Bullish Portfolio

Bullish Portfolio

Understanding the 401k to Roth IRA Rollover in 2026

A 401k to Roth IRA rollover can supercharge your retirement savings by converting pre-tax contributions into tax-free growth potential. With potential tax law changes looming in 2026, now's the time to plan. This strategy allows you to pay taxes upfront on converted funds, enabling tax-free withdrawals in retirement. It's especially powerful for long-term planning, as Roth IRAs offer no required minimum distributions (RMDs) during your lifetime, giving your investments more time to compound.

We'll cover eligibility, step-by-step execution, direct vs. indirect methods, tax implications, benefits for returns, a handy checklist, common pitfalls, and when it's ideal based on income levels.

Eligibility for a 401k to Roth IRA Rollover

To qualify, you generally need to have left your employer or be eligible for an in-service withdrawal if still employed. Key criteria include:

- Access to your 401k balance (post-employment or in-service distribution allowed).

- No outstanding 401k loans.

- Plan allows rollovers—most do, but confirm with your provider.

In 2026, watch for updates from the IRS, as contribution limits and income phase-outs may adjust for inflation.

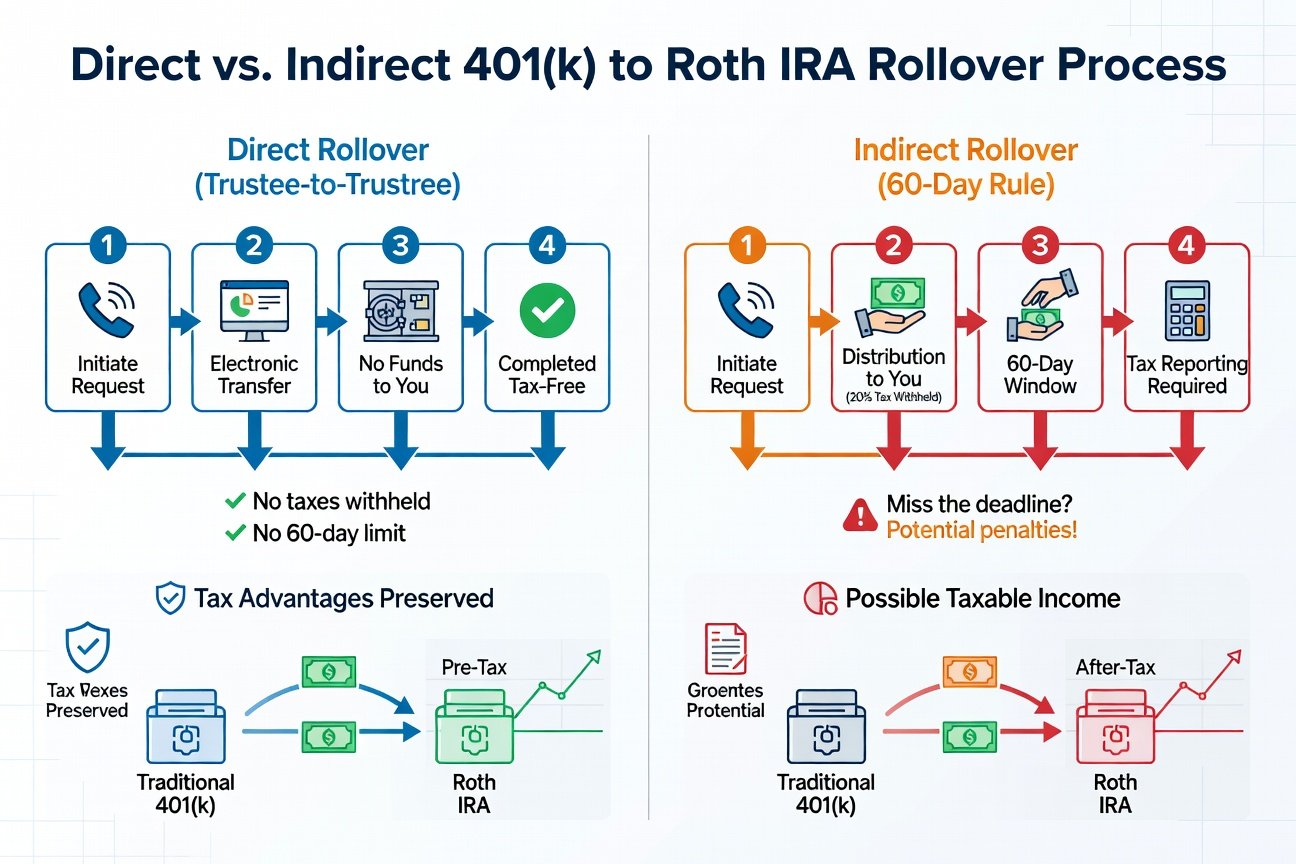

Direct vs. Indirect Rollover: Which Method to Choose?

Choose wisely to avoid tax headaches.

Direct Rollover (Recommended)

Your 401k provider transfers funds straight to your Roth IRA custodian. No taxes withheld, no 60-day rule stress. Ideal for simplicity and avoiding penalties.

Indirect Rollover

You receive a check, must deposit into Roth IRA within 60 days. 20% mandatory withholding applies (you cover from other funds to roll full amount). Only one indirect per 12 months. Riskier—miss the deadline, face taxes and 10% penalty if under 59½.

Pro tip: Always opt for direct to minimize risks.

Step-by-Step Guide to Executing the Rollover in 2026

Follow these steps for a smooth process:

- Contact Your 401k Provider: Request rollover forms. Specify Roth IRA direct rollover.

- Open or Confirm Roth IRA: Use providers like Fidelity or Vanguard. Ensure account details match exactly.

- Complete Forms: Provide Roth IRA account number, custodian info. Elect direct transfer.

- Choose Assets: Decide on cash, in-kind transfer (ETFs/stocks), or mix. Note: Some 401ks liquidate to cash.

- Handle Taxes: Calculate conversion amount; pay estimated taxes via Form 8606.

- Confirm Receipt: Verify funds in Roth IRA within 1-2 weeks.

- Report on Taxes: File Form 1099-R and 8606 for 2026 taxes.

Tax Implications of the Rollover

The big caveat: Roth conversions are taxable as ordinary income in the year of conversion. For example, rolling $100,000 adds $100,000 to your taxable income, potentially pushing you into a higher bracket.

- 2026 Brackets (Estimated): Single filers: 10-37%. Married: Similar scales.

- 5-Year Rule: Converted principal accessible penalty-free after 5 years or age 59½.

- No Income Limits: Unlike contributions, conversions have no AGI caps since 2010.

Consult a tax advisor or use IRS rollover guidance for precision.

How This Strategy Enhances Long-Term Retirement Planning and Returns

Roth conversions shine for tax diversification. Pay taxes now at lower rates, enjoy tax-free growth forever. Key benefits:

- Tax-Free Withdrawals: No RMDs, heirs inherit tax-free.

- Boosted Returns: More compounding without tax drag. A $100k conversion at 7% annual return grows to ~$761k in 30 years, all tax-free.

- Hedge Against Future Taxes: If rates rise post-2025 TCJA sunset, you're protected.

- Medicare/ACA Optimization: Lower future MAGI reduces premiums.

Integrate with 401k investing: Roll to Roth for low-cost index funds, enhancing overall portfolio efficiency.

401k to Roth Rollover Checklist

Print this for your process:

- ☐ Verify eligibility with 401k admin.

- ☐ Open Roth IRA if needed.

- ☐ Calculate tax impact (use tax software).

- ☐ Request direct rollover form.

- ☐ Fund tax payment from non-retirement sources.

- ☐ Track 1099-R delivery (Jan 2027).

- ☐ File Form 8606 with 2026 return.

Common Pitfalls to Avoid

Steer clear of these traps:

- Pro-Rata Rule: If you have pre-tax and after-tax 401k funds, taxes apply proportionally.

- 60-Day Miss: Indirect rollovers fail often—stick to direct.

- Bracket Creep: Convert in chunks over years to stay in lower brackets.

- Recharacterization Gone: No undoing conversions since 2018.

- Provider Fees: Shop for low-cost Roth custodians like Fidelity.

When Is It Ideal? By Income Level

Tailor to your situation:

- Low Income (<$100k): Prime time—low rates, fill brackets optimally.

- Middle Income ($100k-$250k): Ladder conversions over 2-5 years.

- High Income (>$250k): Strategic in low-income years (e.g., sabbatical). Watch AMT.

- Near Retirement: If expecting higher future taxes or longevity.

Run projections with tools like Vanguard's retirement planner.

Final Thoughts

A 2026 401k to Roth IRA rollover is a proactive move for tax-efficient retirement. By paying taxes now, you unlock decades of tax-free growth, outperforming traditional 401k holds in many scenarios. Start planning today—consult a fiduciary advisor for personalized math. Your future self will thank you.

No comments yet. Be the first!