Bullish Portfolio

Bullish Portfolio

Introduction: The Psychology Behind Wealth Building

Behavioral finance bridges the gap between psychology and investing, revealing how cognitive biases often derail even the best compounding strategies. In 2026, investors who master these insights can accelerate wealth accumulation by sticking to disciplined, long-term approaches rather than reacting to market noise. This guide provides practical steps to identify biases, build habits, and compare emotional versus systematic methods for superior results. Understanding these dynamics is essential for anyone aiming to achieve financial independence through consistent compounding over decades.

Understanding Compounding Returns and Behavioral Barriers

Compounding returns occur when investment gains generate additional earnings over time, creating exponential growth. However, human emotions frequently interrupt this process through impulsive decisions. By applying behavioral finance concepts, investors can minimize interference and let compounding work its magic across decades. The power of compounding is most evident in long-term portfolios where small, consistent returns accumulate without disruption from emotional selling or panic buying. Behavioral barriers such as fear and greed act as silent wealth destroyers, often causing investors to abandon sound plans during periods of uncertainty.

Identifying Common Biases That Sabotage Compounding

Loss aversion causes investors to fear losses more than they value equivalent gains, often leading to premature selling during downturns. Recency bias makes recent market events seem more probable to repeat, prompting overreactions to short-term volatility. Other pitfalls include confirmation bias, where investors seek only information supporting existing views, and overconfidence, which inflates perceived ability to time markets. Anchoring bias further complicates decisions by causing individuals to fixate on initial purchase prices rather than current fundamentals. Herd mentality can drive investors to follow crowd behavior during bubbles or crashes, undermining personalized strategies. Recognizing these tendencies is the first step toward mitigation. Regular journaling of investment decisions and reviewing past outcomes can highlight patterns driven by emotion rather than data. Investors who track their emotional responses alongside portfolio performance often discover recurring triggers that lead to suboptimal choices.

Actionable Steps to Build Disciplined Investing Habits

Developing habits that counteract biases requires deliberate effort and repetition. Here are proven steps to foster discipline:

- Automate contributions to investment accounts to remove emotional timing decisions and ensure steady capital deployment regardless of market conditions.

- Set predefined rules for rebalancing portfolios based on target allocations rather than market predictions, reducing the temptation to chase performance.

- Practice mindfulness or consult a fiduciary advisor during high-stress periods to counteract impulsive trades and maintain perspective.

- Review long-term historical data quarterly instead of daily portfolio fluctuations to avoid short-term noise influencing decisions.

- Establish a "cooling-off" period of at least 48 hours before making any significant changes to holdings, allowing rational analysis to prevail.

- Create a written investment policy statement outlining goals, risk tolerance, and rules to reference during volatile times.

- Use visualization techniques to imagine future financial independence, reinforcing commitment to the compounding process.

These habits foster consistency, allowing compounding to compound without behavioral drag. Over time, they become second nature and protect against common psychological pitfalls.

Real-World Examples of Behavioral Tweaks Improving Outcomes

Consider an investor who shifted from frequent trading to a systematic index approach after recognizing loss aversion tendencies. Over five years, this change aligned their portfolio with broader market gains through uninterrupted compounding, resulting in significantly higher terminal wealth. Another example involves an individual who countered recency bias by committing to dollar-cost averaging during the 2022-2023 volatility, resulting in lower average purchase costs and stronger subsequent returns. A third case features a retiree who overcame confirmation bias by diversifying beyond familiar sectors after reviewing objective performance data, leading to more resilient portfolio growth. These stories illustrate how small behavioral adjustments can yield outsized improvements in long-term results.

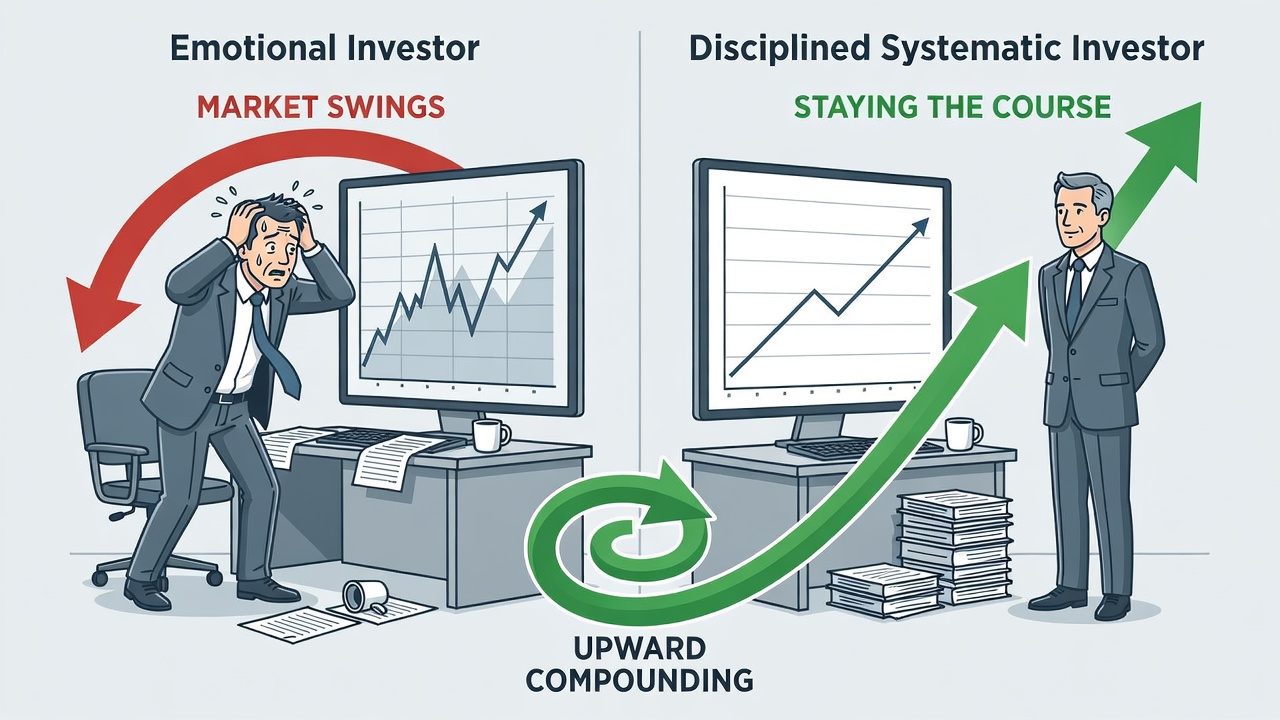

Emotional vs. Systematic Approaches: A Clear Comparison

Emotional investing often leads to buying high during euphoria and selling low amid panic, eroding compounding potential. Systematic strategies, by contrast, rely on rules-based frameworks that maintain exposure through cycles. Data from major institutions shows systematic investors typically outperform their emotional counterparts by avoiding timing mistakes and staying invested longer. Emotional approaches tend to generate higher transaction costs and tax inefficiencies, while systematic methods emphasize low-cost, tax-efficient vehicles. The contrast becomes especially stark during market corrections when emotional investors exit prematurely and miss subsequent recoveries.

Maintaining Consistency During Market Volatility

Market swings in 2026 will test resolve, but predefined plans and diversified allocations help. Focus on your time horizon and goals rather than headlines. Resources from authoritative bodies like the U.S. Securities and Exchange Commission and Investor.gov offer tools for staying informed without emotional overload. Additional guidance from the Federal Reserve can provide macroeconomic context that supports long-term thinking. Practical tactics include limiting news consumption to once per week, maintaining an emergency cash buffer separate from investments, and periodically revisiting personal financial goals to reaffirm commitment.

The Role of Technology and Tools in Behavioral Investing

Modern platforms and apps can reinforce disciplined behavior through features like automatic rebalancing alerts, goal-tracking dashboards, and sentiment-neutral reporting. Robo-advisors often embed behavioral safeguards by limiting user overrides during volatile periods. Selecting tools that minimize decision fatigue while providing transparent data helps investors stay aligned with compounding objectives.

Conclusion

Integrating behavioral finance with compounding strategies equips investors for sustainable wealth growth. By addressing biases head-on and adopting systematic habits, financial independence becomes more attainable in 2026 and beyond.

FAQ

How can I overcome loss aversion when markets drop?

Reframe downturns as buying opportunities aligned with your long-term plan and review historical recovery data to reinforce perspective.

Is recency bias more dangerous in bull or bear markets?

It poses risks in both, but especially after prolonged trends where investors assume continuation without considering mean reversion.

What role does automation play in behavioral success?

Automation removes daily decision points, reducing opportunities for emotional interference and supporting steady compounding.

How often should I review my investment strategy?

Conduct annual reviews or after major life events, avoiding frequent checks that amplify short-term noise.

Can technology fully eliminate emotional biases?

Technology provides helpful guardrails but works best when paired with personal awareness and written rules.

What should I do if I feel tempted to sell during a downturn?

Consult your investment policy statement, wait the required cooling-off period, and focus on your original time horizon and goals.

No comments yet. Be the first!