Bullish Portfolio

Bullish Portfolio

Introduction: Why High-Yield Savings Matter for Beginners

Building wealth starts with a secure foundation. High-yield savings accounts (HYSAs) provide a low-risk way to grow money faster than traditional options while keeping funds accessible. This guide explains their mechanics, tax rules in 2026, and practical steps to integrate them into a broader wealth-building strategy aimed at financial independence. For newcomers, the appeal lies in simplicity and safety. Unlike volatile investments, these accounts offer FDIC insurance up to $250,000 per depositor, protecting principal while delivering better returns. Establishing this base early allows compounding to work its magic over decades, turning consistent small deposits into substantial growth without exposing savings to market swings.

Understanding the Mechanics of High-Yield Savings Accounts

HYSAs function similarly to standard savings accounts but pay higher interest due to lower overhead from online-only banks. Interest compounds, typically daily or monthly, accelerating growth over time. The key difference from low-yield alternatives is the rate environment, which in 2026 continues to favor online institutions. To understand compounding, consider how each interest payment is added to the principal, so future interest calculations include the newly earned amount. This creates an exponential effect rather than linear growth. Tax implications remain straightforward: interest earned is taxable as ordinary income at the federal level. Report it on Form 1099-INT. State taxes may also apply depending on residency. Consult IRS resources for details on reporting requirements. IRS official guidance provides current forms and instructions for accurate filing. Additionally, account holders should review statements regularly to track interest accrual and ensure compliance with any annual reporting thresholds.

Selecting the Optimal High-Yield Account

Choosing the right account involves evaluating several factors. Start by comparing interest rate consistency and any minimum balance requirements that could affect earnings. Confirm FDIC or NCUA insurance coverage to protect deposits. Examine fees for withdrawals, transfers, or account maintenance, as these can quietly reduce net returns. Assess mobile app quality and customer support availability, since most interactions occur digitally. Consider ATM access and ease of linking external accounts for seamless transfers. Compare multiple providers rather than defaulting to the first option. Look for accounts that allow easy automation and provide transparent rate histories. Reading user reviews on independent sites and checking the bank’s regulatory filings can reveal reliability over time. Some institutions also offer tiered rates based on balance levels, which may benefit larger savers.

Automating Deposits for Consistent Growth

Consistency drives compounding. Set up automatic transfers from your paycheck or checking account on payday. Even modest weekly amounts add up significantly over years. Practical steps include calculating affordable contribution amounts based on your budget, scheduling transfers to occur immediately after income arrives, reviewing and increasing contributions quarterly as income grows, and using round-up features offered by some banks to capture spare change. This automation removes decision fatigue and ensures steady progress toward financial independence. Many banks integrate with payroll systems or budgeting apps, allowing transfers to happen the same day funds are deposited. Over time, this habit builds discipline and accelerates the compounding timeline without requiring constant attention.

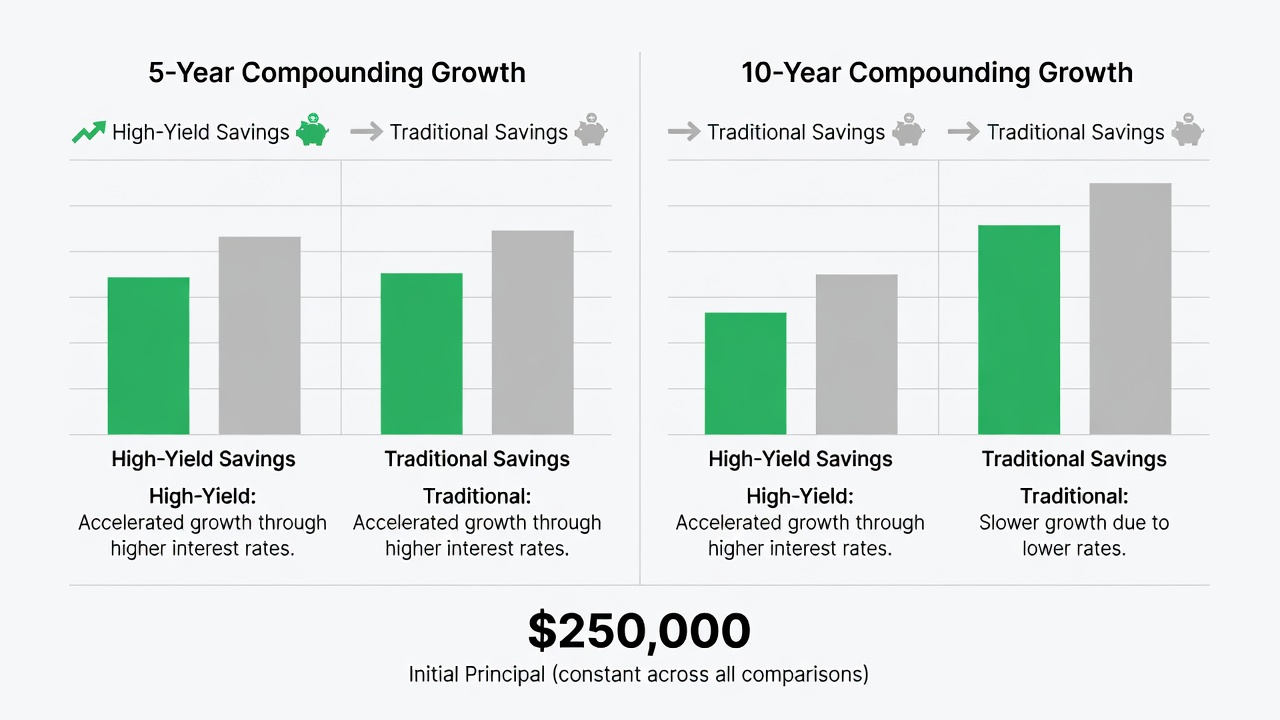

Real-World Compounding Examples Over 5–10 Years

Compounding rewards patience. Consider two scenarios: one using a high-yield account versus a traditional low-yield option. The difference becomes substantial over time due to the higher base rate and reinvested interest. For instance, a consistent monthly deposit pattern over five years can produce noticeably different ending balances when rates differ meaningfully. Extending the horizon to ten years magnifies the gap further, illustrating why starting early matters more than the size of initial deposits. Visual comparisons often highlight how the later years contribute disproportionately to total growth because of accumulated interest on interest.

Comparing High-Yield Accounts to Low-Yield Alternatives

Traditional bank savings often pay far less. The opportunity cost compounds annually. While low-yield accounts may offer branch access, the trade-off in growth usually outweighs convenience for most digital-savvy users. Evaluate your liquidity needs. If frequent in-person banking is required, maintain a small balance at a traditional institution while directing the bulk to a high-yield option. This hybrid approach balances accessibility with optimized returns. Over multiple years, the cumulative difference can represent thousands of dollars in forgone growth that could have been redirected toward other financial goals.

Integrating High-Yield Savings Into a Broader Wealth Strategy

Treat the HYSA as the first layer of your financial pyramid. Once an emergency fund reaches three to six months of expenses, redirect additional savings toward retirement accounts, index funds, or other growth assets. Track progress monthly using simple spreadsheets or built-in bank tools to visualize how contributions and interest combine. Align savings goals with life milestones such as home purchases or career changes. This integration ensures the high-yield account supports rather than competes with long-term investing plans.

Common Pitfalls to Avoid

Common pitfalls include chasing the absolute highest rate without checking stability, ignoring fees that erode returns, and failing to increase contributions with raises. Another mistake is treating the account as a checking substitute, which can trigger withdrawal limits. New users sometimes overlook the impact of inflation on purchasing power or forget to update beneficiary information. Maintaining a written plan that outlines contribution schedules and review dates helps prevent these issues and keeps the wealth-building process on track.

Monitoring Performance and Adjusting Over Time

Regular monitoring ensures the account remains competitive. Set calendar reminders every six months to compare current offerings with your existing rate. If better options emerge, transferring funds is usually straightforward and penalty-free. Keep records of all transfers and interest statements for tax preparation. As your financial situation evolves, adjust automation amounts to reflect new income levels or expenses. This proactive approach maximizes the account’s role in your overall strategy.

Conclusion

High-yield savings accounts form the bedrock for compounding wealth. By understanding mechanics, automating contributions, and avoiding common errors, beginners establish momentum toward financial independence. The next step is opening an account and beginning the automation process today.

FAQ

What are the main risks associated with high-yield savings?

The primary risk is inflation potentially outpacing returns over long periods, though principal remains protected by FDIC insurance. Rate fluctuations represent another consideration, but funds stay liquid. FDIC resources explain insurance coverage in detail.

How liquid are these accounts?

Most offer same-day or next-day transfers to linked accounts. Some impose monthly withdrawal limits, so plan accordingly for larger needs. Understanding transfer timelines helps avoid temporary cash-flow gaps.

When should I scale savings into other assets?

Once your emergency fund is complete, consider moving excess capital into diversified investments while maintaining the high-yield account as a cash buffer. This staged approach reduces risk while pursuing higher long-term returns.

Are there any additional tax considerations in 2026?

Beyond federal reporting, some states tax interest income differently. Review your state revenue department guidelines each year and retain all 1099 forms for accurate filing.

No comments yet. Be the first!