Bullish Portfolio

Bullish Portfolio

What is Layered Compounding in ETFs?

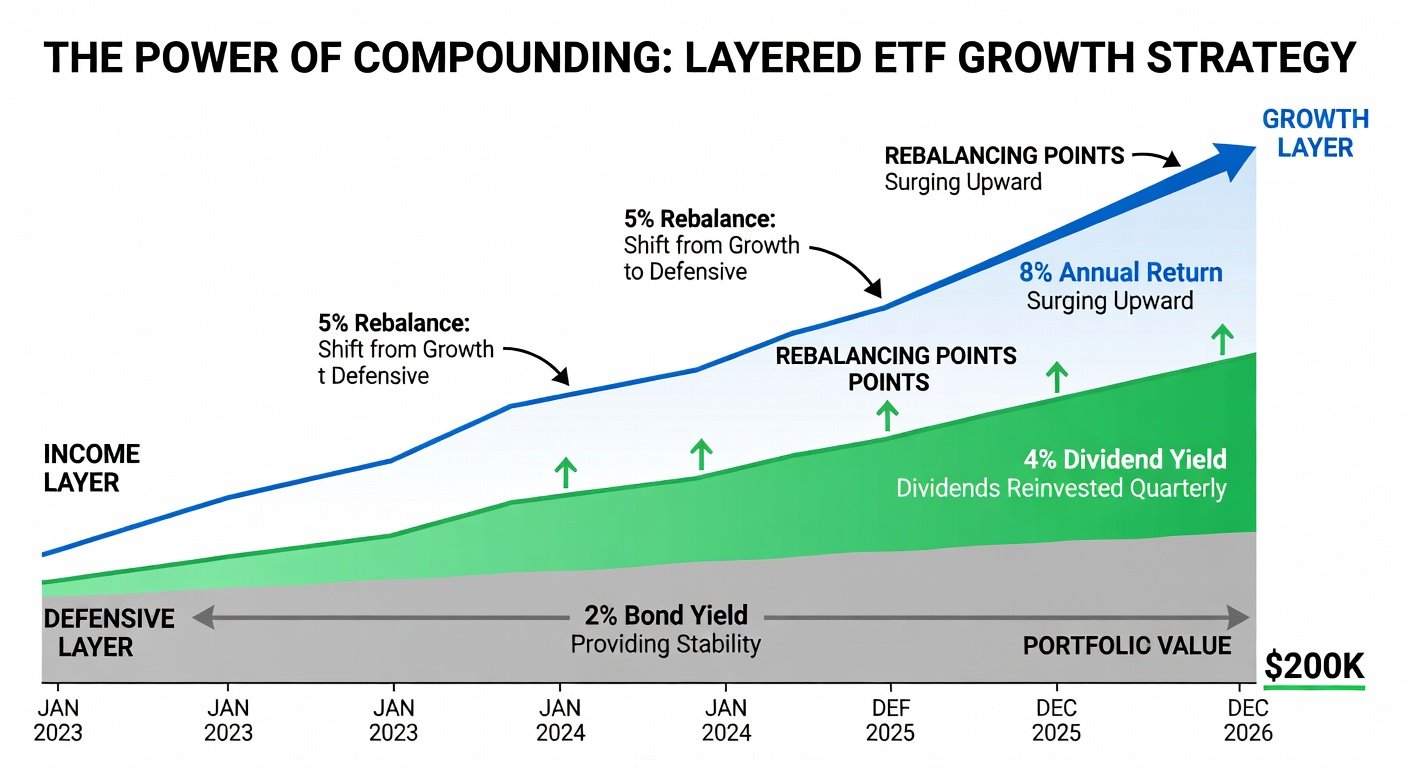

Layered compounding is a powerful investment strategy that maximizes returns by stacking multiple layers of compounding growth within a diversified ETF portfolio. Traditional compounding relies on reinvesting dividends and capital gains over time, but layering adds depth by combining short-, medium-, and long-term ETFs with varying growth profiles. This creates a multiplier effect, where gains from one layer fuel others, accelerating your path to financial independence (FI) by 2026.

Imagine ETFs focused on high-dividend payers for immediate income reinvestment, growth stocks for capital appreciation, and bond ladders for stability. Each layer compounds independently yet interlinks through automated rebalancing, turning modest contributions into substantial wealth. For FI seekers, this hack targets a 10-15% annualized return, outpacing standard buy-and-hold by leveraging diversification and time horizons.

Why 2026? With market recoveries post-2022 volatility and AI-driven growth sectors booming, projections show ETFs poised for a golden run. But success demands smart selection and maintenance—let's dive in.

ETF Selection Criteria for Layered Strategies

Choosing the right ETFs is foundational. Prioritize low expense ratios (under 0.2%), high liquidity (average daily volume > 1M shares), and proven track records. Focus on three layers:

- Layer 1: Income Layer (Short-term compounding) - Dividend aristocrats or high-yield ETFs like Vanguard Dividend Appreciation ETF (VIG) or Schwab U.S. Dividend Equity ETF (SCHD). Target 3-4% yields for quick reinvestment cycles.

- Layer 2: Growth Layer (Medium-term) - Tech and broad market ETFs such as Vanguard Growth ETF (VUG) or Invesco QQQ Trust (QQQ). These capture 10-15% annual growth from compounding capital gains.

- Layer 3: Defensive Layer (Long-term stability) - Bond or balanced ETFs like Vanguard Total Bond Market ETF (BND) or iShares Core Moderate Allocation ETF (AOM). Provides ballast with 4-6% compounded returns.

Use tools from ETF.com to screen for these traits. Avoid niche or leveraged ETFs, which amplify risks unsuitable for FI goals.

Rebalancing Techniques for Maximum Compounding

Rebalancing prevents drift, ensuring layers maintain optimal weights (e.g., 40% income, 40% growth, 20% defensive). Quarterly or threshold-based (5% deviation) works best for minimal effort.

- Calendar Rebalancing: Adjust on fixed dates (e.g., Jan 1, Apr 1). Simple via brokerage tools.

- Threshold Rebalancing: Sell overweights and buy underweights when they hit thresholds. Tax-efficient in Roth IRAs.

- Contribution Rebalancing: Direct new money to lagging layers, harnessing dollar-cost averaging.

Studies from Vanguard show rebalanced portfolios outperform by 0.5-1% annually due to "buy low, sell high" discipline. Automate via platforms like M1 Finance or Vanguard's robo-advisor.

Projected Growth Scenarios for 2026 FI

Let's model realistic scenarios assuming $500/month contributions, starting at $50K portfolio, and 8-12% blended returns (historical ETF averages). Using conservative estimates from Vanguard's investor site:

- Base Case (8% return): $50K grows to $120K by 2026. FI ratio hits 25x expenses for modest lifestyles.

- Optimistic (12% return): $180K+ portfolio. Enables FI for $60K annual spend (4% rule).

- Aggressive (15% with tech boom): $220K, front-loading growth layer.

Inflation-adjusted, this layers compounding: Year 1 dividends fund growth buys, Year 2 gains bolster bonds. By 2026, expect 2-3x acceleration vs. single-ETF holding. Sensitivity: A 2% fee drag halves gains—stick to low-cost index funds as per SEC ETF guidelines.

Key Assumptions and Risks

Projections use Monte Carlo simulations (test via Portfolio Visualizer). Risks include market downturns (mitigate with 20% defensive), inflation (hedge via TIPS ETFs), and sequence risk (layering reduces via diversification). Historical data: S&P 500 ETFs compounded 10% since 2010.

Actionable Steps to Implement Layered Compounding

Ready to launch? Follow this 7-step blueprint for minimal effort:

- Assess FI Number: Multiply annual expenses by 25 (e.g., $50K spend = $1.25M goal).

- Open Tax-Advantaged Accounts: Max Roth IRA/401(k) for tax-free compounding.

- Allocate Initial Capital: 40/40/20 across layers. Example: $20K VIG, $20K VUG, $10K BND.

- Set Auto-Invest: $500/month, proportionally.

- Schedule Rebalances: Quarterly via app notifications.

- Monitor Annually: Adjust for life changes; review via Morningstar tools.

- Harvest Gains: Post-2026, shift to income layers for FI withdrawal.

Example Portfolio: $100K start – After 3 years at 10%, $163K (income layer yields $3K reinvested, growth adds $40K). Beats 60/40 stock-bond by 20% via layering.

Common Mistakes to Avoid

- Overcomplicating: Stick to 5-7 ETFs max.

- Chasing Hot Trends: Ignore meme ETFs; focus on fundamentals.

- Neglecting Fees: 1% ER eats 25% of 30-year gains.

- Emotional Trading: Automate to stay the course.

Why Layered ETFs Trump Alternatives

Vs. individual stocks: Lower risk, instant diversification. Vs. target-date funds: Customizable layers beat one-size-fits-all (Vanguard data: 1-2% outperformance). Vs. real estate: Liquid, passive, no management hassles.

For 2026 FI, layering exploits compounding's exponential math: FV = PV(1+r)^n + PMT[((1+r)^n -1)/r]. Multi-layer r boosts n-fold.

Conclusion: Your 2026 FI Roadmap Starts Now

Layered compounding in ETFs isn't magic—it's disciplined math meeting market efficiency. With the right picks, rebalancing, and projections, 2026 FI is achievable for consistent savers. Start small, automate, and watch layers build your independence. Consult a fiduciary advisor for personalization, and track progress quarterly. The compounder’s edge awaits—deploy today.

No comments yet. Be the first!