Bullish Portfolio

Bullish Portfolio

Roth IRA vs. 401(k): Key Comparison for 2026 Retirement Planning

As we head into 2026, retirement savers face evolving rules under the SECURE 2.0 Act, making the choice between Roth IRAs and 401(k)s more strategic than ever. Both offer tax advantages and growth potential, but they shine in different scenarios. This guide breaks down contribution limits, tax benefits, employer matches, and new regulations to help you optimize your plan.

Whether you're a young professional prioritizing tax-free growth or a high earner chasing matches, understanding these accounts is crucial. We'll provide a decision framework based on age, income, and risk tolerance, plus tips to blend them for diversified growth.

Contribution Limits in 2026

Contribution limits rise annually with inflation. For 2026, expect:

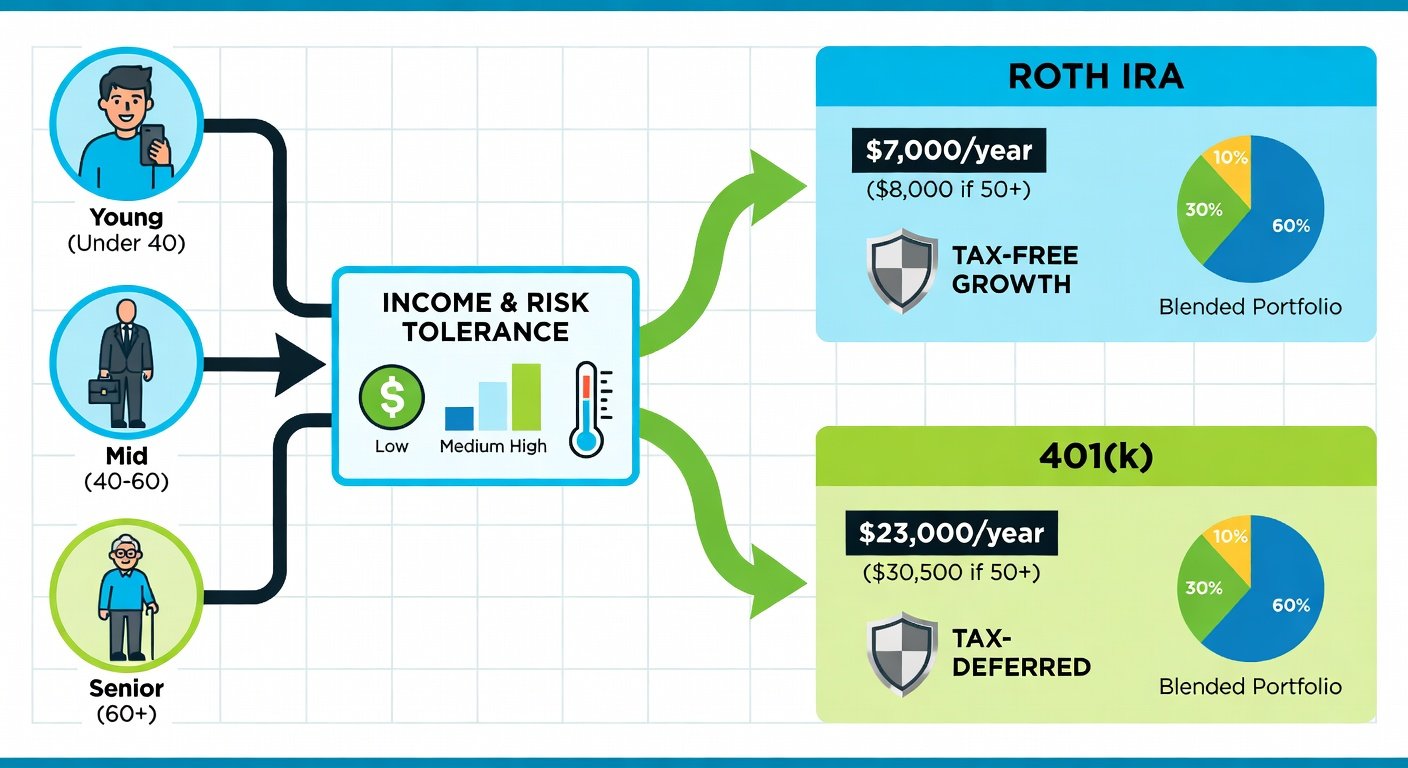

- 401(k): Employee deferral limit projected at $24,000 (up from $23,500 in 2025), plus employer matches up to a total of $69,000 or 100% of compensation.

- Roth IRA: $7,500 for those under 50 ($8,500 for 50+), income-limited (phase-out starts at $150,000 MAGI single/$236,000 married).

401(k)s allow higher contributions, ideal for aggressive savers, while Roth IRAs offer flexibility for self-employed or side-hustlers. Check the latest from the IRS 401(k) limits page.

Tax Advantages: Roth vs. Traditional

Tax treatment is the biggest differentiator:

- Roth IRA/401(k): Post-tax contributions grow tax-free; qualified withdrawals after 59½ are tax-free. Perfect if you expect higher taxes in retirement or want hedge against future rate hikes.

- Traditional 401(k): Pre-tax contributions reduce current taxable income; withdrawals taxed as ordinary income. Best for those in peak earning years seeking immediate relief.

Many 401(k) plans now offer Roth options. For 2026, mega-backdoor Roth conversions remain viable for high earners exceeding limits. Learn more via the IRS Roth IRA overview.

Employer Matches and New 2026 Regulations

Employer matches make 401(k)s unbeatable—free money! Average match is 4-6% of salary. Roth IRAs lack matches but offer investment freedom (stocks, ETFs, no company restrictions).

SECURE 2.0 brings changes: automatic enrollment up to 15%, higher catch-up limits ($11,250 for ages 60-63), and penalty-free withdrawals for emergencies. These favor 401(k)s for employer-sponsored perks. See details in the IRS SECURE 2.0 FAQ.

Decision-Making Framework: Age, Income, and Risk Tolerance

Use this framework to choose:

- Age:

- Under 40: Prioritize Roth IRA/401(k) for decades of tax-free compounding.

- 40-59: Max 401(k) match first, then Roth IRA.

- 60+: Focus on catch-up contributions; blend for RMD avoidance.

- Income:

- Under phase-out ($150k single): Roth IRA shines.

- Over $200k: 401(k) match + backdoor Roth.

- Risk Tolerance:

- Conservative: Target-date funds in both.

- Aggressive: Stock-heavy Roth for growth.

Score yourself: If matches available, 401(k) first (100% return on match). Then Roth IRA for tax diversification.

Tips to Maximize Both Accounts

Don't choose—use both!

- Step 1: Contribute enough to 401(k) for full match.

- Step 2: Fund Roth IRA if eligible.

- Step 3: Use mega-backdoor if plan allows (after-tax to Roth).

- Invest smart: Low-cost index funds (e.g., S&P 500 ETFs) for 7-10% avg returns.

- Rebalance annually: 60/40 stocks/bonds adjusting for age.

- Monitor regs: 2026 may see Roth conversion tweaks.

Avoid early withdrawals—10% penalty + taxes erode gains.

Case Studies: Blending Roth IRA and 401(k) for Success

Case 1: Sarah, 32, $90k Income, Moderate Risk

Sarah maxes her 4% 401(k) match ($3,600), adds $7,000 to Roth IRA. Invests in total market ETFs. By 65, at 8% return: ~$1.2M tax-free. Blending captures match + Roth growth.

Case 2: Mike, 48, $250k Income, High Risk

Mike does mega-backdoor Roth ($46k post-tax to Roth IRA/401(k)). Full 6% match. Portfolio: 80% equities. Projects $3M+ by retirement, diversified taxes.

Case 3: Retiree Couple, 62, $180k Combined

They use catch-ups ($11k each 401(k)), Roth conversions to fill low brackets. Result: Minimized RMD taxes, $2.5M blended portfolio yielding 4% safely.

These cases show blending reduces risk—employer perks + personal control + tax flexibility.

Final Thoughts for 2026

In 2026, Roth IRA and 401(k) together build bulletproof retirement. Prioritize matches, embrace Roth for future-proofing, and adapt to regs. Consult a fiduciary advisor for personalization. Start today—compound interest waits for no one.

No comments yet. Be the first!