Bullish Portfolio

Bullish Portfolio

Introduction: Navigating 2026 Market Uncertainty with Roth IRA and 401k Accounts

Market volatility in 2026 presents unique challenges for retirement savers. With economic shifts, inflation pressures, and geopolitical factors creating uncertainty, protecting your Roth IRA and 401k balances requires proactive, defensive strategies. This guide explores how to rebalance portfolios, shift toward defensive assets, and sustain contribution momentum without panic selling. Whether you have a high or low risk tolerance, these tactics help preserve capital while positioning for long-term growth. Roth IRAs offer tax-free growth and withdrawals, while traditional 401k plans provide tax-deferred contributions. Combining both vehicles strategically becomes essential during turbulent times. Investors must focus on sequence-of-returns risk, where early withdrawals during downturns can permanently damage portfolios. Understanding the interplay between these account types allows for optimized tax treatment and risk management across market cycles.

In 2026, ongoing fluctuations in interest rates and equity markets demand a disciplined approach. Rather than reacting emotionally to daily swings, successful retirement planning emphasizes long-term allocation frameworks that can withstand multiple quarters of uncertainty. This article provides concrete steps, sample allocations, and real scenarios to help you build resilience.

Understanding Sequence-of-Returns Risk in Volatile Markets

Sequence-of-returns risk occurs when poor investment performance coincides with withdrawals. In 2026, this risk is heightened due to fluctuating interest rates and equity swings. Defensive planning involves building cash buffers and diversifying across asset classes that perform differently in downturns. For example, retirees who begin drawing from accounts during a prolonged decline may deplete principal faster than expected, leaving less capital to recover when markets rebound. To mitigate this, many advisors recommend maintaining a separate cash or short-term bond reserve equivalent to several years of living expenses within the overall retirement framework.

Both Roth IRAs and 401k accounts can be structured to reduce this risk through careful asset placement. Placing more stable holdings in accounts subject to required minimum distributions helps protect growth-oriented assets in Roth accounts, where tax-free compounding provides additional flexibility.

Rebalancing Tactics for Roth IRA and 401k Portfolios

Regular rebalancing maintains your target asset allocation. During volatility, review allocations quarterly. Sell assets that have outperformed to buy undervalued ones, keeping risk levels consistent. Use tax-advantaged accounts like Roth IRAs for rebalancing without immediate tax consequences. A practical example involves an investor whose equity allocation drifted from 60 percent to 75 percent after a strong quarter; rebalancing back to target by moving excess gains into bonds restores the original risk profile without creating taxable events.

Key steps include assessing current allocations, identifying drifts beyond 5 percent, and executing trades within contribution limits. Avoid overtrading to minimize fees. Consider setting calendar reminders and using automatic rebalancing tools available in many 401k plans. Documenting each rebalance helps track performance and maintain discipline across market environments.

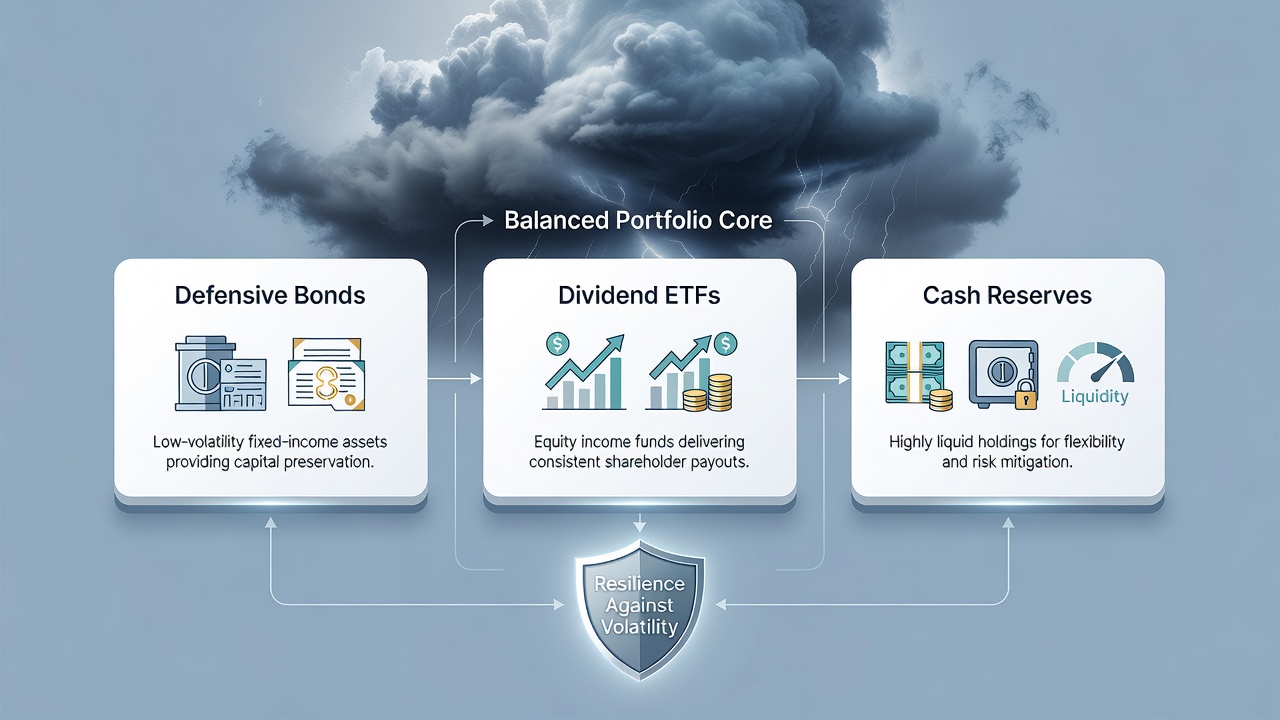

Shifting to Defensive Assets

Defensive assets such as bonds, dividend aristocrats, and low-volatility ETFs provide stability. Consider increasing bond exposure or adding Treasury inflation-protected securities. In 401k plans, target-date funds automatically adjust toward conservatism as retirement nears. Additional defensive options include utilities, consumer staples, and healthcare sector funds, which historically exhibit lower volatility than broad market indexes. Shifting gradually rather than abruptly helps avoid timing mistakes while improving downside protection.

Maintaining Contribution Momentum Without Panic Selling

Continue regular contributions even in downturns to benefit from dollar-cost averaging. Automate transfers into Roth IRAs and 401ks. Historical data shows that staying invested outperforms attempts to time the market. Investors who maintained steady contributions throughout previous volatile periods, such as 2022, often achieved lower average purchase prices and stronger recoveries. Setting up payroll deductions or automatic bank transfers removes emotion from the process and ensures consistent accumulation regardless of headline news.

Sample Portfolio Adjustments by Risk Tolerance

Portfolio construction should reflect personal circumstances including age, time horizon, and income needs. Conservative investors might allocate 60 percent to high-quality bonds, 25 percent to dividend-focused equities, and 15 percent to cash equivalents. Moderate investors could target 45 percent equities tilted toward defensive sectors, 45 percent fixed income, and 10 percent alternatives such as REITs or commodities. Aggressive investors may retain 65 percent equities with an emphasis on quality and dividends while keeping 35 percent in bonds. Revisit these targets annually or after major life events to ensure alignment with evolving goals.

Real-World Case Examples of Weathering Downturns

Consider an investor who maintained contributions through the 2022 bear market via a Roth IRA. By avoiding sales and rebalancing into bonds, their portfolio recovered faster than peers who panicked. Another example involves shifting 401k allocations to stable value funds during uncertainty, preserving principal while markets stabilized. A third case features a couple who used a Roth conversion ladder strategy during a volatile year to create tax-free withdrawal options later, demonstrating how proactive tax planning complements asset allocation decisions in uncertain environments.

Tax-Efficient Withdrawal Sequencing

Order withdrawals strategically: start with taxable accounts, then traditional 401ks (required minimum distributions), and finally Roth IRAs for tax-free growth. This sequencing minimizes lifetime tax burdens. Consult IRS guidelines at IRS.gov for current rules. In practice, a retiree might draw from taxable brokerage accounts first to allow Roth assets more time to grow tax-free, then satisfy required minimum distributions from traditional accounts before accessing Roth funds only when necessary. Modeling different sequences with tax software or a financial advisor reveals opportunities to reduce overall tax drag.

Comparing Bond Ladders Versus Dividend-Focused ETFs

Bond ladders provide predictable income through staggered maturities, reducing interest rate risk. Dividend-focused ETFs offer growth potential alongside income but carry equity volatility. For 2026, a hybrid approach in Roth IRAs often balances both benefits. Bond ladders excel in providing contractual cash flows and principal protection at maturity, while dividend ETFs may deliver higher total returns over long periods but experience price fluctuations. Learn more about market regulations at SEC.gov. Investors frequently blend both strategies, using ladders for near-term needs and ETFs for inflation-protected income growth.

Actionable Checklists for 2026 Retirement Planning

- Review current asset allocation in both accounts and document target percentages.

- Increase emergency cash reserves to 12-24 months of expenses held in stable vehicles.

- Automate contributions and rebalance quarterly using plan tools or advisor guidance.

- Evaluate defensive sector exposure in equities including utilities and staples.

- Simulate withdrawal scenarios using retirement calculators at least annually.

- Review beneficiary designations and estate planning documents for accuracy.

- Assess overall fees across Roth IRA and 401k holdings to ensure cost efficiency.

Common Pitfalls to Avoid

Investors often panic-sell during dips, chase past performance, or neglect rebalancing. Overlooking fees in 401k plans or failing to update beneficiary designations can also erode savings. Additional mistakes include concentrating too heavily in employer stock, ignoring inflation protection, and making frequent Roth conversions without considering future tax brackets. Stay disciplined and focus on long-term goals rather than short-term noise. Developing a written investment policy statement helps counteract behavioral biases during stressful market periods.

FAQ: Addressing Investor Concerns

How does volatility affect Roth IRA contributions?

Volatility does not impact contribution limits or eligibility, allowing consistent investing regardless of market conditions.

What is the best way to handle sequence-of-returns risk?

Build a cash bucket for 3-5 years of withdrawals and maintain diversified holdings across Roth IRA and 401k accounts.

Should I stop contributing to my 401k in uncertain markets?

No—continuing contributions leverages lower prices and employer matches, enhancing long-term outcomes.

How often should I rebalance during high volatility?

Quarterly reviews with a 5 percent drift threshold provide a balance between discipline and transaction costs.

Are dividend ETFs safer than broad market funds in downturns?

They tend to exhibit lower volatility but still carry equity risk; combining with bonds improves overall stability.

Conclusion

Effective 2026 retirement planning with Roth IRAs and 401ks emphasizes defense, discipline, and diversification. By implementing rebalancing, shifting to protective assets, and following checklists, investors can weather volatility confidently. Start reviewing your accounts today to secure a resilient retirement future. Regular monitoring combined with a clear strategy transforms market uncertainty into an opportunity for disciplined accumulation and preservation.

No comments yet. Be the first!