Bullish Portfolio

Bullish Portfolio

Introduction: Turning Business Profits into Long-Term Wealth

Many entrepreneurs focus on day-to-day operations and growth, yet overlook how small business income can accelerate financial independence through the power of compounding. This guide shows beginners exactly how to allocate earnings into diversified investments, project realistic timelines, and sidestep common mistakes that reduce returns. Compounding works by reinvesting returns so earnings generate additional earnings over time. When paired with consistent small business cash flow, the effect compounds even faster than salary-based saving alone, allowing owners to build substantial portfolios without relying solely on high salaries or external funding.

Financial independence often means having enough passive income or assets to cover living expenses indefinitely. Small business owners possess a unique advantage because they control revenue streams and can strategically direct surplus profits into vehicles that grow exponentially. This approach transforms operational success into personal wealth security, creating multiple layers of financial resilience.

Understanding the Power of Compounding with Business Income

Business owners often enjoy irregular but potentially higher cash flows than salaried employees. This variability requires deliberate planning to harness compounding effectively. Unlike fixed paychecks, business profits can be scaled through pricing, marketing, or new offerings, creating larger principal amounts to invest early. The mathematics of compounding favors early and consistent contributions, where even modest annual additions can balloon over decades due to exponential growth curves.

Business Cash Flow vs. Traditional Salary Compounding

Salary earners typically contribute fixed percentages from predictable income. Business owners can direct larger lump sums during profitable periods, shortening the timeline to financial independence. For example, a business generating steady monthly profit can allocate half to investments during strong quarters, outpacing a salaried peer earning the same annual total but spreading contributions evenly. This flexibility allows business owners to front-load investments during peak seasons, maximizing the time each dollar spends growing in the market.

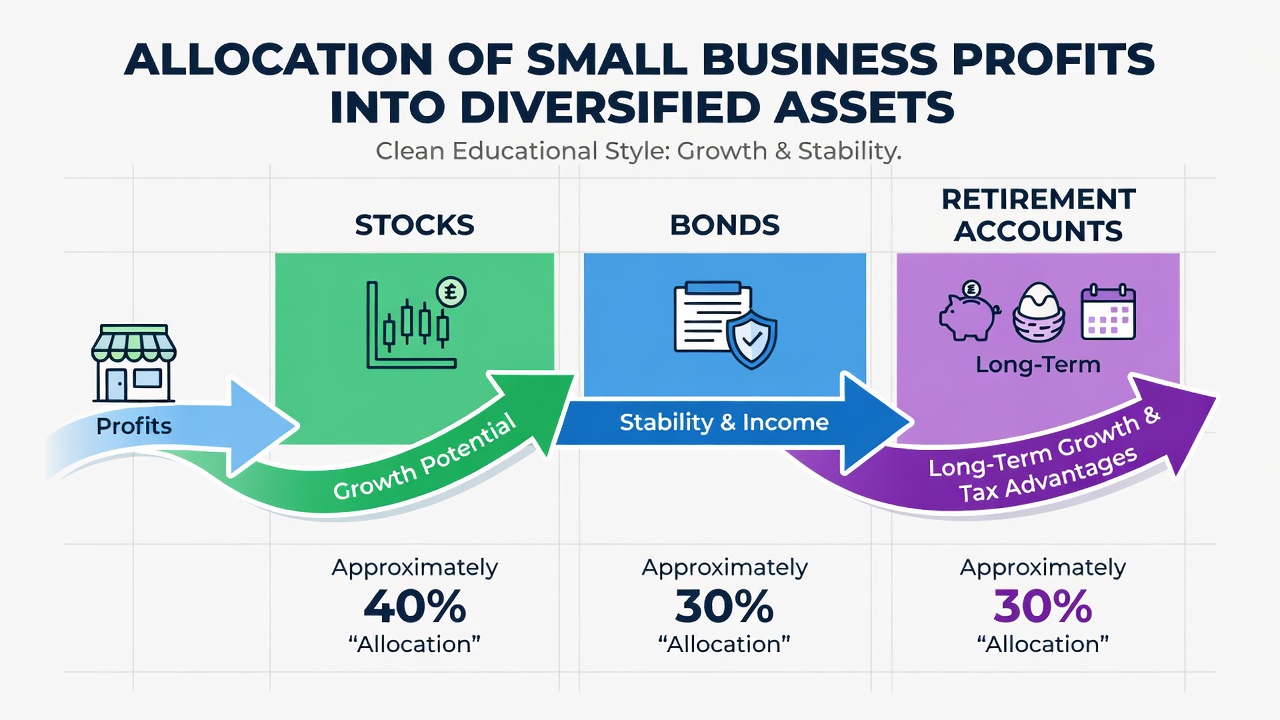

Practical Steps to Allocate Business Earnings

Follow these actionable steps to integrate profits into a compounding strategy. First, calculate your true net profit after all business expenses and taxes. Next, establish an emergency reserve covering several months of personal and business needs to avoid forced withdrawals from investments during downturns. Then, determine an allocation percentage for long-term investments. Choose diversified vehicles such as index funds, bonds, and retirement accounts. Finally, automate transfers on a monthly schedule to maintain consistency regardless of cash flow fluctuations.

Each step builds a foundation for sustainable wealth. Net profit calculations must account for reinvestments in inventory or equipment, while emergency reserves protect against unexpected repairs or slow periods. Automation removes emotional decision-making and ensures compounding never pauses.

Sample Calculations and Growth Timelines

Consider a business netting a moderate annual profit. Allocating a portion yearly into a diversified portfolio earning an average market return shows meaningful growth. After a decade, the investment could reach substantial levels through compounding alone, assuming consistent contributions. Extending the horizon further amplifies results dramatically, demonstrating how business income accelerates the journey toward independence. Adjust assumptions for your situation using online compound interest calculators from reputable sources.

Multiple scenarios help illustrate sensitivity. A conservative allocation with lower returns still builds wealth steadily, while aggressive yet diversified strategies can shorten timelines by several years. Tracking these projections quarterly allows adjustments for changing business performance or market conditions.

Real-World Examples of Business Owners Reaching FI Faster

Several entrepreneurs have documented reinvesting significant portions of profits into low-cost index funds, reaching financial independence in roughly half the time compared to traditional career paths. One bakery owner scaled operations gradually, then directed surplus earnings into broad-market ETFs, achieving portfolio independence by the early forties. Another consultant used seasonal windfalls to max out tax-advantaged accounts first, then funneled remaining profits into taxable brokerage accounts, creating a balanced portfolio that generated reliable withdrawals within fifteen years of starting the business.

These cases highlight common patterns: disciplined percentage-based allocation, avoidance of lifestyle inflation, and regular portfolio reviews. They also show that success stems from treating business profits as fuel for external compounding rather than solely business expansion.

Common Pitfalls That Erode Returns

- Withdrawing profits too frequently for lifestyle upgrades instead of reinvestment.

- Concentrating investments in the business itself without diversification across asset classes.

- Ignoring tax-advantaged accounts that shelter compounding gains from annual taxation.

- Failing to rebalance portfolios annually, allowing risk levels to drift over time.

- Chasing high-risk individual stocks rather than broad diversification, leading to volatility that interrupts compounding.

Actionable Checklist for Tracking Progress

- Review net profit monthly and update allocation targets based on actual performance.

- Log investment contributions in a simple spreadsheet or dedicated financial app for visibility.

- Rebalance asset allocation every twelve months to maintain target risk levels.

- Monitor net worth quarterly to visualize compounding effects and celebrate milestones.

- Consult a tax professional before year-end planning to optimize contribution timing.

- Compare actual returns against initial projections and adjust contribution rates if needed.

Place

Tax Implications and Scaling Efforts FAQ

How do taxes affect reinvested business profits?

Profits are typically taxed as ordinary income or subject to self-employment tax. Using retirement accounts like SEP IRAs or Solo 401(k)s can defer taxes and allow more capital to compound. Visit IRS.gov for current contribution limits and rules.

Should I scale the business or invest profits externally?

Many owners split efforts by reinvesting a portion back into growth initiatives while directing the remainder to diversified markets. This balances higher potential business returns with reduced risk through external compounding. Resources from Investor.gov provide guidance on evaluating these trade-offs.

What if my business income fluctuates seasonally?

Build a larger cash buffer during peak months and maintain a lower but steady investment rate during slower periods to preserve compounding momentum. This approach prevents gaps that could slow long-term growth.

How should I handle unexpected windfalls from the business?

Direct a fixed percentage of any windfall immediately into investments rather than spending first. This habit maintains the compounding engine even during irregular revenue spikes.

Conclusion

Small business income offers a powerful lever for compounding when paired with disciplined allocation, diversification, and consistent tracking. By following the steps, examples, and checklists above, entrepreneurs can transform daily operations into a faster path to financial independence while building lasting financial security.

No comments yet. Be the first!