Bullish Portfolio

Bullish Portfolio

Introduction to Alternative Investments in 2026

In 2026, investors are increasingly looking beyond traditional stocks and bonds to achieve better diversification. Alternative investments such as real estate, commodities, and private equity offer unique opportunities to reduce overall portfolio risk while potentially enhancing returns. This guide provides a beginner-friendly approach to integrating these assets into your core portfolio management strategy. With equity markets showing elevated valuations and bond yields fluctuating amid economic uncertainty, alternatives serve as essential tools for building resilience. Understanding their role helps investors move from basic asset allocation toward sophisticated diversification that aligns with personal goals and market realities.

Market conditions in 2026 emphasize the need for assets that exhibit low correlation with equities. By understanding risk-return profiles and correlation benefits, you can optimize asset allocation for greater resilience against inflation, geopolitical shifts, and sector-specific downturns.

Understanding Key Alternative Asset Classes

Real Estate

Real estate provides tangible assets and income through rentals or appreciation. It often shows moderate correlation to stock markets, helping stabilize portfolios during volatility. Investors can access this class through direct property ownership, real estate investment trusts (REITs), or crowdfunding platforms. In 2026, commercial and residential sectors continue to adapt to remote work trends and urbanization patterns, creating varied opportunities across regions.

Commodities

Commodities like gold, oil, and agricultural products act as inflation hedges. Their prices are influenced by supply-demand dynamics rather than corporate earnings, offering diversification benefits. Gold remains popular for its safe-haven status, while energy commodities respond quickly to global events. Futures contracts, ETFs, and mutual funds provide accessible entry points without physical storage needs.

Private Equity

Private equity involves investing in non-public companies, typically through funds. It can deliver higher returns but comes with longer lock-up periods and higher risk. Strategies range from venture capital to buyouts, targeting companies at different growth stages. This asset class often outperforms public markets over long horizons due to active management and operational improvements.

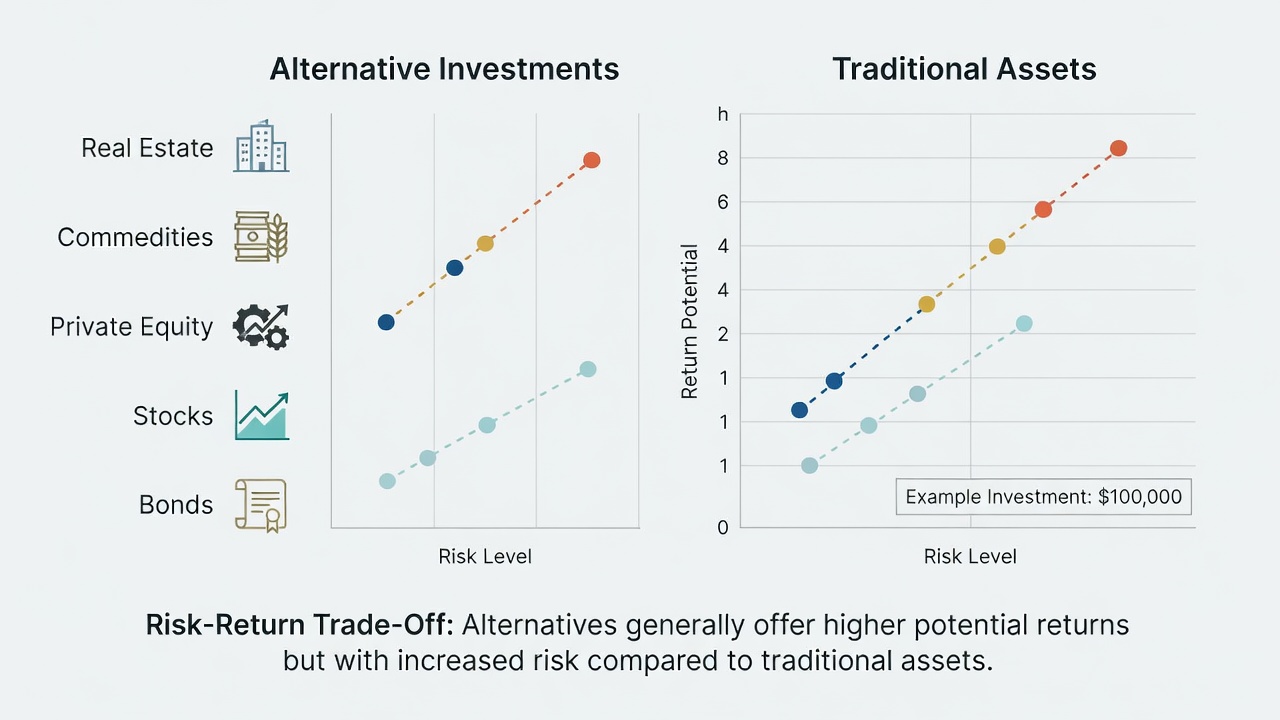

Risk-Return Profiles and Correlation Benefits

Each alternative carries distinct risks. Real estate may face interest rate sensitivity, while commodities experience price swings from geopolitical events. Private equity involves illiquidity and operational risks. However, historical data shows these assets often have correlations below 0.5 with broad stock indices, improving portfolio efficiency. For example, adding 15 percent alternatives to a 60/40 stock-bond mix has historically reduced maximum drawdowns by 10 to 15 percent in past cycles. Federal Reserve resources highlight how diversification across asset classes can mitigate systemic risks in evolving markets.

Recommended Allocation Percentages

For most investors, alternatives should comprise 10-20 percent of a diversified portfolio in 2026. A conservative approach might allocate 5 percent to real estate, 5 percent to commodities, and 5 percent to private equity, adjusting based on risk tolerance and time horizon. Aggressive investors may tilt toward 25 percent total alternatives, favoring private equity for growth potential. Always consider liquidity needs and time horizon when setting targets.

Step-by-Step Implementation Process

- Assess your current portfolio and risk tolerance using online tools or advisor consultations.

- Research specific vehicles such as REITs for real estate or commodity ETFs, reviewing expense ratios and historical performance.

- Determine allocation targets aligned with 2026 economic forecasts from reputable sources.

- Execute purchases through brokerage accounts or fund platforms, starting with smaller positions to test execution.

- Monitor performance and rebalance annually or when allocations drift more than 5 percent from targets.

Sample Portfolio Examples

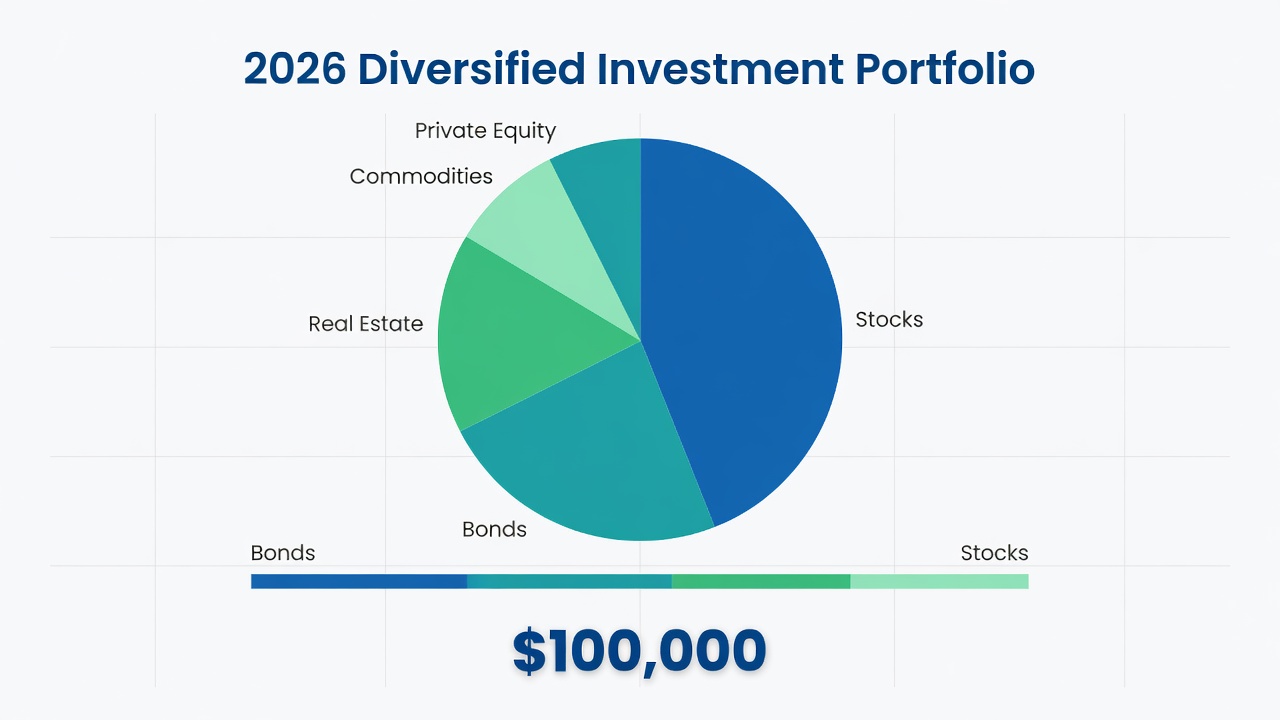

Consider a balanced investor with $100,000: 60 percent stocks, 20 percent bonds, 8 percent real estate via REITs, 7 percent commodities, and 5 percent private equity funds. This mix aims to lower volatility compared to a 100 percent traditional allocation. A retiree might use 70 percent bonds, 15 percent stocks, 8 percent real estate, 5 percent commodities, and 2 percent private equity to prioritize income and stability. Younger professionals could increase private equity to 10 percent for higher growth while maintaining 50 percent equities and 15 percent alternatives overall.

Common Pitfalls to Avoid

- Over-allocating to illiquid assets without sufficient cash reserves for emergencies.

- Ignoring fees that can erode returns over time, such as management and performance fees in private equity.

- Failing to account for tax implications in different account types like IRAs versus taxable brokerage accounts.

- Chasing past performance instead of forward-looking analysis based on current valuations and economic indicators.

Comparison Table: Alternatives vs Traditional Mixes

| Aspect | Traditional Portfolio | With Alternatives |

|---|---|---|

| Expected Volatility | Higher equity-driven swings | Reduced through low correlations |

| Inflation Protection | Limited | Stronger via commodities and real estate |

| Liquidity | High | Variable, lower in private equity |

| Return Potential | Market average | Potentially enhanced in certain cycles |

| Complexity | Low | Higher due to research needs |

SEC investor education provides further guidance on evaluating these trade-offs. Additional insights are available at Investor.gov.

Practical Tips for 2026 Markets

Stay informed on regulatory changes and use dollar-cost averaging when entering alternatives. Consult professionals for complex vehicles like private equity. Review holdings quarterly and adjust for life events such as job changes or inheritance. Incorporate environmental, social, and governance factors when selecting real estate or commodity funds to align with modern investor values.

Monitoring and Rebalancing Strategies

Effective portfolio management requires ongoing oversight. Set calendar reminders for quarterly reviews and use portfolio analytics software to track correlations in real time. Rebalance by selling outperforming assets and buying underperformers to maintain target weights. This discipline prevents drift and captures the full benefits of diversification over multi-year periods.

Conclusion

Integrating alternative investments into your 2026 portfolio can significantly improve diversification and risk management. By following structured steps, avoiding common mistakes, and maintaining disciplined monitoring, investors of all experience levels can build more robust allocations. Begin with modest positions, educate yourself continuously, and seek professional advice when needed to navigate this evolving landscape successfully.

FAQ

What are the tax implications of alternative investments?

Many alternatives generate ordinary income or capital gains, which may differ by account type. Real estate often benefits from depreciation deductions, while private equity distributions can trigger complex tax events. Always review with a tax advisor to optimize after-tax returns.

How do liquidity concerns affect alternatives?

Real estate and private equity typically have lower liquidity than stocks, meaning sales may take weeks or months. Commodities via ETFs offer better liquidity. Plan allocations to avoid forced sales during downturns and maintain emergency cash outside these holdings.

No comments yet. Be the first!