Bullish Portfolio

Bullish Portfolio

Introduction to Compounding and Financial Independence

Compounding is one of the most powerful forces in personal finance, allowing your money to grow exponentially over time through the reinvestment of returns. For beginners aiming for financial independence, understanding compounding returns transforms consistent saving into lasting wealth. This article explores the mechanics in depth, provides real-world growth examples with various rates, and delivers actionable steps to implement a compounding-focused strategy that can span decades.

Financial independence means having enough passive income to cover living expenses without relying on active work. Compounding accelerates this by reinvesting earnings, creating a snowball effect where gains generate further gains. Whether you are starting with modest amounts or building from scratch, the principles remain the same: time, consistency, suitable investment vehicles, and disciplined behavior matter most. Early action maximizes the impact because each additional year allows returns to build upon previous returns, often leading to surprising acceleration in later stages.

The Mathematical Power of Compounding Returns

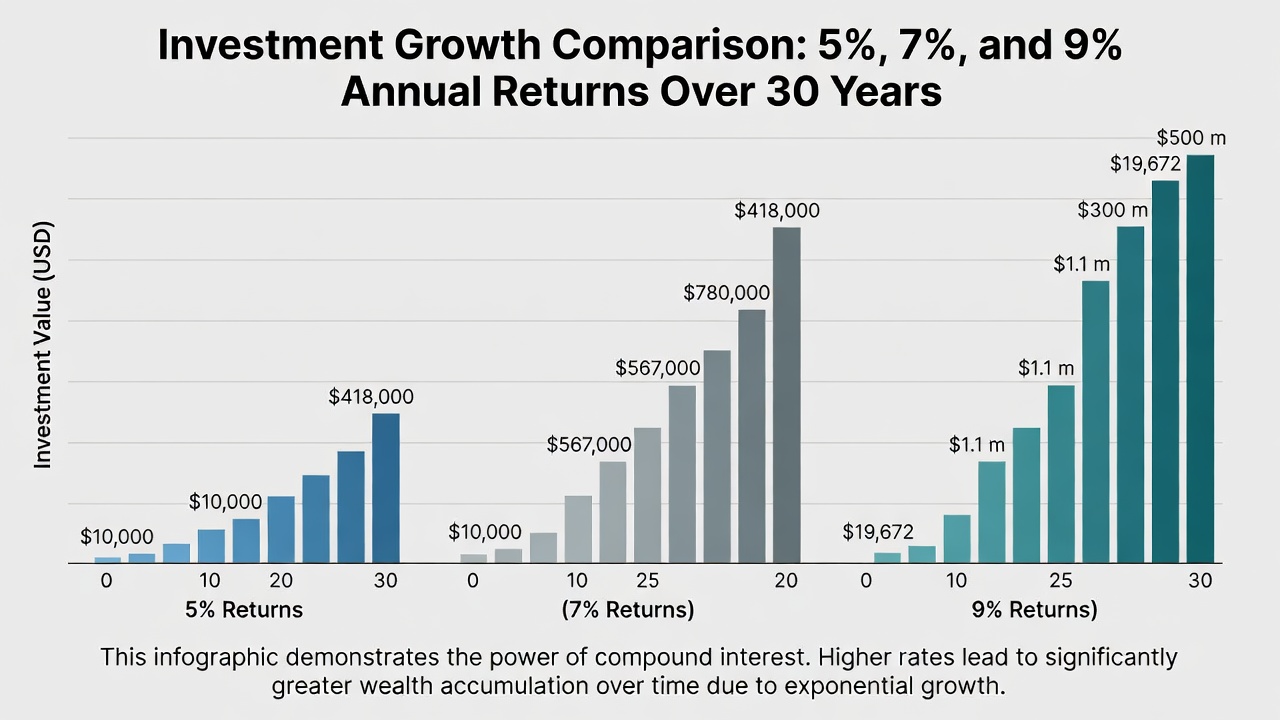

Compounding occurs when investment returns generate additional returns on both the original principal and accumulated earnings. A foundational example: $10,000 invested at 7% annual return grows to approximately $19,672 after 10 years without additional contributions. Adding $500 monthly increases the total dramatically over decades because regular contributions also begin earning returns immediately.

Consider these detailed scenarios over 30 years with consistent $500 monthly contributions, assuming reinvestment and no withdrawals:

- At 5% average annual return: the portfolio reaches roughly $418,000, showing steady but moderate growth driven primarily by contributions.

- At 7% average annual return: the total climbs to roughly $567,000, where compounding adds substantial acceleration after year 15.

- At 9% average annual return: the outcome reaches roughly $780,000, illustrating how higher rates amplify the effect significantly in the final decade.

These illustrations highlight how even small rate differences compound into significant gaps. Historical market data supports average equity returns around 7-10% after inflation for diversified portfolios over long periods, though past performance does not guarantee future results. To visualize further, imagine extending the timeline to 40 years: the 7% scenario would exceed $1.1 million, emphasizing why patience is essential. Beginners should model their own numbers using online calculators to internalize these dynamics before committing capital.

Selecting Low-Cost Investment Vehicles

Choosing efficient vehicles minimizes fees that erode compounding over time. Broad-market index funds and ETFs tracking the S&P 500 or total stock market offer low expense ratios and broad diversification across hundreds of companies. Target-date funds provide automatic diversification and glide-path adjustments as retirement nears, making them ideal for hands-off beginners.

Compare options through reputable platforms and prioritize those with expense ratios below 0.2%. Avoid high-fee actively managed funds unless they consistently outperform net of costs. Retirement accounts such as IRAs and 401(k)s add tax advantages that further boost net compounding by sheltering growth from annual taxation. Robo-advisors can automate allocation and rebalancing for a small advisory fee while still keeping overall costs low. For more details on index investing fundamentals, see Investopedia. Diversification across asset classes reduces volatility, helping investors stay invested during downturns so compounding can continue uninterrupted.

Avoiding Common Behavioral Pitfalls

Behavioral mistakes often derail compounding more than market conditions themselves. Market timing attempts frequently lead to missed gains, while panic selling during downturns locks in losses and resets the compounding clock. High spending reduces contribution capacity, and lifestyle inflation erodes progress by increasing expenses in tandem with income.

Common pitfalls include:

- Checking portfolios too frequently, triggering emotional decisions based on short-term noise rather than long-term trends.

- Ignoring fees that compound negatively over decades, quietly reducing final balances by tens or hundreds of thousands.

- Chasing hot stocks or sectors instead of maintaining diversified, low-cost holdings that capture broad market returns.

- Withdrawing early from tax-advantaged accounts, triggering penalties and lost growth opportunities that cannot be recovered.

- Failing to increase contributions as income rises, missing the chance to accelerate the compounding curve.

Discipline and automation counteract these issues. Set automatic transfers from paychecks and review progress quarterly rather than daily. Maintaining a written investment policy statement helps anchor decisions during volatile periods. Recognizing that markets fluctuate is key; history shows recoveries follow declines, allowing patient investors to benefit fully from compounding cycles.

Tracking Progress with Simple Tools

Free spreadsheets or apps like compound interest calculators help monitor growth and maintain motivation. Input starting balance, monthly contributions, expected return, and time horizon to project outcomes and run sensitivity analyses. Adjust assumptions annually based on actual performance and life changes.

Many brokerage platforms include built-in trackers with visual charts. Combine these with net-worth statements updated monthly to stay motivated and identify needed adjustments. Some investors use simple formulas in personal spreadsheets to project forward under optimistic, base, and conservative scenarios, providing a realistic range rather than a single point estimate.

5-Step Implementation Plan

Follow this structured approach to harness compounding effectively:

- Assess current finances by calculating income, expenses, and existing savings rate, then identify areas to free up at least 10-15% for investing.

- Open suitable accounts such as a Roth IRA or employer-sponsored plan, taking advantage of any matching contributions that represent instant returns.

- Automate monthly contributions starting at any amount and increasing annually by 1% or more whenever raises occur.

- Select low-cost diversified funds aligned with your risk tolerance and timeline, favoring broad equity exposure for growth phases.

- Review annually, rebalance if needed, and increase contributions as income grows while monitoring for lifestyle creep.

Consistency over perfection drives results. Even modest increases in contribution rate or return assumptions yield outsized long-term benefits when sustained over 20 or more years.

Side-by-Side Scenario Comparisons

Scenario A: Start at age 25 with $300 monthly at 6% return until age 65 yields about $530,000. Scenario B: Delay until age 35 but contribute $600 monthly at the same rate yields roughly $430,000. The earlier starter benefits from 10 extra years of compounding despite lower monthly amounts. Adding a third scenario with $400 monthly starting at age 30 reaches approximately $480,000, showing intermediate timing still produces strong results when paired with discipline.

These comparisons underscore starting early. Inflation erodes purchasing power, so target returns exceeding inflation by several percentage points through diversified equities. Rebalancing annually keeps risk levels appropriate as balances grow.

FAQ: Tax Implications and Inflation Effects

How do taxes affect compounding? Tax-advantaged accounts like IRAs defer or eliminate taxes on growth, preserving more capital for reinvestment. Taxable accounts require strategies such as holding investments long-term for favorable capital gains rates. See IRS.gov for current contribution limits and rules.

What about inflation? Inflation reduces real returns. A 7% nominal return with 3% inflation delivers approximately 4% real growth. Adjust expected returns downward in projections to account for this effect over multi-decade periods.

Can I adjust for changing circumstances? Yes. Increase contributions during high-income years or reduce temporarily if needed, then resume. The key remains maintaining the habit over decades. Rebalancing and periodic reviews ensure the portfolio stays on track.

How does risk factor into long-term compounding? Higher equity allocations historically produce stronger compounding but with greater short-term volatility. Younger investors can tolerate more risk, shifting gradually toward bonds as the goal nears.

Conclusion

Compounding transforms disciplined saving into financial independence when applied consistently. By selecting efficient vehicles, avoiding pitfalls, tracking progress, and following a clear plan, beginners can build substantial wealth. Begin today, stay consistent, and let time work in your favor through the remarkable mathematics of compounding returns.

No comments yet. Be the first!