Bullish Portfolio

Bullish Portfolio

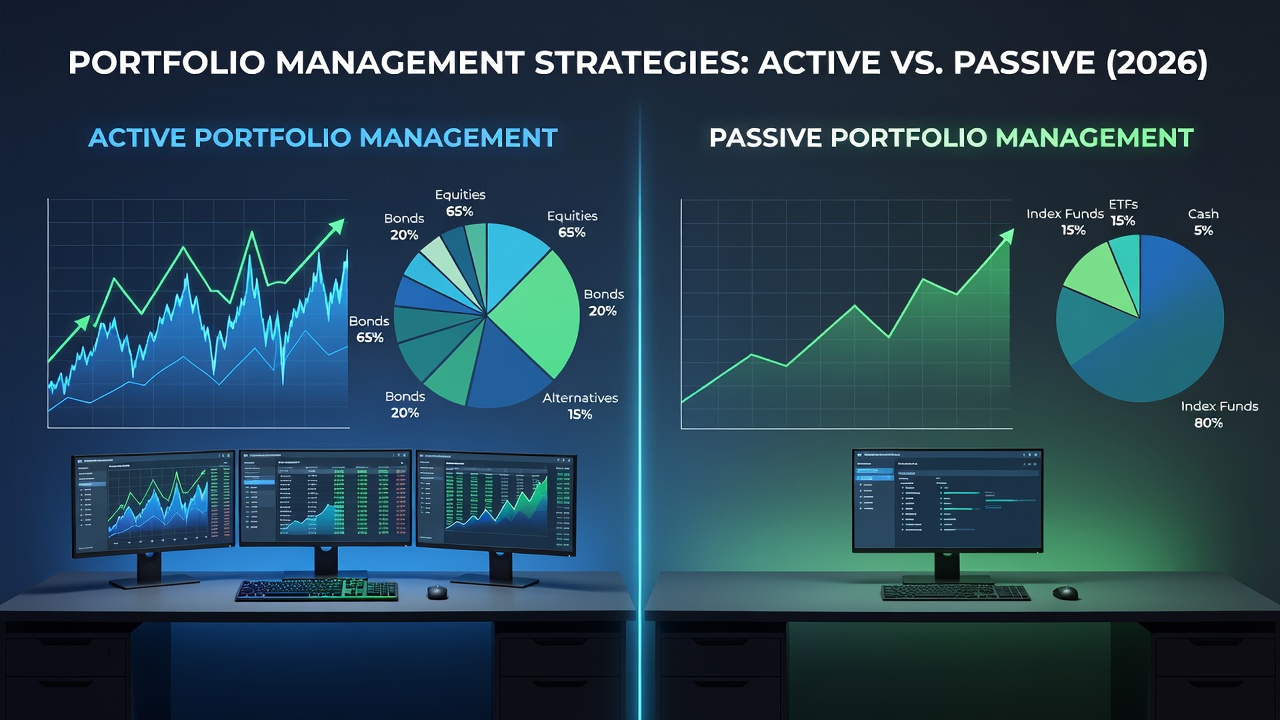

Introduction to Active and Passive Portfolio Management in 2026

Investors navigating 2026 markets face a fundamental choice between active and passive portfolio management. Active management involves professional managers selecting individual securities to outperform benchmarks, while passive management tracks market indices through low-cost vehicles like ETFs. This comparison examines their impacts on diversification, asset allocation, costs, and performance amid evolving economic conditions including interest rate adjustments and technological disruption. Understanding these approaches helps align strategies with personal goals for sustainable wealth building. Economic volatility, sector rotations, and global supply chain shifts continue to shape outcomes, making it essential to evaluate both styles thoroughly rather than defaulting to one approach.

The debate extends beyond simple returns. Diversification benefits and asset allocation efficiency play central roles in long-term success. Investors must consider how each method handles risk across equities, fixed income, and alternative assets in the current environment.

Core Differences in Strategy Execution

Active managers conduct in-depth research, analyze financial statements, and adjust holdings based on market forecasts and economic indicators. This hands-on approach aims to exploit inefficiencies but requires constant monitoring and access to proprietary data. Passive strategies, by contrast, replicate indices such as the S&P 500 or MSCI World with minimal intervention, emphasizing broad market exposure over stock picking. Execution in passive portfolios relies on rules-based rebalancing triggered by index changes rather than discretionary decisions.

Asset allocation differs significantly between the two. Active portfolios may tilt toward sectors expected to outperform based on macroeconomic analysis, whereas passive allocations follow market-cap weights that automatically adjust with price movements. Both influence diversification levels, with active potentially concentrating risk in high-conviction holdings and passive promoting broad exposure across thousands of securities. In 2026, active managers often incorporate ESG factors or thematic trends like artificial intelligence, adding layers of complexity to their process.

Cost Implications and Fee Structures

Expense ratios represent a key differentiator that directly affects net returns. Active funds typically carry higher fees due to research teams, frequent trading, and performance incentives. Passive options maintain lower costs, preserving more returns for investors over extended periods through efficient index replication. Transaction costs and tax implications also vary, with active trading potentially increasing capital gains distributions during volatile periods.

Investors should evaluate total cost of ownership, including any advisory or platform fees layered on top of fund expenses. Lower ongoing expenses in passive strategies often compound advantages in long-term holding periods, especially when markets trend upward. Understanding these structures helps prevent erosion of portfolio value from unnecessary layers of charges.

Performance Potential Under 2026 Economic Scenarios

Market conditions in 2026, including potential rate cuts, inflation moderation, and sector rotations, test both styles under varying pressures. Historical data shows passive approaches often deliver market returns minus minimal fees, while active managers may outperform in inefficient or bearish environments through defensive positioning and selective security choices. Bull markets tend to favor passive indexing due to broad participation, whereas sideways or declining markets can reward active stock selection that avoids underperformers.

Scenarios like inflation spikes or geopolitical events can favor active security selection when managers identify companies with pricing power or supply chain resilience. However, consistent outperformance remains challenging across full market cycles, leading many to consider hybrid models that capture the strengths of each style. Investors reviewing backtested results from recent years should factor in survivorship bias and changing market regimes specific to 2026.

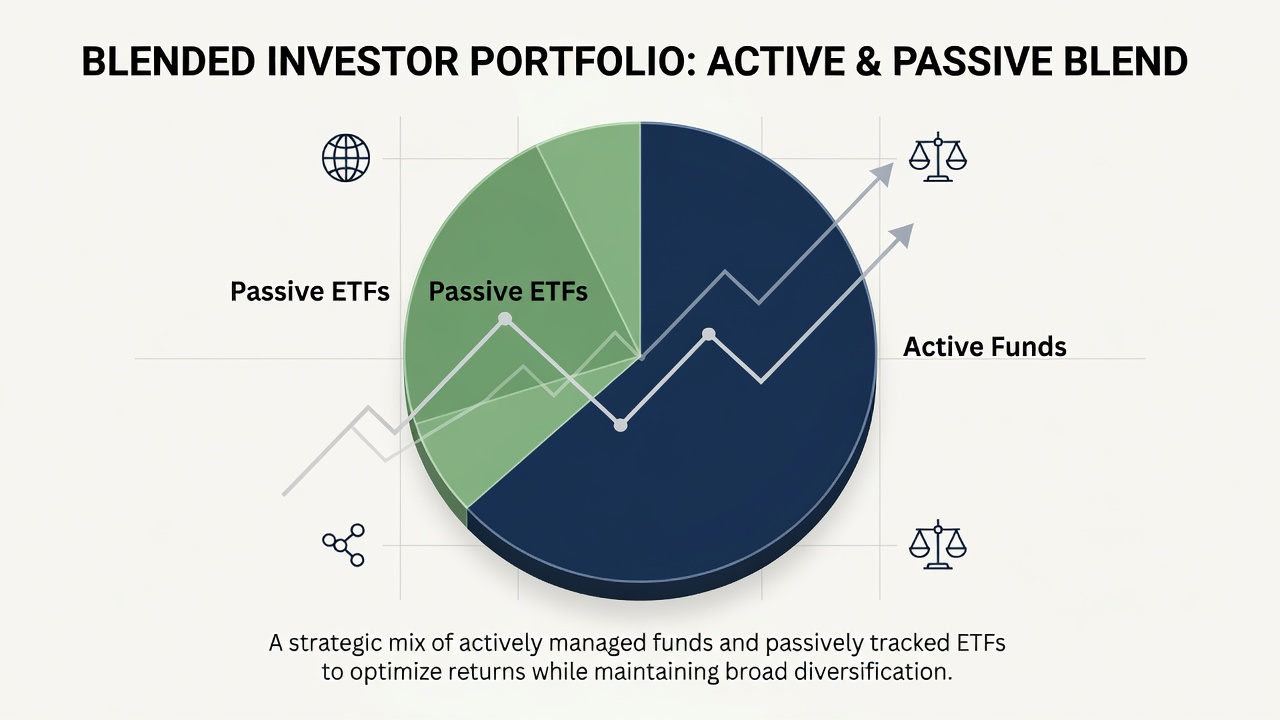

Blending Active and Passive Methods for Optimal Results

Many investors combine both styles in a core-satellite framework to balance cost efficiency with potential outperformance. The core uses low-cost passive index funds for broad market exposure and automatic diversification, while satellites allocate to active managers targeting specific opportunities like emerging markets, small-cap value, or thematic sectors. This blend enhances overall diversification and manages costs effectively while allowing tactical adjustments.

Implementation requires clear rules for allocation percentages and periodic review. Rebalancing periodically ensures allocations stay aligned with risk tolerance and market shifts without introducing excessive turnover. Investors can start with an 80/20 split and adjust based on personal objectives or changing economic signals.

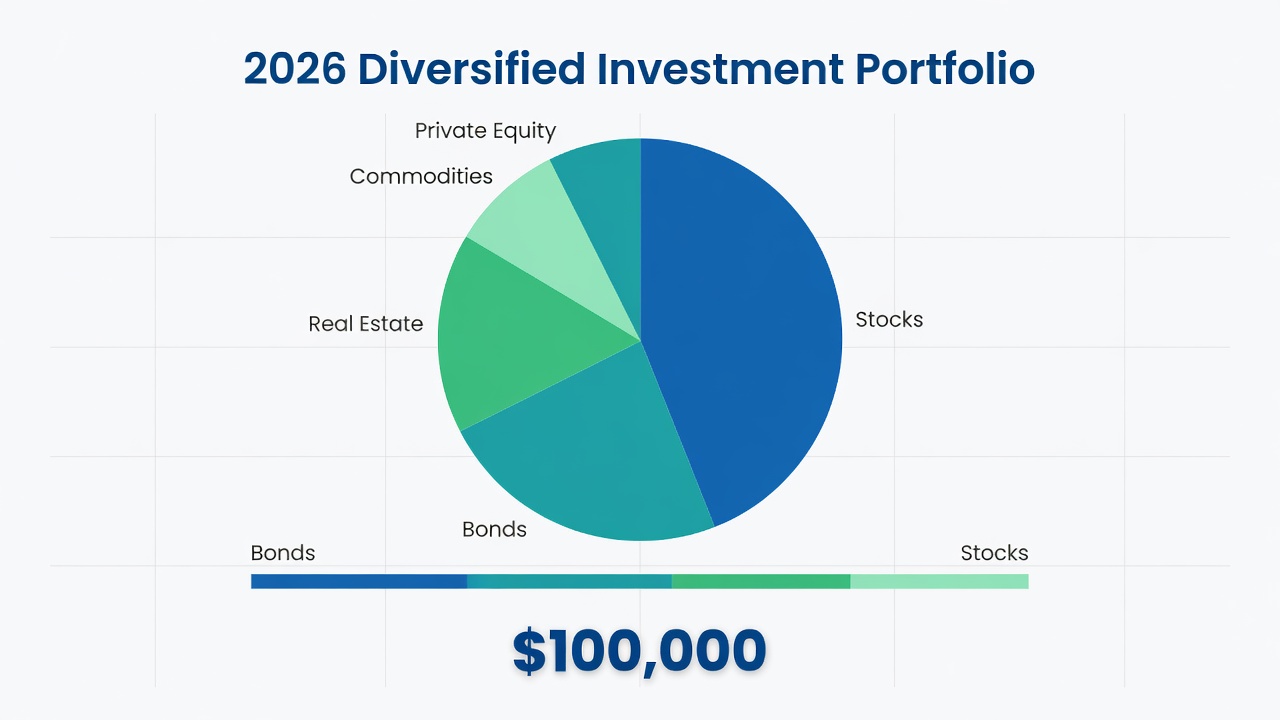

Real-World Case Studies of Investor Portfolios

Consider a moderate-risk investor allocating 70% to passive total-market ETFs covering U.S. and international equities plus bonds, with the remaining 30% in actively managed growth and value funds. During recent volatility, the passive core provided stability and low-cost market participation while active components captured upside in select technology and healthcare sectors through timely adjustments.

Another example involves retirement accounts blending broad bond index funds with actively managed equity sleeves focused on dividend growth. This setup demonstrated resilience across interest-rate cycles by maintaining income generation and capital appreciation. A third case study features a high-net-worth individual using passive core holdings for liquidity needs alongside active private equity allocations, illustrating how blending scales across different portfolio sizes and time horizons.

Step-by-Step Guidance on Implementation

- Assess your risk tolerance, time horizon, and investment goals through questionnaires or advisor consultations to establish baseline parameters.

- Determine core passive allocation using broad index products that cover major asset classes and geographic regions for foundational diversification.

- Research active managers with strong long-term track records, reasonable fees, and transparent processes using independent rating platforms and regulatory filings.

- Construct the portfolio with appropriate asset allocation across equities, fixed income, and alternatives while documenting target percentages for each sleeve.

- Implement automatic rebalancing through software tools or scheduled reviews to maintain intended risk levels without emotional decision-making.

- Review tax efficiency by considering account types such as taxable brokerage versus retirement accounts and adjust holdings as needed for changing regulations.

- Monitor performance relative to benchmarks quarterly but avoid frequent trading that increases costs and taxes.

Common Mistakes to Avoid

- Over-concentrating in high-fee active funds without clear evidence of value added over passive alternatives.

- Ignoring rebalancing needs, which can cause allocations to drift significantly from targets during strong market moves.

- Chasing recent performance instead of evaluating long-term consistency and process quality in active managers.

- Neglecting diversification across global markets, asset classes, and investment styles that passive vehicles naturally provide.

- Failing to account for behavioral biases that lead to abandoning a plan during short-term underperformance periods.

Frequently Asked Questions

How do fees impact long-term returns?

Higher fees in active management can erode compounding benefits over decades. Passive strategies generally minimize this drag through lower expense ratios that leave more capital invested in the market.

When should portfolios be rebalanced?

Annual reviews or triggers based on allocation drift of 5% or more help maintain intended risk levels without excessive trading that generates costs and taxes.

Can active management outperform in all markets?

While possible in certain conditions such as high dispersion among stocks, studies indicate passive approaches often match or exceed active results net of fees over extended periods across most market environments.

What role does diversification play in each approach?

Passive strategies inherently deliver wide diversification through index holdings, while active requires deliberate effort to avoid concentration risk and maintain exposure across uncorrelated assets.

Conclusion

Choosing between active and passive portfolio management depends on individual circumstances, market outlook, and cost sensitivity. Blending both often yields balanced results for long-term growth when executed with discipline. Consult resources from U.S. Securities and Exchange Commission, Federal Reserve, and Investor.gov for regulatory and economic insights to inform decisions in 2026 and beyond.

No comments yet. Be the first!