Bullish Portfolio

Bullish Portfolio

Introduction to the Compounding Clash

In the race toward financial independence (FI) by 2026, investors face a pivotal choice: stocks or real estate? Both asset classes harness the power of compounding—where returns generate more returns over time—but they differ vastly in risk, liquidity, leverage, and growth potential. With market volatility, rising interest rates, and economic shifts on the horizon, this comparison dives deep into projected 2026 returns, historical performance adjusted for future trends, pros and cons, entry strategies, real-world examples, risks, and diversification. Whether you're a beginner saver or seasoned portfolio builder, understanding these dynamics can supercharge your path to FI, where passive income covers living expenses.

Financial independence isn't just about accumulation; it's about sustainable growth. Stocks offer broad market exposure via indexes like the S&P 500, while real estate provides rental income and appreciation. But which wins for compounding by 2026? Let's break it down.

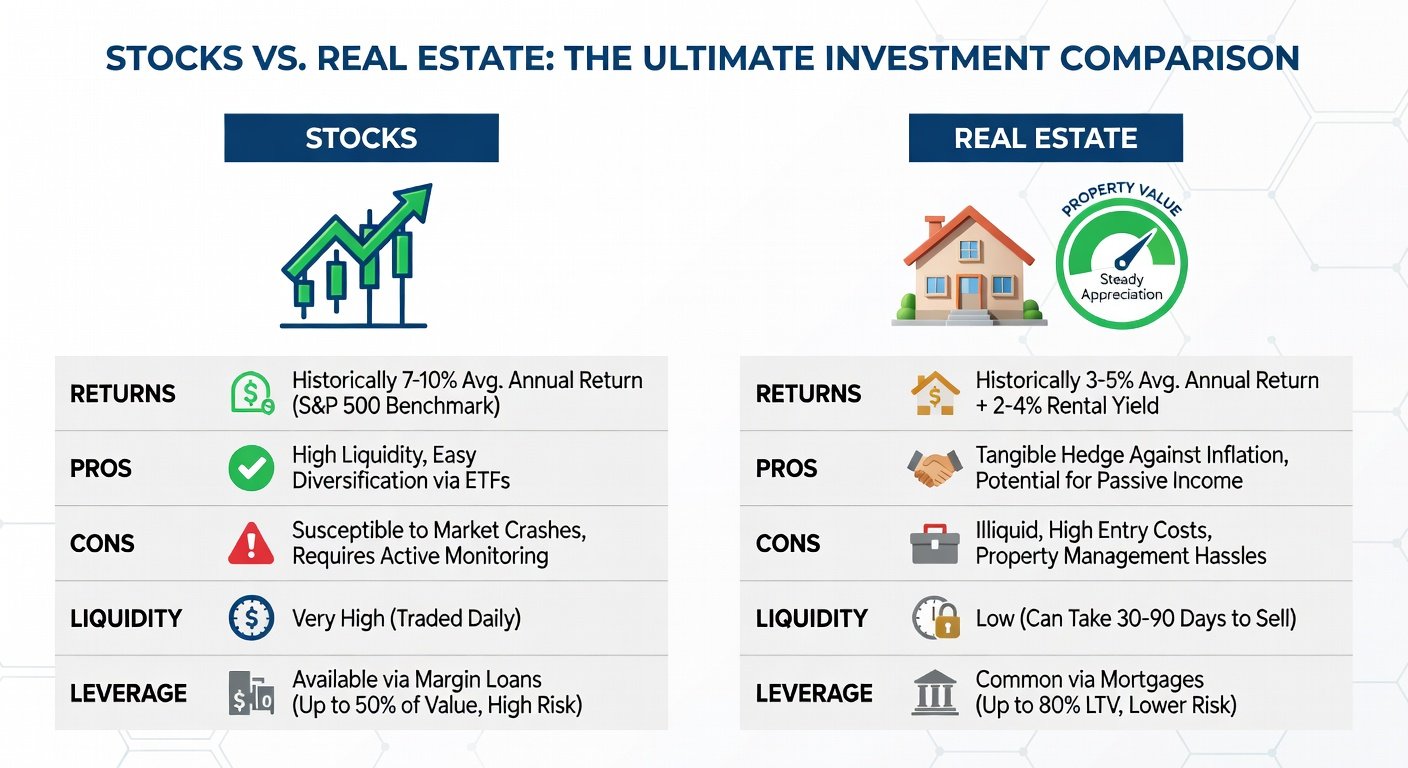

Historical Performance: Lessons from the Past

Historically, stocks have delivered superior long-term compounding. From 1926 to 2023, the S&P 500 averaged about 10% annual returns (including dividends), per data from S&P Dow Jones Indices. Adjusted for inflation, that's around 7%. Real estate, tracked by the Case-Shiller Index, averaged 4-5% nominal appreciation plus 3-5% rental yields, totaling 7-10% in strong markets.

However, future trends alter this. Post-2020, stocks surged with tech dominance (e.g., Magnificent Seven), but 2022's bear market reminded us of volatility. Real estate boomed during low rates but cooled with hikes. For 2026 projections:

- Stocks: Analysts forecast 6-8% annualized returns through 2026, factoring AI growth, but tempered by valuations (CAPE ratio ~35).

- Real Estate: 5-7% total returns, with multifamily rentals resilient amid housing shortages, per Freddie Mac outlook.

Compounding math favors stocks slightly: $100k at 7% grows to $140k in 7 years; at 6%, $133k. But real estate's leverage amplifies this—more on that later.

Pros and Cons: A Head-to-Head Comparison

Stocks excel in liquidity and diversification; real estate shines in leverage and inflation hedging. Here's a detailed table:

| Factor | Stocks | Real Estate |

|---|---|---|

| Compounding Rate (Proj. 2026) | 6-8% | 5-7% (levered: 10-15%) |

| Liquidity | High (sell in seconds) | Low (months to close) |

| Leverage | Low (margin risky) | High (20-30% down) |

| Entry Barrier | $100+ | $50k+ |

| Management | Passive (ETFs) | Active (tenants) |

| Tax Benefits | Long-term capital gains | Depreciation, 1031 |

Leverage and Liquidity: The Make-or-Break Factors

Leverage turbocharges real estate compounding. A $200k property with 25% down ($50k) appreciating 5% yields 20% equity return. Stocks rarely match this without risky margin (up to 50% but with margin calls). Yet, liquidity is stocks' edge: During 2020's crash, stock investors pivoted fast; real estate sellers waited.

Inflation favors real estate—rents rise with CPI—while stocks correlate with GDP growth.

Step-by-Step Entry Guides

Entering Stocks for FI

- Assess Goals: Calculate FI number (25x annual expenses).

- Open Brokerage: Use Vanguard or Fidelity for low-fee index funds.

- Choose Vehicles: VTI (total market) or VOO (S&P 500) for broad exposure.

- Dollar-Cost Average: Invest $500/month automatically.

- Rebalance Annually: Maintain 80/20 stocks/bonds.

- Monitor: Use tools like Personal Capital.

Entering Real Estate for FI

- Build Credit/Savings: Aim for 20% down, 700+ FICO.

- Research Markets: Target cash-flow positive areas (e.g., Midwest).

- Finance: FHA for first-timers (3.5% down) or conventional.

- Acquire: Single-family or syndications via Roofstock.

- Manage: Self or hire property manager (8-10% rent).

- Scale: Refinance to buy more (BRRRR strategy).

Real Investor Examples

Meet Sarah, 35: Invested $50k in VOO in 2016. By 2023, compounded to $150k (18% CAGR amid bull run). FI on track by 2026 via 15% savings rate.

Contrast Mike: Bought duplex 2018 for $300k (20% down). Rents cover mortgage; equity now $200k. Leveraged growth hit 25% returns, FI via rentals by 2027.

Hybrid winner: BiggerPockets forums highlight folks blending REITs (stocks-like real estate) with direct properties.

Risk Assessments and Diversification Strategies

Stocks risk: Sequence of returns (early crashes derail FI). Mitigation: Bonds, cash buffer.

Real estate risks: Vacancies (10% avg), repairs (1% rule), rates (cap rates compress). Use insurance, reserves.

Diversification: 60/40 stocks/REITs + physical properties. Or 50/30/20 stocks/RE/ alternatives. For 2026 FI, stress-test portfolios with 4% safe withdrawal. Reference Investopedia for portfolio tools.

Hybrid approach: REITs like VNQ offer real estate compounding without management, blending best worlds.

Conclusion: Choose Your Compounding Champion

For pure compounding speed and ease, stocks edge out toward 2026 FI—especially with low entry. But real estate's leverage suits hands-on investors chasing outsized returns. Assess your risk tolerance, time, and capital: Start with stocks, layer real estate. Track progress quarterly; adjust for macro shifts like Fed policy. Your FI journey starts now—compound wisely.

Frequently Asked Questions

How do taxes impact stocks vs real estate?

Stocks: 0-20% long-term gains; qualified dividends taxed favorably. Real estate: Deduct mortgage interest, depreciation (27.5 years); 1031 exchanges defer gains. Consult IRS.gov.

What are entry barriers?

Stocks: Minimal ($1 via fractional shares). Real estate: $40k+ down payment, accreditation for syndications.

Best hybrid approach?

70% stocks (index funds), 20% REITs, 10% direct rental—balances liquidity, yield, appreciation.

No comments yet. Be the first!