Bullish Portfolio

Bullish Portfolio

Introduction to Retirement Portfolio Management in 2026

Retirees and financial advisors in 2026 face unique challenges in balancing income generation with capital preservation. This guide provides practical, beginner-friendly techniques for building resilient portfolios that emphasize diversification across asset classes while minimizing volatility. Unlike generic advice, we focus on customized approaches tailored to the decumulation phase, incorporating inflation hedges and rigorous risk testing. Effective retirement portfolio management requires understanding the shift from accumulation to decumulation. During accumulation, investors can tolerate higher volatility for growth. In decumulation, the priority shifts to generating sustainable withdrawals without depleting principal prematurely. Market conditions in 2026 continue to highlight the importance of low-volatility strategies amid evolving interest rates and geopolitical factors. Retirees must integrate multiple asset types to create income streams that last decades while protecting against unexpected downturns.

Comparing Accumulation and Decumulation Phases

The accumulation phase typically involves aggressive equity exposure to build wealth over decades. In contrast, the decumulation phase demands a more conservative stance. Key differences include risk tolerance, time horizon, and objectives. Accumulation allows for 70-90% equities to maximize compounding; decumulation often targets 40-60% to reduce sequence-of-returns risk. Time horizons shift from 20-30 years of growth to 30-plus years of withdrawals. Objectives move from capital appreciation to income stability and preservation. Transitioning smoothly between phases involves implementing a retirement glide path that gradually adjusts allocations. For example, a worker in their 50s might maintain higher equity exposure for growth, then begin shifting five years before retirement to establish income stability.

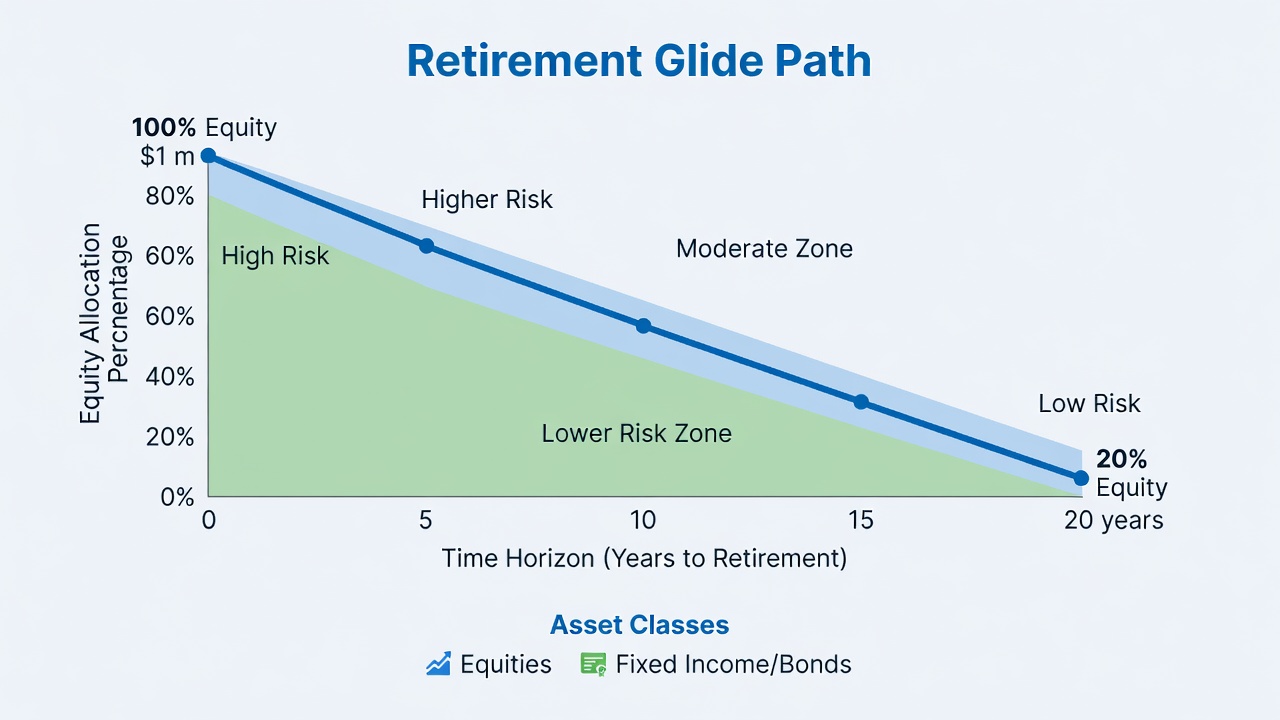

Building a Customized Retirement Glide Path

A glide path is a strategic roadmap that reduces equity exposure as retirement approaches and progresses. For 2026 retirees, consider models that start with moderate equity allocations and shift toward fixed income and alternatives. Practical example: A 65-year-old might begin with 50% equities, 35% fixed income, and 15% inflation hedges like TIPS or commodities. Over the next decade, equities could decline to 30% while increasing fixed income to 50%. This dynamic approach helps maintain diversification while adapting to changing market conditions and personal needs. Advisors often use software to model multiple glide path scenarios, incorporating life expectancy and spending needs. Retirees should review their glide path annually and adjust for health changes or market shifts.

Customized Asset Allocation Models for Low Volatility

Asset allocation is the cornerstone of diversification. Prioritize low-volatility assets such as high-quality bonds, dividend aristocrats with stable payouts, and inflation-protected securities. A sample model includes equities at 40% in broad-market index funds and defensive sectors like healthcare and utilities; fixed income at 40% in investment-grade bonds and ladders for predictable cash flow; and inflation hedges at 20% in Treasury Inflation-Protected Securities (TIPS) and real estate investment trusts (REITs). This mix aims to deliver steady income while buffering against market downturns and rising prices. Within equities, diversify across large-cap, mid-cap, and international holdings to avoid single-market concentration. Fixed income should ladder maturities to manage interest rate risk. For more on investor protections and allocation basics, consult SEC.gov.

Stress-Testing Against Sequence-of-Returns Risk

Sequence-of-returns risk occurs when poor market performance coincides with early retirement withdrawals, amplifying losses. Stress-testing involves simulating various scenarios using historical data and Monte Carlo projections. Steps for stress-testing include modeling withdrawal rates starting at 3-4% of portfolio value, applying historical downturns like 2008 or 2022 market conditions, and adjusting allocations if projected success rates fall below 80%. Real-world example: A retiree with a $1 million portfolio tests a 4% withdrawal and finds vulnerability in early years, prompting a shift to more bonds. Additional testing should incorporate rising inflation scenarios and longevity assumptions up to age 95. Tools from government resources such as FederalReserve.gov can provide current economic data for more accurate modeling.

Step-by-Step Rebalancing Workflows

Regular rebalancing maintains target allocations. Follow this workflow: review portfolio quarterly or after major market moves; identify drifts exceeding 5% from targets; sell overweight assets and buy underweight ones to restore balance; account for tax implications in taxable accounts. This disciplined process prevents over-concentration and supports long-term stability. Consider using threshold-based rebalancing instead of calendar-based to minimize transaction costs. For instance, if equities drift to 55% from a 40% target, execute trades to realign. Document all rebalancing decisions for tax reporting and future reference.

Incorporating Inflation Hedges Effectively

Inflation can erode purchasing power over long retirements. Effective hedges include TIPS, commodities, and certain REITs. Allocate 10-20% to these assets and rebalance them alongside core holdings. In 2026, monitor Treasury yields and commodity trends to fine-tune exposure. Real-world application: During periods of elevated inflation, increase TIPS allocation by selling short-term bonds to preserve real returns.

Tax-Efficient Strategies in Portfolio Management

Taxes significantly impact net returns in retirement. Hold tax-inefficient assets like REITs in tax-advantaged accounts. Use tax-loss harvesting during rebalancing in taxable accounts. Understand required minimum distributions and their effect on asset location. These strategies complement diversification by preserving more capital for income needs.

Common Pitfalls and How to Avoid Them

Many retirees fall into traps like over-concentration in dividend stocks, ignoring inflation, or neglecting fees. Diversification across uncorrelated assets mitigates these issues. Always maintain broad exposure rather than chasing high yields. Additional pitfalls include emotional selling during downturns and failing to update beneficiary designations. Create an annual checklist to review concentration limits, fee structures, and overall risk alignment.

FAQ: Retirement Portfolio Diversification

Q: How often should I rebalance my retirement portfolio?

A: Quarterly reviews with annual adjustments are typically sufficient unless significant market events occur.

Q: What role do inflation hedges play in 2026 portfolios?

A: They protect purchasing power against rising costs, complementing equities and bonds.

Q: Is professional advice necessary for glide path implementation?

A: While self-management is possible, consulting a fiduciary advisor can provide personalized modeling.

Q: How can I avoid over-concentration in dividend stocks?

A: Limit any single sector to 10-15% and use broad index funds for equity exposure.

For additional retirement resources, explore TreasuryDirect.gov and Investor.gov.

Conclusion

Implementing these diversification essentials creates a robust foundation for 2026 retirement success. Start by mapping your glide path, stress-test regularly, and maintain disciplined rebalancing. Consistent application of these techniques supports both income stability and capital preservation over the long term.

No comments yet. Be the first!