Bullish Portfolio

Bullish Portfolio

Introduction to Index Fund Investing for Financial Independence

Index fund investing offers a straightforward path to building wealth over time while pursuing financial independence (FI). By tracking broad market indexes, these funds provide diversified exposure to stocks and bonds at minimal cost, allowing investors to benefit from long-term market growth without the need for stock picking or market timing. This approach emphasizes patience and consistency, making it ideal for beginners focused on steady progress rather than high-risk strategies. The philosophy behind index funds aligns closely with the goal of financial independence, where the focus shifts from chasing quick wins to creating a sustainable portfolio that grows reliably through market participation.

The core idea is simple: own a slice of the entire market through low-cost funds that mirror indexes like the S&P 500. Over decades, this method has delivered reliable returns through the power of compounding, where reinvested earnings generate additional growth. For those aiming at FI, index funds reduce emotional stress by removing the guesswork of active management. Many individuals discover that this method frees up mental energy previously spent on researching individual stocks, allowing more time for career advancement or side income streams that further accelerate savings rates.

Understanding the Mechanics of Low-Cost Broad-Market Indexing

Broad-market index funds hold hundreds or thousands of securities in proportions that match a benchmark index. This passive strategy minimizes trading activity, keeping expense ratios extremely low compared to actively managed alternatives. Investors benefit from automatic diversification across sectors, geographies, and company sizes. Because the fund simply replicates the index, there is no need for expensive research teams or frequent trading that can erode returns through transaction costs and taxes.

Key advantages include transparency and predictability. You know exactly what you own because the holdings mirror the index. Automatic rebalancing occurs within the fund itself, so you avoid the tax implications of frequent personal trades. This structure supports long-term holding, which is essential for compounding to work its magic on your portfolio. In addition, the low turnover rate typical of index funds means fewer capital gains distributions, preserving more of your returns inside taxable accounts when necessary.

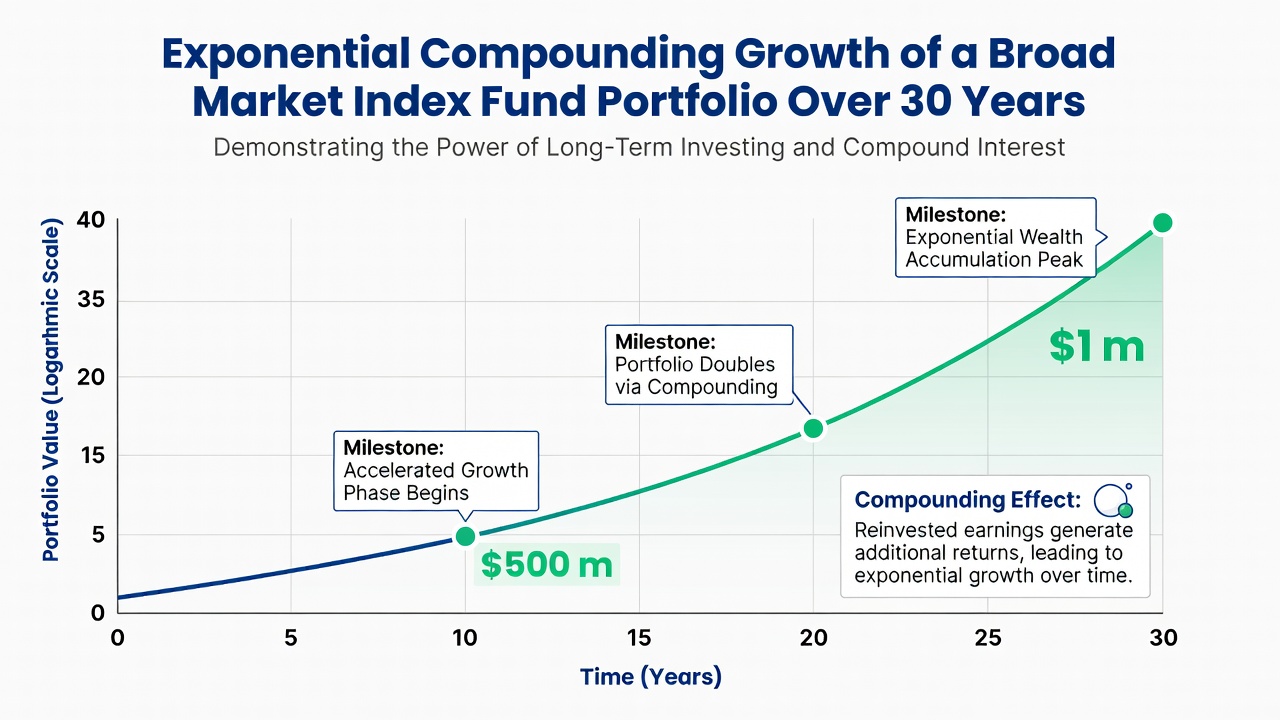

Historical Performance and the Power of Exponential Growth

Decades of data show that broad U.S. stock indexes have delivered average annual returns around 10% before inflation over long periods. This growth compounds exponentially: early investments have more time to multiply through reinvested dividends and capital gains. A modest monthly contribution starting in your 20s can grow substantially by retirement age due to this effect. Investors who stayed the course through multiple market cycles have seen their portfolios expand dramatically because each year’s gains build upon the previous year’s balance.

While past performance does not guarantee future results, the consistency of market returns across multiple economic cycles underscores why index funds remain a cornerstone for wealth building. Volatility occurs, but staying invested through downturns has historically rewarded patient investors. For example, someone who invested consistently during the 2008 financial crisis and continued contributions saw their account recover and surpass previous highs within a few years, illustrating the resilience of broad-market indexing.

Practical Steps for Setting Up Automatic Contributions

Begin by opening a brokerage account that offers commission-free index fund trades. Choose low-cost providers and set up recurring transfers from your bank account on payday. Start with an amount you can sustain, then increase contributions as income grows. The key is to treat contributions like a non-negotiable bill so the habit becomes automatic and less prone to interruption.

- Select target-date or total market funds aligned with your risk tolerance and time horizon.

- Enable automatic dividend reinvestment to maximize compounding.

- Review allocations annually but avoid frequent changes driven by short-term news.

- Track progress using simple spreadsheets or portfolio tools that show contribution totals and growth separately.

- Adjust contribution amounts whenever you receive a raise or reduce expenses.

This automation removes decision fatigue and ensures dollar-cost averaging works in your favor over time. Many successful index investors also maintain a separate high-yield savings account for short-term goals so investment accounts remain untouched except for long-term growth.

Comparing Index Funds to Active Strategies

Active funds rely on managers attempting to outperform the market through research and timing. While some succeed short-term, most underperform broad indexes after fees over five- or ten-year periods. Index funds win by delivering market returns at a fraction of the cost, freeing investors from constant monitoring. Studies consistently show that the majority of active managers fail to beat their benchmarks after expenses, making the simplicity of indexing more attractive for most individuals.

Real-world examples often show index portfolios outperforming the average active fund by several percentage points annually when fees are considered. This gap widens over decades, directly impacting FI timelines. Investors who switch from active funds to low-cost indexes frequently notice the difference within the first few years as more of each return stays invested rather than being paid out in management fees.

Tax-Efficient Account Choices Like IRAs

Tax-advantaged accounts such as IRAs and 401(k)s enhance index fund returns by deferring or eliminating taxes on gains. Traditional IRAs offer upfront deductions, while Roth versions provide tax-free withdrawals in retirement. For FI seekers, prioritizing these accounts maximizes compounding efficiency. Contribution limits are adjusted periodically, so checking current rules each year helps optimize savings.

Learn more about retirement accounts at IRS.gov and investor protections at Investor.gov. Consider backdoor Roth strategies if income limits apply, and always contribute the maximum allowed each year when possible. Additionally, employer-sponsored plans often include matching contributions that represent free money and should be maximized before funding taxable accounts.

Real-World Portfolio Examples with Projected Timelines

Consider a 30-year-old investing $500 monthly in a total stock market index fund. With historical average returns, this could grow to over $1 million by age 65, assuming consistent contributions. Adjusting for higher savings rates accelerates FI, potentially reaching independence in 15–20 years. Adding a spouse’s contributions or incorporating bond funds for stability can further customize the plan.

Another example: a couple combining spousal IRAs with taxable brokerage accounts sees faster growth due to diversified tax treatment. These scenarios illustrate how small, regular actions compound into substantial wealth without complex tactics. A third example involves someone starting later in life who increases monthly contributions aggressively while keeping expenses low, demonstrating that it is never too late to benefit from indexing if the commitment remains steady.

Addressing Common Pitfalls: Volatility and Emotional Decisions

Market dips can trigger panic selling, derailing long-term plans. Successful index investors maintain discipline by viewing volatility as normal rather than a signal to exit. Establish rules in advance, such as never selling during downturns unless life circumstances change dramatically. Keeping a written investment policy statement helps reinforce these commitments during stressful periods.

Other pitfalls include chasing past performance or over-allocating to single sectors. Broad indexing naturally avoids these traps. Regular education and journaling investment decisions help maintain perspective. Many investors also benefit from reading foundational investing books or participating in online communities focused on passive strategies to stay motivated.

Actionable Checklist for Beginners

- Define your FI number based on annual expenses multiplied by 25.

- Open tax-advantaged accounts first before taxable brokerage accounts.

- Fund low-cost total market index funds monthly without interruption.

- Reinvest all dividends automatically to harness compounding.

- Review asset allocation once per year and rebalance only if targets drift significantly.

- Build an emergency fund covering six to twelve months of expenses outside investments.

- Ignore daily market noise and focus on contribution consistency.

- Increase savings rate whenever income rises or discretionary spending falls.

Conclusion

Index fund investing provides a reliable, low-maintenance route to wealth accumulation and financial independence. By focusing on broad diversification, automatic contributions, and tax efficiency, beginners can harness compounding without unnecessary complexity. Start today, stay consistent, and let time work in your favor while avoiding common emotional pitfalls that derail many investors.

No comments yet. Be the first!