Bullish Portfolio

Bullish Portfolio

Introduction to 2026 Retirement Tax Optimization

Retirement planning in 2026 requires sophisticated tax strategies beyond standard contribution limits. High-income investors can leverage Roth IRA and 401k vehicles to reduce lifetime tax burdens through careful timing and account management. This guide provides actionable tactics for conversions, required minimum distributions, and strategic contributions that go far beyond basic rules. Investors must consider inflation adjustments to limits, evolving IRS guidelines, and their unique income trajectories to build truly tax-efficient retirement portfolios.

Understanding these techniques helps investors navigate changing IRS rules while maximizing tax-free growth. Effective planning starts with assessing current income levels and projected future tax brackets. Many overlook how small annual decisions compound over decades into substantial savings. This article delivers step-by-step processes, multiple real-world examples, and decision frameworks that apply across different life stages.

Key Differences Between Roth IRA and Traditional 401k Accounts

Roth accounts accept after-tax contributions with tax-free qualified withdrawals, while traditional accounts offer upfront tax deductions but tax withdrawals as ordinary income. In 2026, contribution limits and income thresholds continue to influence eligibility for direct Roth IRA contributions. The choice between the two creates opportunities for tax diversification that can protect against both rising and falling tax rates over a lifetime.

Many high earners rely on backdoor Roth strategies to bypass income limits. Combining both account types creates flexibility for tax diversification in retirement. Consider these advantages in a bulleted comparison: Roth accounts provide tax-free inheritance benefits and no required minimum distributions for the original owner, while traditional accounts deliver immediate tax relief that can be reinvested elsewhere. Investors should evaluate their expected tax rate in retirement versus today before committing exclusively to one type.

Strategic Timing for Roth Conversions in 2026

Roth conversions involve moving funds from traditional accounts to Roth accounts, paying taxes on the converted amount. Optimal timing occurs in years with lower taxable income, such as during career transitions or before Social Security begins. The decision requires forecasting multiple years of income to avoid bracket creep and Medicare surcharges.

Step-by-step process: 1) Calculate projected taxable income for the year using detailed spreadsheets that include wages, investment income, and deductions. 2) Determine the amount to convert without pushing into a higher bracket by testing several conversion sizes. 3) Execute the conversion by December 31 and track the five-year seasoning period for each conversion. 4) Pay conversion taxes from non-retirement funds to preserve account balances and allow more money to grow tax-free.

Partial conversions over multiple years often outperform large single-year moves by managing bracket creep effectively. For instance, an investor might convert $40,000 annually for five years instead of $200,000 in one year, staying within lower tax brackets each time and reducing overall tax paid on the conversions.

Managing Required Minimum Distributions (RMDs)

RMDs from traditional accounts begin at age 73 for most individuals in 2026. These taxable distributions can push retirees into higher brackets and trigger Medicare premium surcharges. Proactive management involves projecting RMD amounts years in advance and layering strategies that reduce the balance subject to these rules.

Strategies include converting to Roth accounts before RMD age, using qualified charitable distributions to satisfy RMDs without adding taxable income, or delaying Social Security to offset RMD income. Roth accounts have no RMDs during the owner's lifetime, preserving tax-free growth. Additional tactics involve rolling over 401k funds into IRAs for greater investment flexibility and then executing targeted conversions in low-income years after retirement but before RMDs start.

IRS retirement plan resources provide official guidance on RMD calculations and exceptions that change periodically.

Leveraging After-Tax Contributions and Mega Backdoor Roth

After-tax contributions to 401k plans allow high earners to exceed standard elective deferral limits. The mega backdoor Roth converts these after-tax funds into Roth accounts through in-plan rollovers or separate Roth IRA contributions. This approach requires careful coordination with plan administrators and attention to earnings that accrue between contribution and conversion.

Implementation steps: Confirm plan allows after-tax contributions and in-service withdrawals. Maximize employee deferrals first. Contribute maximum after-tax amounts. Convert to Roth promptly to avoid earnings taxation. Monitor the plan's specific rules around timing and frequency of conversions to stay compliant.

This tactic works best for those with employer plans supporting the feature and sufficient cash flow for larger contributions. When executed consistently over 10 to 15 years, the additional tax-free growth can add hundreds of thousands of dollars to retirement resources.

Tax-Efficient Rebalancing Techniques

Rebalancing maintains target asset allocations while minimizing tax impact. Prioritize rebalancing within tax-advantaged accounts to avoid capital gains realization. Investors should also consider directing new contributions toward underweight asset classes rather than selling existing holdings in taxable accounts.

Practical example: An investor holds 70% stocks and 30% bonds. If stocks rise to 80%, sell bonds and buy stocks inside the 401k rather than a taxable brokerage. This preserves tax efficiency. Another approach uses tax-loss harvesting in taxable accounts to offset gains elsewhere, then rebalances using new contributions to underweight asset classes while maintaining overall portfolio risk targets.

Investment Allocation Strategies Within Accounts

Placing tax-inefficient investments inside Roth or traditional accounts enhances overall after-tax returns. High-growth assets with low dividends belong in Roth accounts to maximize tax-free compounding, while bonds generating ordinary income fit better in traditional accounts where the tax deduction offsets the income. Revisit allocations annually as contribution room and income change.

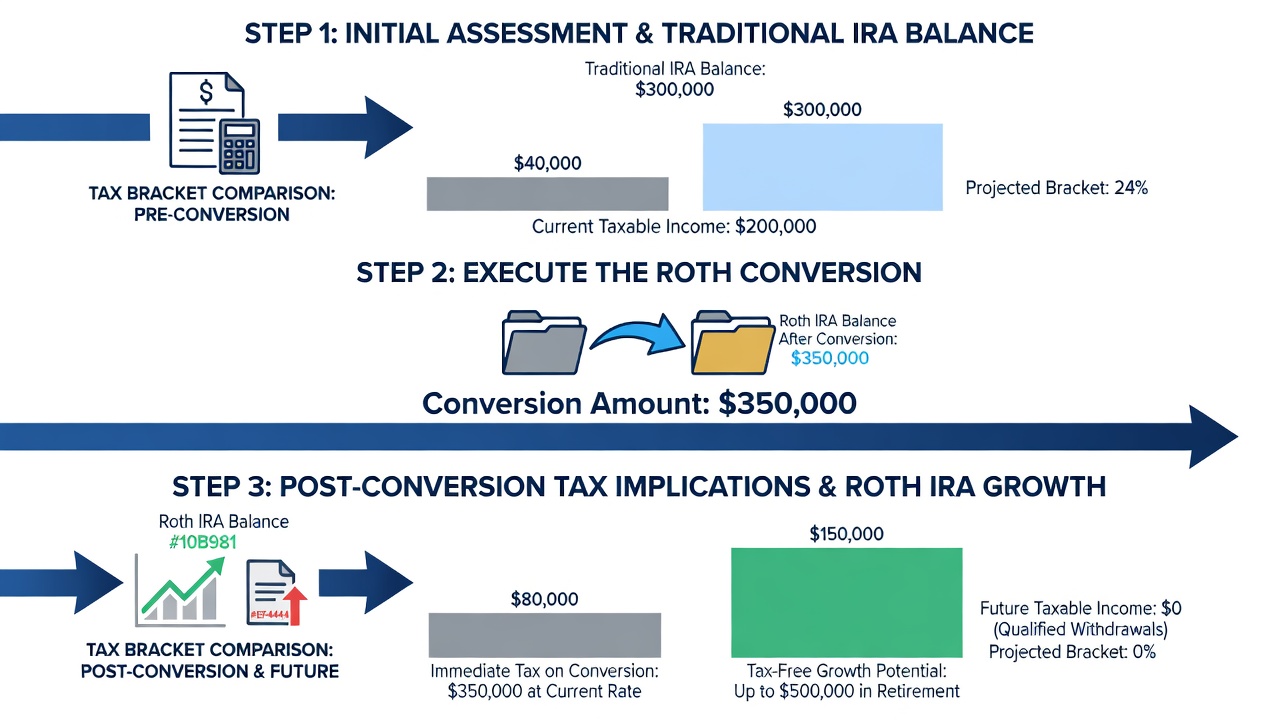

Real-World Case Studies of High Earners

Case Study 1: A 52-year-old executive earning $350,000 annually converts $80,000 from a traditional 401k to Roth IRA over two years. This move reduces future RMDs and positions more assets for tax-free inheritance while keeping annual tax bills manageable. The executive funds the tax payments from a taxable brokerage account to let the full converted amount grow tax-free.

Case Study 2: A married couple with $500,000 combined income uses mega backdoor Roth to contribute an additional $40,000 after-tax annually, converting to Roth for compounded tax-free growth over 15 years. They also execute modest annual conversions during years when one spouse takes a sabbatical, further lowering their projected RMD burden.

These examples illustrate how income level influences optimal tactics, with higher earners focusing more on conversions and backdoor strategies.

Scenario Comparisons Across Income Levels

- Moderate income ($150,000): Direct Roth IRA contributions plus standard 401k deferrals provide sufficient tax diversification with minimal need for advanced maneuvers.

- High income ($300,000+): Backdoor Roth and systematic conversions become essential to overcome contribution limits and create tax-free income streams.

- Very high income ($500,000+): Mega backdoor plus multi-year conversion ladders maximize tax-free retirement income and reduce exposure to future tax rate increases.

Comparing scenarios shows that earlier action on conversions yields greater long-term benefits due to extended tax-free compounding periods. Lower-income households benefit most from maximizing employer matches first, while higher earners should prioritize after-tax contribution features.

Common Pitfalls and 2026 IRS Rule Updates

Investors often overlook the pro-rata rule when executing backdoor Roth contributions, resulting in unexpected taxation. Another frequent mistake involves paying conversion taxes from retirement accounts instead of outside funds. Failing to track each conversion's five-year clock can also create surprises during withdrawals.

2026 updates may include inflation-adjusted contribution limits and potential changes to RMD starting ages. Always verify current rules with official sources before executing strategies. Consulting a tax professional familiar with the latest IRS notices helps avoid costly errors.

Conclusion

Tax optimization for Roth IRA and 401k accounts in 2026 demands proactive planning and precise execution. By mastering conversions, RMD management, and after-tax contribution strategies, investors can significantly reduce lifetime tax exposure while building substantial retirement wealth. Regular reviews of income projections and account balances ensure tactics remain aligned with evolving personal circumstances and tax law changes.

FAQ

What is the best age to start Roth conversions?

Many begin in their early 50s when income may dip temporarily, but the ideal timing depends on individual tax bracket projections and life events such as planned sabbaticals or business exits.

Can I undo a Roth conversion in 2026?

Recharacterizations are no longer permitted, making careful planning essential before completing any conversion and requiring accurate tax projections beforehand.

How do RMDs affect Roth accounts?

Roth IRAs and designated Roth 401k accounts have no owner RMDs, offering significant flexibility compared to traditional accounts and allowing continued tax-free growth for heirs.

Are there income limits for mega backdoor Roth contributions?

No direct income limits exist on after-tax 401k contributions, though plan-specific rules and overall contribution caps still apply and should be confirmed with the plan administrator each year.

No comments yet. Be the first!