Bullish Portfolio

Bullish Portfolio

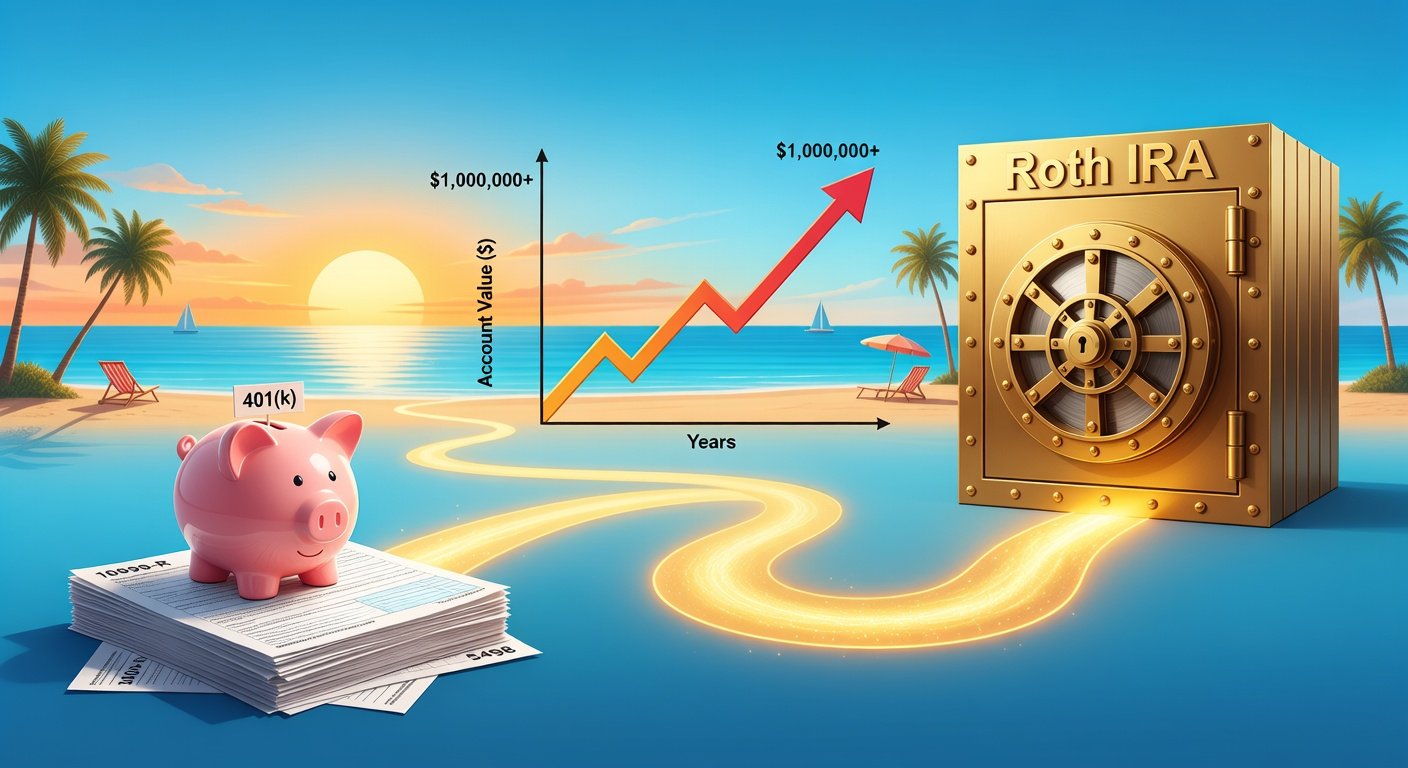

Maximizing Retirement Savings: Roth IRA and 401k Strategies for 2026

Planning for retirement has never been more critical, especially with inflation and market volatility in play. As we look ahead to 2026, savvy investors are focusing on Roth IRAs and 401k plans to build tax-advantaged wealth. These accounts offer powerful benefits: Roth IRAs provide tax-free growth and withdrawals, while 401ks often come with employer matches that supercharge your savings. In this guide, we'll explore five practical strategies to maximize contributions, optimize asset allocation, leverage employer matches, execute tax-efficient rollovers, and diversify for faster growth. We'll also cover updated limits, real-world examples, and common pitfalls to avoid.

The IRS typically announces contribution limits annually, with adjustments for inflation. For 2025, the 401k limit is $23,500 (plus $7,500 catch-up for those 50+), and Roth IRA is $7,000 ($8,000 catch-up). Expect modest increases for 2026—check the IRS website for official updates. Now, let's dive into the strategies.

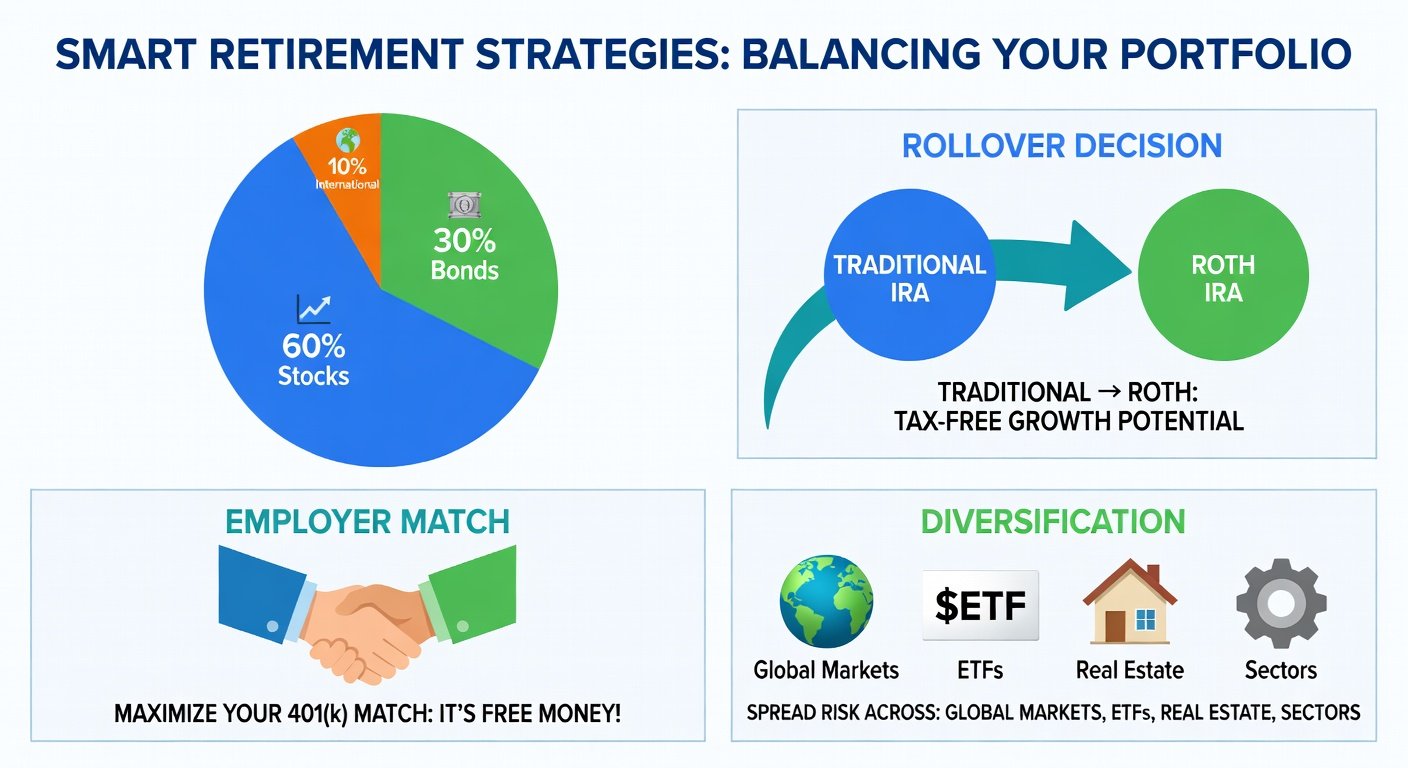

Strategy 1: Fully Capture Your Employer Match

The employer match is free money—don't leave it on the table. Many companies match 50% to 100% of your contributions up to 4-6% of your salary. For example, if you earn $100,000 and your employer matches 100% up to 5%, contributing $5,000 gets you an extra $5,000 instantly.

Real-world example: Sarah, a 35-year-old marketing manager, was only contributing 3% to her 401k, missing half her match. By bumping to 6%, she added $6,000 from her employer annually, growing her nest egg by over $500,000 by retirement (assuming 7% returns).

Common mistake: Treating the match as optional. Prioritize it before other savings. Use payroll deduction for automatic contributions.

Strategy 2: Optimize Asset Allocation for Growth

Asset allocation is the foundation of long-term returns. A common rule: subtract your age from 110 to determine stock allocation (e.g., 75% stocks at age 35). For 2026, with markets favoring growth, tilt toward diversified index funds.

- Target-date funds: Hands-off option that auto-adjusts to more bonds as you age.

- 60/40 split: 60% equities (S&P 500 ETF), 40% bonds for balance.

- Rebalance annually: Sell winners, buy losers to maintain targets.

Example: Mike allocated 80% to stocks early, riding bull markets, then shifted to 50/50 by 50. This beat a static portfolio by 1.5% annually.

Mistake to avoid: Panic-selling during downturns. Stay the course—time in the market beats timing the market.

Strategy 3: Execute Tax-Efficient Rollovers

Rollovers convert traditional 401ks/IRAs to Roths, paying taxes now for tax-free future growth. Ideal if you expect higher taxes in retirement or have low-income years.

- Direct rollover from old 401k to Roth IRA (no withholding).

- Pay taxes from external funds to maximize the rollover amount.

- For 2026, mega backdoor Roth: Contribute after-tax to 401k (up to $70,000 total limit), then convert.

Visit the IRS retirement plans page for rollover rules. Example: After a job change, Tom rolled $50,000 to Roth, paying $12,000 tax. In 20 years, that grows tax-free to $200,000+.

Mistake: Indirect rollovers triggering 20% withholding and 60-day deadlines.

Strategy 4: Master Diversification Techniques

Diversification reduces risk without sacrificing returns. Spread across asset classes, geographies, and sectors.

- ETFs for broad exposure: VTI (total stock), BND (bonds), VXUS (international).

- Alternative assets: 10-20% in REITs or commodities via funds.

- Roth ladder: Convert portions annually to manage taxes.

Example: During 2022's bear market, Lisa's diversified portfolio (50% US stocks, 20% international, 20% bonds, 10% gold) dropped only 12% vs. S&P's 20%.

Mistake: Over-concentration in employer stock—limit to 10%.

Strategy 5: Leverage Spousal and Catch-Up Contributions

Married? Contribute to a non-working spouse's IRA. Over 50? Add catch-ups. For 2026, combine 401k ($24,000+ est.), Roth IRA ($7,200+), and HSA if eligible for triple tax benefits.

Example: The Johnsons maxed both 401ks ($48,000 total) and IRAs ($14,000), plus match, hitting $70,000/year savings on dual incomes.

Mistake: Forgetting income limits for Roth IRA direct contributions (phase-out at $150k+ MAGI single).

Common Pitfalls and Final Tips

Avoid early withdrawals (10% penalty + taxes), ignoring fees (choose low-cost funds <0.1%), and lifestyle inflation—save raises first. Track progress with tools like Vanguard's retirement calculator.

By implementing these strategies, you could grow savings 20-30% faster. Start today: Review your plan, increase contributions by 1%, and consult a fiduciary advisor. Your 2026 self will thank you.

No comments yet. Be the first!