Bullish Portfolio

Bullish Portfolio

Why Prioritize Roth IRAs and 401(k)s for 2026 Retirement Planning?

Roth IRAs and 401(k)s remain cornerstone vehicles for tax-advantaged retirement savings. In 2026, with potential tax rate hikes on the horizon and market volatility from geopolitical tensions and AI-driven growth, low-fee funds offer the best path to compounding wealth. Roth IRAs provide tax-free withdrawals, ideal for high-growth assets, while 401(k)s enable employer matches and higher contribution limits. This guide spotlights the best mutual funds, ETFs, and index funds tailored to current conditions, emphasizing expense ratios under 0.1% for maximum returns.

Amid 2025's market rebound—S&P 500 up ~25% YTD driven by tech—2026 projections suggest 8-12% annualized returns, per analysts, but with inflation lingering at 2-3%. Focus on diversified, low-cost options to weather uncertainties.

Current Market Conditions Shaping 2026 Fund Choices

Entering 2026, equities lead with U.S. large-caps outperforming amid Fed rate cuts. International markets lag but offer value, while bonds stabilize at 4-5% yields. High-growth sectors like tech and renewables shine, but recession risks demand balance. Low-fee passive funds from Vanguard and Fidelity dominate, capturing 90%+ of market benchmarks at minimal cost.

Top Low-Fee Index Funds for Roth IRAs and 401(k)s

Index funds track broad markets with rock-bottom fees, perfect for buy-and-hold strategies.

- Vanguard Total Stock Market Index Fund (VTSAX/VTI): Expense ratio 0.04%. Tracks CRSP US Total Market Index. 10-year annualized return: ~12.5% (as of 2025). Ideal for broad U.S. exposure in Roth IRAs.

- Vanguard S&P 500 Index Fund (VFIAX/VOO): 0.04% fee. Mirrors S&P 500. 10-year return: ~13.2%. Core holding for 401(k)s chasing large-cap growth.

- Fidelity ZERO Total Market Index Fund (FZROX): 0% fee. No-minimum U.S. total market fund. Since inception (2018), ~14% annualized. Game-changer for cost-conscious investors.

For international diversification, add Vanguard Total International Stock Index (VTIAX/VXUS) at 0.11%, with 5-year returns ~7% amid emerging market rebounds.

Best ETFs for High-Growth in Tax-Advantaged Accounts

ETFs trade like stocks with intraday liquidity, suiting 401(k) self-directed options and Roth conversions.

- Vanguard S&P 500 ETF (VOO): 0.03% expense. AUM $1.2T+. 2025 YTD: +28%. Staple for aggressive growth.

- Invesco QQQ Trust (QQQ): 0.20% fee. Nasdaq-100 focus. 10-year return: ~18%. Tech-heavy for young investors' Roth IRAs.

- iShares Core MSCI Total International Stock ETF (IXUS): 0.07%. Global ex-U.S. exposure. Balances U.S. dominance.

Fixed-income ETFs like Vanguard Total Bond Market ETF (BND) (0.03%, 5-year return ~1.5%) stabilize portfolios as rates normalize.

Mutual Funds: Actively Managed Picks with Proven Track Records

While passive reigns, select active mutual funds outperform in niches.

- Fidelity Contrafund (FCNTX): 0.41% fee. Large-growth focus. 10-year return: ~15.1%. Leverages manager Will Danoff's tech bets.

- Vanguard Wellington Fund (VWELX): 0.25%. Balanced stock-bond mix. 10-year return: ~9.5%. Conservative choice for nearing-retirees.

- T. Rowe Price Blue Chip Growth (TRBCX): 0.70%. Mega-cap growth. 10-year: ~14.8%.

Check Vanguard's investor site for latest prospectuses.

Matching Funds to Risk Profiles and Diversification Needs

Align investments with age, timeline, and tolerance:

- Aggressive (20s-40s): 80-100% equities. 60% VOO/QQQ, 20% VXUS, 20% growth mutuals. Targets 10-15% returns.

- Moderate (40s-50s): 60% stocks (VOO/VTI), 30% international/bonds (BND/IXUS), 10% balanced (VWELX). Aims for 7-10%.

- Conservative (50s+): 40% equities (VTSAX), 50% bonds (BND), 10% cash equivalents. Seeks 4-6% with capital preservation.

Use the Fidelity planning tools for personalized risk assessments.

Optimal Allocation Strategies for 2026

Employ a "core-satellite" approach: 70% in broad index funds/ETFs (core), 30% in sector/high-growth (satellite).

- Assess Total Portfolio: Aim for 60/40 stocks/bonds globally.

- Rebalance Annually: Sell winners, buy laggards to maintain targets.

- Dollar-Cost Average: Invest fixed amounts monthly to mitigate volatility.

- Tax Efficiency: Place bonds in 401(k)s, growth in Roths. Per IRS guidelines, maximize contributions ($7,000 Roth IRA/$23,500 401(k) under 50).

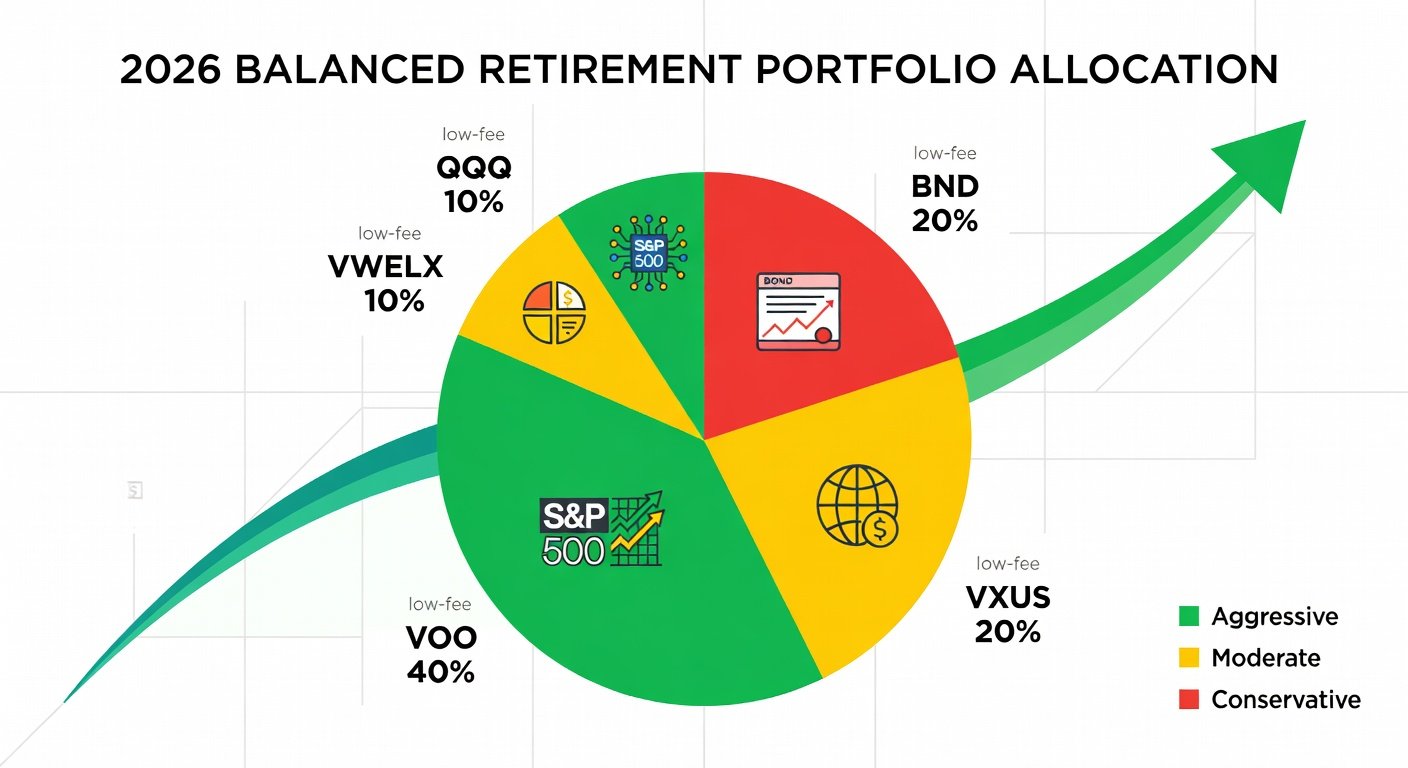

Sample Moderate Portfolio: 40% VOO, 20% VXUS, 20% BND, 10% QQQ, 10% VWELX. Backtested 10-year return: ~9.8% with 12% volatility.

Real-World Performance Data and Projections

Historical data underscores low-fee superiority:

| Fund | Expense Ratio | 10-Yr Annualized Return (to 2025) | 2026 Projection |

|---|---|---|---|

| VOO | 0.03% | 13.2% | 10-12% |

| VTI | 0.03% | 12.5% | 9-11% |

| QQQ | 0.20% | 18.0% | 12-15% |

| FZROX | 0% | 14.0% (since 2018) | 10-13% |

| BND | 0.03% | 1.5% | 4-5% |

Data sourced from Morningstar. Projections factor 2% inflation, 8% GDP growth. Active funds like FCNTX beat benchmarks by 2% net of fees.

Actionable Steps to Implement in 2026

1. Review your 401(k)/Roth balances via employer portals.

2. Open/rollover at Vanguard or Fidelity for access.3. Allocate per risk profile, rebalancing quarterly.

4. Monitor via apps, avoiding emotional trades.

Low-fee funds have historically outperformed 85% of active peers over 15 years, per S&P data. Start today for compounded gains into retirement.

No comments yet. Be the first!