Bullish Portfolio

Bullish Portfolio

Introduction to Tax-Efficient Portfolio Management in 2026

Managing investments with taxes in mind can significantly boost long-term returns by minimizing the impact of taxes on gains and income. In 2026, investors face evolving tax rules that reward proactive strategies such as strategic asset placement and loss harvesting. This guide provides actionable steps for building and maintaining a tax-efficient portfolio while preserving strong diversification across asset classes. Effective tax management is not about avoiding taxes entirely but about legally deferring, offsetting, and minimizing them through thoughtful account selection and trading discipline. Investors who ignore these principles often see a substantial portion of their returns eroded each year by unnecessary tax liabilities, which can compound into hundreds of thousands of dollars lost over a multi-decade investment horizon.

Understanding Tax Drag and Its Impact

Tax drag refers to the reduction in returns caused by taxes on dividends, interest, and realized capital gains. Even modest annual tax costs compound over decades. Effective management focuses on deferring taxes, offsetting gains with losses, and selecting the right account types for each asset. For example, a portfolio generating 7 percent annual returns might lose 1.5 to 2 percent to taxes in a taxable account, depending on the investor’s bracket and the mix of income types. Over 30 years this difference becomes dramatic, turning what appears to be a solid performance into a noticeably smaller nest egg. Understanding where taxes arise helps investors prioritize which holdings belong in which account types and when to realize gains versus losses.

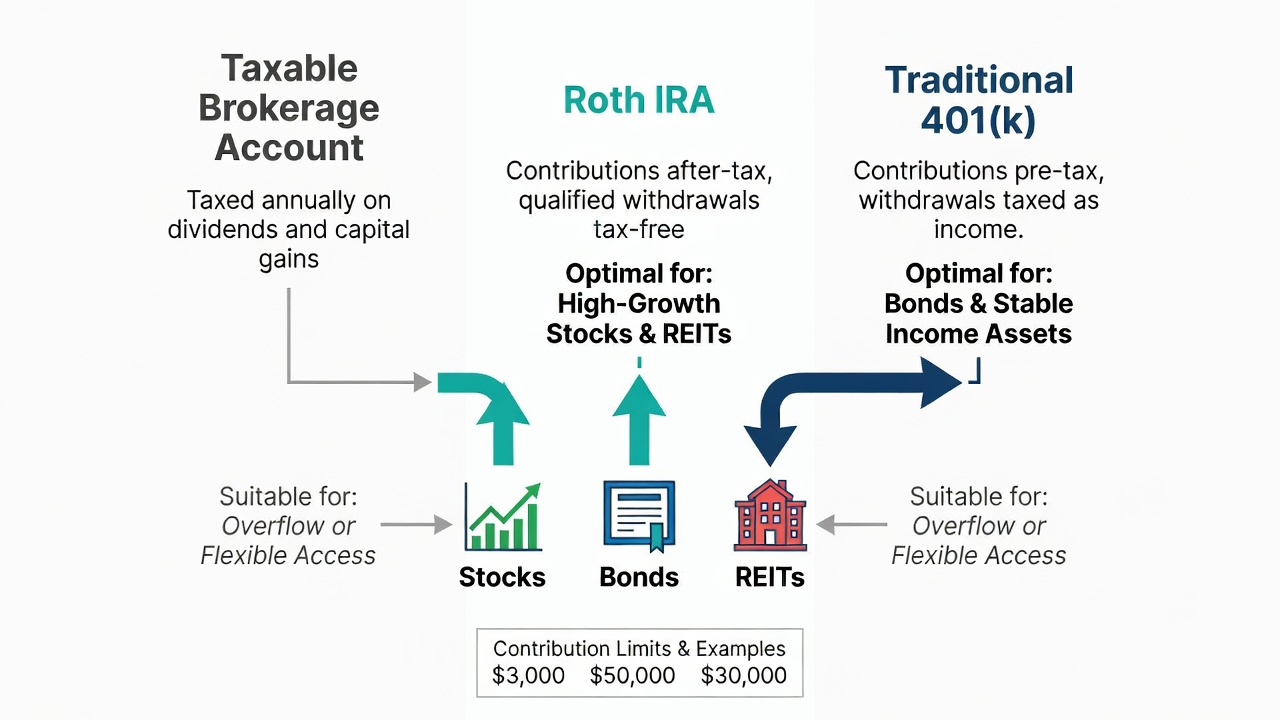

Asset Location Strategies Across Account Types

Asset location involves placing investments in taxable, tax-deferred, or tax-free accounts to maximize after-tax returns. High-growth equities often perform best in Roth IRAs or taxable brokerage accounts, while bonds and REITs suit traditional IRAs or 401(k)s due to their ordinary income tax treatment. The core idea is to match the tax characteristics of each security with the tax treatment of the account. Tax-inefficient assets that generate frequent ordinary income should be shielded inside retirement accounts, whereas assets that produce qualified dividends or long-term capital gains can remain in taxable accounts where preferential rates apply.

Step-by-step example: 1) Review current holdings and account balances. 2) Identify tax-inefficient assets like high-yield bonds. 3) Rebalance by moving them into tax-advantaged accounts during the next contribution window. 4) Monitor annually for changes in tax brackets. Consider an investor who holds corporate bonds yielding 5 percent in a taxable account. By relocating those bonds to a traditional IRA, the interest becomes tax-deferred until withdrawal, freeing up room in the taxable account for low-dividend growth stocks that qualify for lower long-term rates.

Strategic Tax-Loss Harvesting

Tax-loss harvesting offsets capital gains with realized losses. In 2026, investors should harvest losses opportunistically while avoiding wash-sale rules. Pair this with year-end portfolio reviews to capture losses before they expire. The strategy works best when executed systematically rather than emotionally. Investors should set price-alert thresholds and review positions quarterly instead of waiting for December. This disciplined approach captures losses throughout the year and prevents large concentrated sales that could disrupt asset allocation.

- Identify securities trading below purchase price by more than your chosen threshold.

- Sell to realize the loss and immediately purchase a similar but not identical asset to maintain market exposure.

- Track harvested losses to apply against future gains or up to $3,000 of ordinary income annually.

- Document every transaction for accurate cost-basis reporting.

Real-world scenario: A retiree with $50,000 in unrealized losses on individual stocks harvests them to offset $30,000 in gains from ETF sales, reducing the current-year tax bill. Another example involves a mid-career professional who harvests losses in one sector ETF and simultaneously buys a correlated but different ETF, preserving overall equity exposure while generating a usable tax offset.

Optimizing for Capital Gains in 2026

Long-term capital gains rates remain favorable compared to ordinary income. Hold qualifying assets for more than one year and time sales during lower-income years. Consider donating appreciated securities to charity to avoid gains entirely. Investors nearing retirement can plan Roth conversions or large charitable gifts in years when taxable income is lower, thereby managing the rate at which gains are realized. Another technique involves using specific identification of lots when selling shares so that only the highest-basis shares are sold first, minimizing the taxable gain on each transaction.

IRS official guidance provides the latest bracket information and forms needed for reporting.

Comparing Taxable vs Tax-Advantaged Vehicles

Taxable brokerage accounts offer liquidity and flexibility but trigger annual taxes on dividends and realized gains. Tax-advantaged accounts like IRAs and 401(k)s defer or eliminate taxes but impose contribution limits and withdrawal rules. A balanced approach often combines both for optimal results. Taxable accounts allow immediate access without penalties and provide the benefit of stepped-up basis at death, while retirement accounts protect assets from annual taxation and offer creditor protection in many states. Investors should calculate their expected time horizon and marginal tax rate to decide how much capital belongs in each vehicle type.

Real-World Scenarios for Different Investor Profiles

Young professionals: Prioritize Roth contributions for tax-free growth and locate growth stocks in taxable accounts for step-up basis benefits. They can afford higher equity allocations and should focus on maximizing tax-free space early. Mid-career investors: Use tax-loss harvesting during market dips to offset bonus-related gains and coordinate harvesting with annual bonus timing. They often have peak earning years and should shelter income-producing assets aggressively. Retirees: Shift to municipal bonds in taxable accounts and manage required minimum distributions carefully by spreading withdrawals across multiple years or using qualified charitable distributions when eligible. Each profile benefits from annual reviews that align tax strategy with changing income, spending needs, and life events.

Step-by-Step Implementation Guide

- Audit all accounts and categorize assets by tax efficiency, noting cost basis and holding periods.

- Implement location changes during low-cost rebalancing periods to minimize transaction fees.

- Set calendar reminders for quarterly loss-harvesting reviews and year-end planning sessions.

- Consult tax software or a professional to model multiple withdrawal and conversion scenarios.

- Reassess after any major life or tax-law changes such as marriage, inheritance, or new legislation.

- Document every decision and maintain records for at least seven years.

Common Mistakes to Avoid

Over-harvesting without regard to long-term allocation, ignoring state taxes, or failing to coordinate with overall retirement income planning can reduce effectiveness. Another frequent error is allowing wash-sale violations by repurchasing substantially identical securities within 30 days. Investors should also avoid concentrating too many assets in a single account type, which limits flexibility when tax rules change. Finally, neglecting to update beneficiary designations after major life events can lead to unintended tax consequences for heirs.

Monitoring, Rebalancing, and Staying Compliant

Tax-efficient management requires ongoing monitoring rather than one-time adjustments. Set up automated alerts for significant market moves that create harvesting opportunities. Review asset location whenever contribution limits change or when new account types become available. Staying compliant also means understanding foreign account reporting requirements and coordinating with estate planning documents. Professional software can flag potential issues early and generate the necessary forms for IRS filing.

FAQ

How do 2026 tax rules affect portfolio rebalancing?

Investors should monitor IRS updates for any adjustments to brackets or deduction limits and adjust harvesting thresholds accordingly. Annual rebalancing should incorporate tax impact estimates before executing trades.

Is tax-loss harvesting still beneficial with lower capital gains rates?

Yes, because it defers taxes and can offset ordinary income up to the annual limit while maintaining portfolio balance. The benefit compounds when losses are applied against higher-rate gains in future years.

What compliance steps are required for international holdings?

Report foreign accounts using IRS Form 8938 and FBAR requirements when thresholds are met. Failure to file can result in significant penalties.

Can robo-advisors handle tax-efficient strategies automatically?

Many leading platforms now include automated harvesting and location features, though manual oversight remains valuable for complex situations involving concentrated stock or real estate holdings.

How should investors handle tax changes mid-year?

Build flexibility into the plan by maintaining some cash or short-term holdings that can be adjusted quickly if new legislation alters rates or deduction rules.

Conclusion

Tax-efficient portfolio management in 2026 combines asset location, disciplined harvesting, and account optimization. By following the steps outlined above and reviewing strategies regularly, investors can reduce tax drag without sacrificing diversification or growth potential. Start with an account audit today to identify immediate opportunities and build a repeatable process that adapts to changing markets and tax laws.

No comments yet. Be the first!