Bullish Portfolio

Bullish Portfolio

Introduction to Portfolio Management in 2026

Building a resilient investment portfolio requires mastering two foundational principles: diversification and asset allocation. In today's evolving economic landscape, beginners must understand how to spread risk across different investments while aligning allocations with personal goals and market shifts. This comprehensive guide provides step-by-step instructions, real-world examples, comparison tables, and actionable tips to help you create balanced portfolios that optimize returns while minimizing risks amid 2026 economic conditions. Whether you are just starting out or refining an existing strategy, understanding these concepts is essential for long-term financial success.

Defining Your Risk Tolerance

Before selecting assets, assess your risk tolerance thoroughly. This involves evaluating your financial situation, investment timeline, income stability, debt levels, and emotional comfort with market volatility. Conservative investors prioritize capital preservation and may favor lower-volatility options, while aggressive investors seek higher growth potential and can withstand larger fluctuations. To quantify your tolerance, complete risk assessment questionnaires available on major brokerage platforms or consult a certified financial planner. Consider life events such as job changes, family expansions, or nearing retirement, as these can shift your risk profile over time. A clear understanding of your risk tolerance serves as the foundation for all subsequent allocation decisions and helps prevent panic selling during market downturns.

Selecting Asset Classes

Core asset classes include equities for growth potential, fixed income for stability and income generation, real estate for inflation hedging, commodities for diversification against economic cycles, and cash equivalents for liquidity. Equities, such as stocks in domestic and international markets, offer higher expected returns but come with greater volatility. Bonds provide regular interest payments and tend to perform well when stocks decline. Real estate investments, through REITs or direct property, add tangible assets to the mix. Commodities like gold or oil can protect against inflation and currency fluctuations. Cash or short-term instruments ensure you have funds available for opportunities or emergencies. For 2026 market conditions, emphasize sectors showing resilience, including technology, renewable energy, and healthcare, while maintaining broad exposure to avoid over-concentration. Diversifying across these classes reduces overall portfolio risk because different assets often move independently in response to economic events.

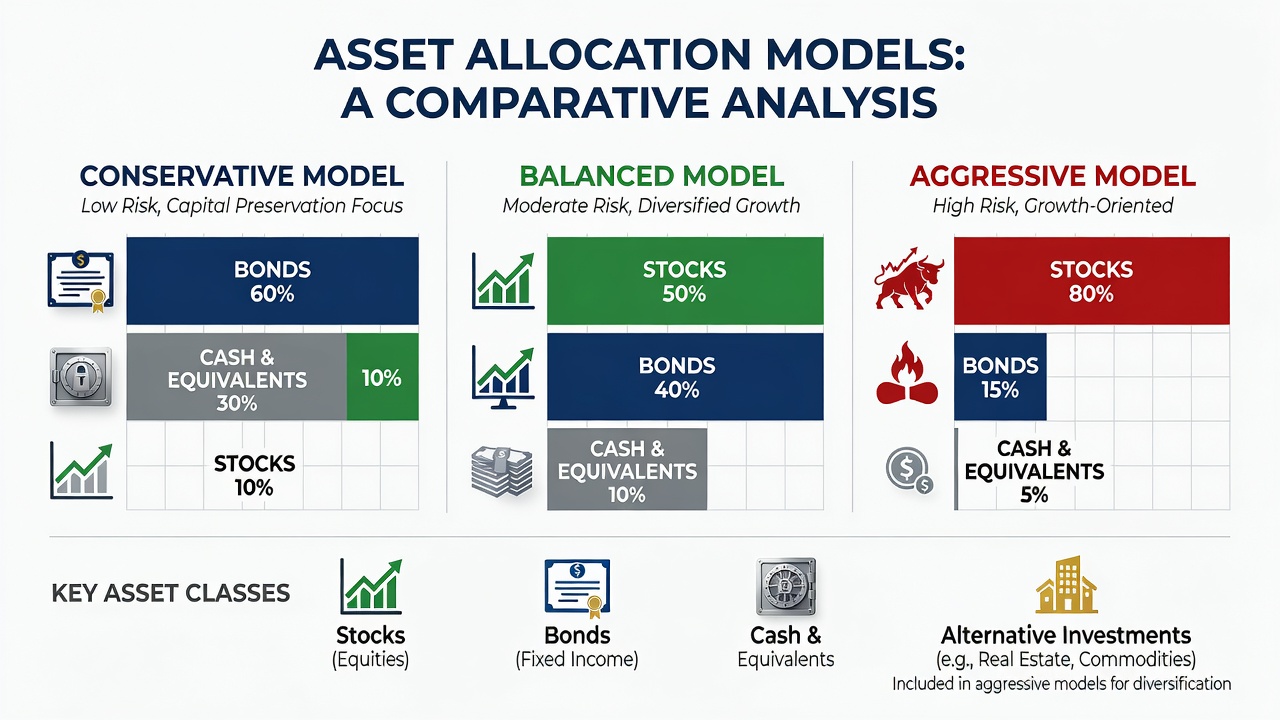

Implementing Allocation Models

Popular allocation models include the classic 60/40 stocks-to-bonds split for moderate risk, the age-based guideline of subtracting your age from 110 to determine equity percentage, target-date funds that automatically adjust over time, and factor-based approaches emphasizing value, growth, or momentum. Compare these using the following table of approaches:

| Model | Equity % | Fixed Income % | Alternative Assets % | Best For |

|---|---|---|---|---|

| Conservative | 30-40 | 50-60 | 10-20 | Capital preservation and steady income |

| Balanced | 50-60 | 30-40 | 10-20 | Moderate growth with controlled risk |

| Aggressive | 70-80 | 15-25 | 5-15 | Long-term capital appreciation |

Follow these detailed steps to implement your model: First, calculate your total net worth and identify investable assets after accounting for emergency reserves. Second, set specific target percentages based on your risk tolerance and time horizon. Third, select low-cost index funds or ETFs that track broad market benchmarks to keep expenses minimal. Fourth, execute purchases across accounts such as taxable brokerage, IRAs, or 401(k)s. Fifth, schedule annual rebalancing to restore original allocations when drifts occur due to market movements. This disciplined process ensures your portfolio remains aligned with your objectives through changing 2026 conditions.

Real-World Examples of Balanced Portfolios

Consider a 35-year-old beginner with moderate risk tolerance and a 25-year horizon. Their portfolio might allocate 55% to global equity ETFs covering large-cap, mid-cap, and emerging markets; 30% to investment-grade bond funds; 10% to real estate investment trusts; and 5% to commodity ETFs. In contrast, a 55-year-old approaching retirement could use 40% equities, 45% bonds, 10% real estate, and 5% cash equivalents to prioritize income and stability. Historical performance during past economic shifts demonstrates that such diversified mixes experienced smaller drawdowns than concentrated stock portfolios. These examples illustrate how allocation adapts to age, goals, and market environments while maintaining diversification benefits.

Monitoring and Adjusting Performance

Review your portfolio quarterly against benchmarks such as the S&P 500 for equities or Bloomberg Aggregate Bond Index for fixed income. Track metrics including total return, volatility, Sharpe ratio, and dividend yield. Use portfolio tracking software or spreadsheets to log holdings, contributions, and performance data. Adjust allocations when personal circumstances change, such as receiving an inheritance or changing jobs, or when market valuations suggest opportunities. Rebalance by selling outperforming assets and buying underperformers to maintain targets. Authoritative resources like Investopedia provide detailed calculators and educational materials to support these processes. Consistent monitoring helps capture gains and avoid prolonged exposure to underperforming segments.

Actionable Tips to Optimize Returns and Minimize Risks

Start with automatic contributions to take advantage of dollar-cost averaging. Prioritize tax-advantaged accounts to enhance compounding. Maintain an emergency fund outside your investment portfolio to avoid forced sales. Incorporate low-cost passive vehicles rather than high-fee active funds. Stay informed about macroeconomic indicators without reacting impulsively to daily news. Consider dollar-cost averaging into new asset classes gradually. These practical steps compound over time and support resilient growth in 2026 markets.

Common Pitfalls and How to Avoid Them

- Over-concentration in a single asset class or sector, which amplifies losses during downturns; mitigate by enforcing strict allocation limits.

- Ignoring ongoing fees that gradually erode net returns; always compare expense ratios before investing.

- Failing to rebalance regularly, allowing allocations to drift far from targets; set calendar reminders for reviews.

- Letting emotions drive buy or sell decisions during volatility; adhere to a written investment policy statement.

- Neglecting international diversification, which limits exposure to global growth opportunities; include at least 20-30% non-domestic holdings.

FAQ Section

What is the ideal allocation for 2026?

It depends on individual risk tolerance, age, and goals, but a balanced mix often starts around 50-60% equities for growth-oriented investors seeking resilience.

How often should I rebalance my portfolio?

Review and rebalance at least annually or whenever allocations drift more than 5% from targets to maintain intended risk levels.

Can beginners effectively use robo-advisors for allocation?

Yes, robo-advisors automate diversification and rebalancing based on your profile, making them excellent starting tools for new investors.

Should I include alternative investments like cryptocurrencies?

Limit alternatives to a small percentage, such as 5%, only after establishing core diversified holdings in traditional asset classes.

How do economic shifts affect asset allocation?

During inflation or rising rates, increase exposure to commodities and short-duration bonds while reducing long-term fixed income to preserve purchasing power.

Conclusion

Mastering portfolio management through thoughtful diversification and strategic asset allocation empowers beginners to navigate 2026 markets with confidence. By following the detailed steps, studying real-world examples, avoiding common pitfalls, and applying actionable tips, you can build wealth steadily while managing downside risks. Continue learning through trusted sources such as SEC.gov and FederalReserve.gov to refine your approach over time.

No comments yet. Be the first!