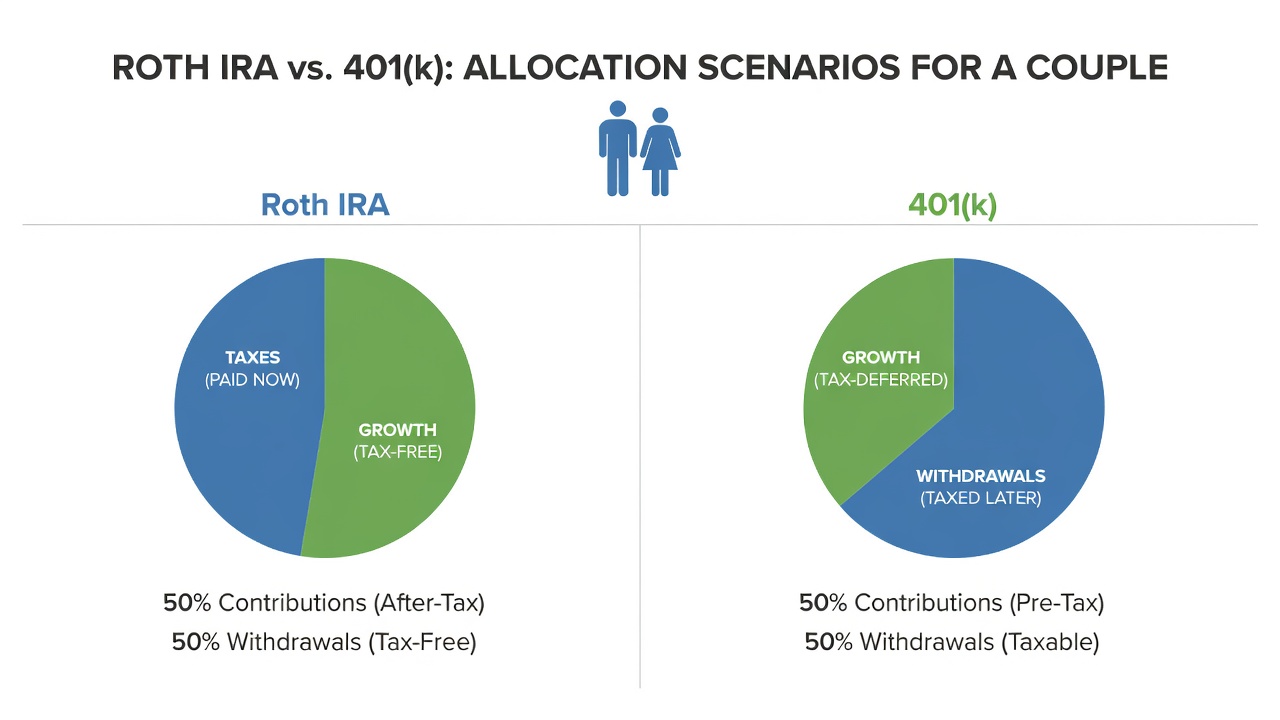

Roth IRAs offer tax-free withdrawals in retirement, while traditional 401(k)s provide upfront tax deductions. For couples, eligibility depends on modified adjusted gross income and filing status. Spousal IRA contributions enable non-working partners to build retirement savings based on the working spouse's earned income. These rules create flexibility but require careful coordination to prevent over-contribution or missed opportunities for tax efficiency. Couples must also consider how contribution limits interact when one or both partners have access to employer-sponsored plans, ensuring they do not exceed annual caps while still maximizing available tax benefits.

Income Splitting Tactics and Spousal IRA Eligibility

Income splitting helps balance contributions across partners. One effective approach involves directing earned income to the lower-earning spouse where possible to stay within favorable tax brackets. Spousal IRA rules permit contributions even if one partner has little or no earned income, provided the couple files jointly and meets overall income thresholds. Couples should review W-2 forms and self-employment income annually to identify optimal splitting points that support both accounts without triggering additional taxes. For example, a household with one high earner and one part-time worker can shift bonuses or consulting income to equalize contributions and preserve eligibility for Roth strategies.

Maximizing Combined Contribution Limits

Couples should aim to fill both partners' accounts strategically. Prioritize accounts with employer matches first, then layer additional savings into IRAs. This layered approach supports diversified tax treatment between pre-tax and after-tax dollars. Tracking contributions throughout the year prevents last-minute scrambles and ensures the household captures every available tax advantage. Regular monitoring also allows adjustments when one partner changes jobs or experiences income fluctuations that affect contribution room.

Prioritizing High-Earner 401(k) Matches

When one partner has access to a generous employer match, direct contributions there before funding IRAs. This captures free money that accelerates overall portfolio growth without additional out-of-pocket cost. Couples can model different contribution percentages to see how the match compounds over decades, often revealing that even modest increases in participation deliver outsized results. In practice, this means calculating the effective return from the match and comparing it against potential Roth growth to determine the optimal sequence of funding.

Handling Mismatched Employer Plans

Different employers often provide varying plan features. Couples should compare vesting schedules, investment options, and loan provisions. In some cases, rolling over older 401(k)s into an IRA can simplify management and open backdoor Roth pathways. Regular plan reviews, ideally each spring, help identify when a rollover makes sense or when staying inside the employer plan preserves unique benefits such as creditor protection. When plans differ significantly in fees or investment menus, the couple may decide to consolidate accounts to reduce administrative complexity and improve oversight of overall asset allocation.

Legal Backdoor Roth Options for High Earners

High-income couples may use backdoor Roth contributions by making non-deductible traditional IRA contributions followed by conversions. This strategy remains fully legal when executed properly and documented with IRS Form 8606. Always coordinate timing to minimize pro-rata taxation on existing pre-tax IRA balances. Working with a tax advisor ensures the conversion ladder aligns with projected future income and required minimum distribution schedules. Timing conversions during lower-income years, such as after a career transition, can further reduce tax impact and enhance long-term tax-free growth potential.

Sample Household Scenarios

Consider a dual-income household where one partner earns significantly more. Allocate the maximum possible to the higher earner's 401(k) to capture the match, then split IRA contributions to balance future tax brackets. Another scenario involves one self-employed partner using a solo 401(k) alongside the other's employer plan for additional flexibility. A third example features a couple nearing retirement who gradually shifts new savings toward Roth accounts to create tax-free withdrawal buckets that complement Social Security and pension income. In each case, running detailed projections helps the couple visualize how different contribution mixes affect after-tax retirement income and risk exposure.

Comparison Table of Allocation Scenarios

| Scenario | Primary Focus | Tax Benefit | Risk Level |

|---|---|---|---|

| Match-First Strategy | 401(k) with match | Immediate return | Low |

| Balanced Roth Split | Equal IRA contributions | Tax-free growth | Medium |

| Backdoor Conversion | High earner focus | Future tax-free | Medium-High |

| Hybrid Pre-Tax and Roth | Mixed account types | Tax diversification | Medium |

Common Pitfalls and RMD Timing for Couples

- Ignoring required minimum distributions can trigger unnecessary taxes after age 73.

- Failing to coordinate conversions may push the couple into higher brackets.

- Overlooking beneficiary designations can lead to unintended tax consequences for heirs.

- Not accounting for state tax rules on retirement distributions can reduce net income.

- Delaying spousal IRA contributions past the tax filing deadline limits compounding time.

Practical Steps for Annual Planning

Begin each year by projecting combined household income and estimating tax brackets. Next, list all available retirement accounts and their contribution deadlines. Then model three allocation scenarios using the comparison table above. Finally, schedule a mid-year check-in to adjust for changes in employment or tax law. These steps keep the plan dynamic and responsive to life events such as job changes, inheritances, or health-related expenses that could alter contribution capacity.

Risk Management and Asset Allocation Considerations

Beyond contributions, couples should align investment choices across accounts to maintain an overall risk profile suitable for their time horizon. This may involve placing more aggressive growth assets in Roth accounts for tax-free compounding while using traditional accounts for steadier income generation. Rebalancing annually ensures the portfolio remains aligned with joint retirement goals and changing market conditions.

Frequently Asked Questions

How do RMDs affect surviving spouses?

Spouses often have options to treat inherited accounts as their own, delaying or reducing distributions.

Can both partners contribute to Roth IRAs simultaneously?

Yes, provided the household meets income requirements and has sufficient earned income.

What happens if employer plans differ greatly?

Review each plan's fees and options annually and consider partial rollovers when advantageous.

Are there limits on backdoor Roth conversions for couples?

No annual dollar limit exists on conversions, but pro-rata rules and future tax rates must be evaluated carefully.

Conclusion

Coordinated 2026 retirement planning empowers couples to build substantial tax-advantaged wealth. By focusing on matches, spousal rules, and strategic conversions, partners can achieve balanced growth and minimize future tax burdens. Regular reviews and professional guidance help adapt the plan as circumstances evolve. For official guidance, visit IRS.gov, SSA.gov, and DOL.gov.

No comments yet. Be the first!