Bullish Portfolio

Bullish Portfolio

Introduction: Why Patience Outperforms in Wealth Building

Building lasting wealth rarely happens overnight. The true engine behind financial independence is compounding returns, yet many investors sabotage their progress through impatience. This guide explores how cultivating patience transforms modest, consistent contributions into substantial portfolios over decades. Compounding works by earning returns on both your initial investment and accumulated gains. The longer the time horizon, the more powerful the effect becomes. However, behavioral biases often interrupt this process, leading investors to sell at the wrong time or chase short-term trends instead of allowing markets to work in their favor over extended periods.

Understanding the psychological aspects of investing is just as critical as grasping the numerical mechanics. Many individuals enter the market with good intentions but quickly become distracted by daily fluctuations, news headlines, and the allure of quick profits. Patience serves as the steady anchor that keeps portfolios aligned with long-term objectives. Without it, even the best investment strategies can underperform due to unnecessary trading and emotional decisions.

The Mathematics of Patient Compounding

Consider two investors starting with the same amount. One remains invested for 30 years, while the other frequently exits during downturns. The patient investor benefits from uninterrupted growth cycles. Historical market data shows that missing just a handful of the best trading days can significantly reduce overall returns, underscoring the cost of reactive behavior. Reinvested earnings create a snowball effect where each period of growth builds upon the previous one, accelerating wealth accumulation exponentially rather than linearly.

Patience allows reinvested dividends and interest to accelerate growth exponentially. This principle applies across asset classes, from broad stock market indexes to diversified bond holdings. For deeper insight into these dynamics, explore resources at Investopedia. Investors who grasp the exponential nature of compounding are more likely to tolerate short-term volatility because they understand that time is the most powerful variable in the equation.

Real-Life Examples of Patient Compounding Success

Warren Buffett built his fortune primarily through long-term ownership rather than frequent trading. His approach demonstrates how decades of holding quality businesses generate outsized results. Similarly, many ordinary investors who maintained steady contributions to index funds during market crashes of 2008 and 2020 saw their accounts recover and surpass previous highs within a few years. These examples are not isolated; countless individuals who started small and remained consistent have achieved financial independence by age 50 or 60 through disciplined, patient strategies.

Another compelling case involves teachers and engineers who contributed regularly to retirement accounts without attempting to time entries or exits. Over 25 to 35 years, their portfolios often grew to seven figures solely because they avoided the temptation to react to every economic headline. These stories highlight that time in the market consistently beats attempts to time the market.

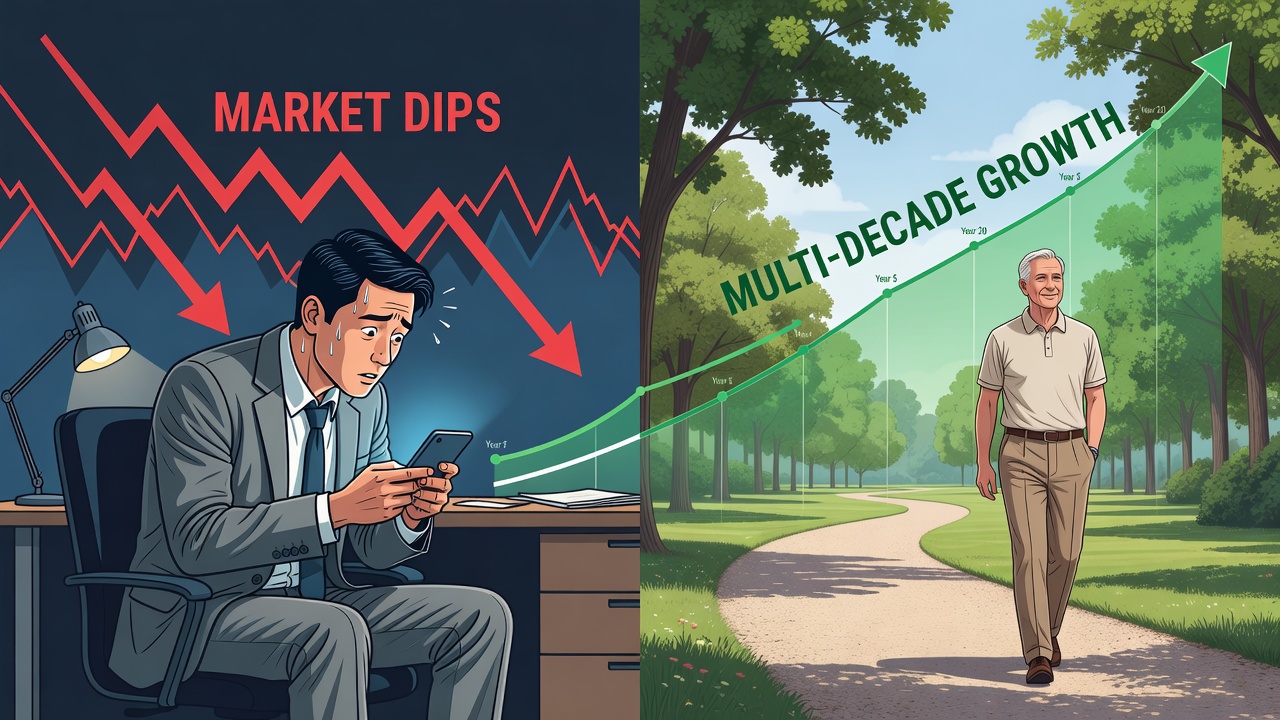

Short-Term vs. Multi-Decade Outcomes

Short-term trading often produces disappointing net results after fees and taxes. In contrast, a multi-decade buy-and-hold strategy captures the full power of compounding. Investors who panic-sell during corrections miss the subsequent recoveries that restore and expand portfolio value. The difference becomes dramatic when comparing a five-year horizon against a 30-year horizon: the longer period allows multiple full market cycles to play out, smoothing volatility and maximizing growth.

Visual comparisons reveal stark differences: a portfolio left untouched grows steadily, while one subjected to frequent adjustments lags due to missed opportunities and transaction costs. Data from major institutions consistently shows that patient investors outperform those who trade actively over extended periods.

Common Behavioral Traps That Disrupt Growth

- Recency bias: Overweighting recent market events and abandoning long-term plans after short periods of underperformance.

- Loss aversion: Selling assets at the first sign of decline to avoid further losses, even when fundamentals remain sound.

- Overconfidence: Believing one can predict market movements better than professionals or algorithms.

- Herd mentality: Following popular trends instead of maintaining a disciplined allocation aligned with personal goals.

- Confirmation bias: Seeking only information that supports the desire to make impulsive changes.

Actionable Steps to Build Investor Discipline

- Define clear financial goals with specific timelines and write them down for future reference.

- Automate contributions to remove emotional decision-making from the process entirely.

- Rebalance portfolios on a fixed schedule rather than reacting to news cycles or price swings.

- Maintain an emergency fund separate from investment accounts to avoid forced sales.

- Review progress annually instead of daily or weekly to reduce anxiety and second-guessing.

- Educate yourself continuously through reputable sources to reinforce the value of patience.

Techniques for Staying the Course During Market Swings

During volatility, focus on your written investment policy statement that outlines acceptable risk levels and target allocations. Limit news consumption to scheduled times rather than constant monitoring. Practice mindfulness or journaling to manage emotional responses before they lead to action. Consider dollar-cost averaging, which turns market dips into buying opportunities by spreading purchases over time. Resources from established firms like Vanguard provide excellent frameworks for maintaining composure. Additionally, connecting with a fiduciary advisor periodically can offer objective perspective when markets feel uncertain.

Common Mistakes to Avoid

One frequent error is checking portfolio values too often, which amplifies the emotional impact of normal fluctuations. Another is abandoning a diversified strategy in favor of concentrated bets based on recent performance. Investors also commonly underestimate the cumulative effect of small, repeated trades that erode returns through fees and taxes. Avoiding these pitfalls requires deliberate systems such as pre-set rules for when and how to make changes.

Practical Checklist for Patient Investing

- Write down your investment thesis and review it quarterly without making reactive adjustments.

- Set alerts for major life changes rather than daily price movements.

- Track total portfolio value, not individual holdings, to maintain perspective.

- Consult a fiduciary advisor before making major allocation shifts.

- Celebrate milestones based on years invested, not short-term gains.

- Revisit your risk tolerance every few years as personal circumstances evolve.

FAQ: Mindset Challenges in Long-Term Investing

How do I resist the urge to sell during a crash?

Remind yourself that market declines are normal and historically followed by recoveries. Review your original plan and avoid checking prices daily. Focus instead on the long-term data that shows patience has rewarded disciplined investors repeatedly.

What if I started investing late?

Compounding still works powerfully even with shorter timeframes. Increase contribution rates and maintain a patient allocation to maximize remaining years. Many people begin in their 40s or 50s and still reach meaningful milestones through consistent effort.

Is patience the only factor needed?

Patience must pair with proper diversification and low costs. Together these elements create the optimal environment for compounding to flourish. Learn more about regulatory perspectives at SEC.gov.

How can I measure my progress without daily checks?

Use quarterly or annual snapshots that focus on contribution consistency and overall trajectory rather than precise valuations at any single moment.

Conclusion

Patience remains the most undervalued skill in investing. By understanding behavioral traps, implementing structured routines, and focusing on long-term outcomes, investors position themselves for the full benefits of compounding returns on the path to financial independence. The journey requires discipline, but the rewards compound far beyond monetary gains into genuine financial freedom.

No comments yet. Be the first!