Bullish Portfolio

Bullish Portfolio

Introduction: Navigating 2026 Markets with Smart Automation

In 2026, market volatility driven by economic shifts, geopolitical events, and technological disruptions continues to challenge traditional investing approaches. Robo-advisors have emerged as powerful digital tools that leverage advanced algorithms to enhance portfolio diversification, helping investors spread risk across multiple asset classes effectively and consistently. This comprehensive guide explores how these platforms optimize asset allocation, the tangible benefits of automated rebalancing, and practical steps for beginners seeking reliable tech-driven solutions in uncertain times.

By using data-driven strategies, robo-advisors minimize human bias and maintain balanced portfolios even during turbulent market periods. Whether you are completely new to investing or looking to refine an existing strategy, understanding these systems can lead to more resilient long-term wealth building and reduced emotional decision-making.

What Are Robo-Advisors and Why Diversification Matters

Robo-advisors are sophisticated digital platforms that provide automated, algorithm-based portfolio management services. They assess your individual risk tolerance, financial goals, and investment time horizon to construct diversified portfolios typically built from low-cost exchange-traded funds (ETFs). Diversification remains one of the foundational principles of sound investing because it reduces the potential negative impact when any single asset or sector underperforms.

In the volatile markets of 2026, effective diversification means blending equities from various regions, bonds of different durations, commodities, and sometimes alternative assets like real estate investment trusts. Robo-advisors excel at this task by continuously monitoring correlations between holdings and making precise adjustments without requiring constant user intervention.

The Role of Diversification in Volatile 2026 Markets

Market conditions in 2026 feature rapid swings influenced by inflation data, interest rate decisions, and global supply chain changes. A well-diversified portfolio acts as a buffer against these fluctuations. For instance, when domestic stocks decline sharply, international equities or bond holdings may provide stability. Robo-advisors incorporate real-time economic indicators to ensure allocations remain aligned with proven diversification principles rather than reacting impulsively to headlines.

This approach draws from established investment theory that emphasizes spreading exposure across uncorrelated assets. Beginners benefit particularly because the technology handles complex calculations that would otherwise require advanced financial expertise.

Algorithm-Driven Strategies for Optimal Allocation

Modern robo-advisors employ sophisticated algorithms that analyze vast datasets, including historical returns, macroeconomic indicators, and real-time market movements. These systems generate recommended asset mixes tailored to individual profiles, such as a moderate-risk portfolio featuring 55% equities and 35% fixed income with the remaining 10% allocated to alternatives.

Practical examples include a beginner portfolio structured as 35% U.S. large-cap stocks, 15% international developed markets, 10% emerging market equities, 25% government and corporate bonds, 10% real estate, and 5% broad commodity exposure. The algorithm continuously evaluates these weights and suggests or executes changes to preserve diversification benefits as market conditions evolve.

Benefits of Automated Rebalancing

Automated rebalancing stands out as a core advantage of robo-advisors. As individual asset values rise or fall, a portfolio can drift away from its intended risk level. Robo-advisors detect this drift automatically and execute small trades to restore the original allocation, all without emotional interference or timing errors.

This process strengthens diversification by preventing any single asset class from dominating the portfolio. In 2026's fast-moving environment, such automation helps investors remain disciplined and focused on long-term objectives like retirement savings or education funding.

Comparing Top Robo-Advisors in 2026

Leading platforms differentiate themselves through varying levels of customization, tax optimization features, and access to specialized asset classes. Some emphasize ESG-focused options while others prioritize global bond exposure. Beginners should evaluate interfaces for clarity, educational content quality, and how well each platform explains its diversification methodology.

Key considerations include the breadth of available ETFs, frequency of rebalancing, and integration with external accounts. Comparing these elements side-by-side helps new users select a service that aligns with their specific diversification needs.

Steps to Get Started with a Robo-Advisor

- Evaluate your complete financial picture, including current savings, monthly cash flow, existing debts, and clear investment objectives.

- Research multiple platforms by reviewing their approach to risk assessment, available asset classes, and historical performance during previous volatile periods.

- Complete the detailed onboarding questionnaire honestly to generate an accurate risk profile and suggested allocation.

- Transfer funds from a bank account or existing brokerage and allow the system to build the initial diversified portfolio.

- Set calendar reminders to review performance summaries quarterly and update personal information after major life changes.

- Monitor educational resources provided by the platform to deepen understanding of how diversification is maintained over time.

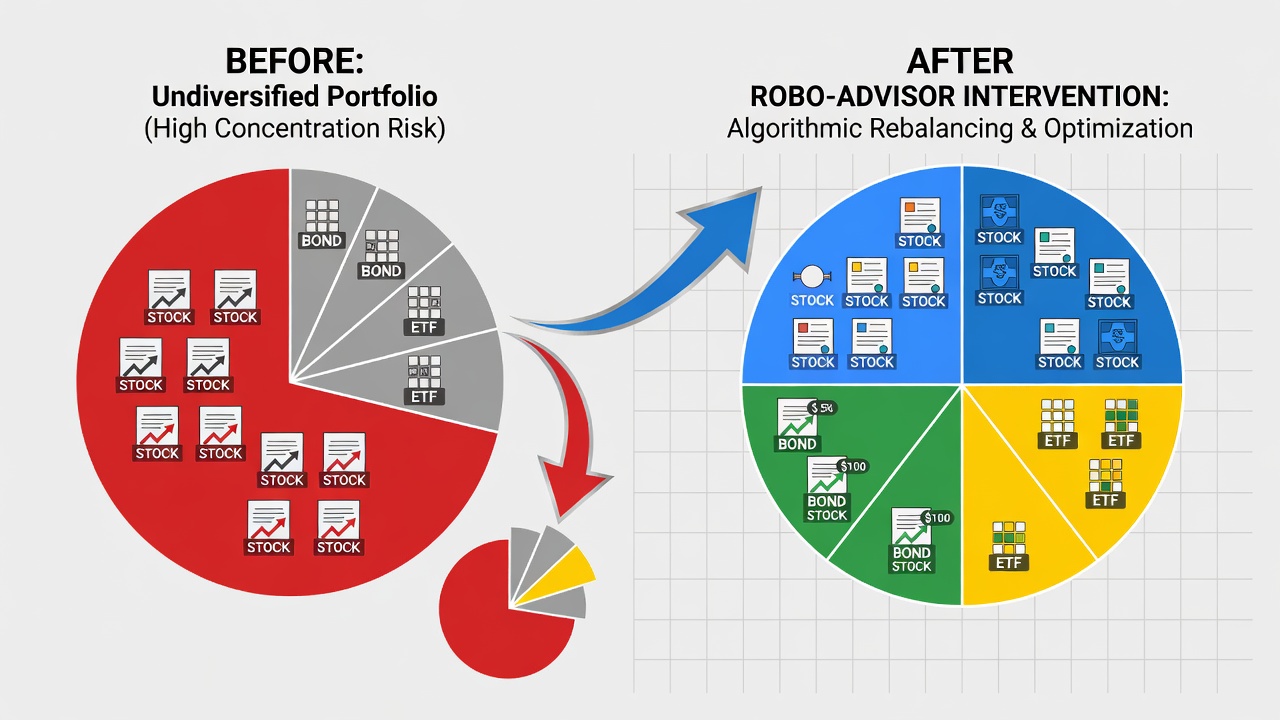

Real-World Case Studies and Asset Mix Examples

Consider the case of a 32-year-old professional beginning with moderate risk tolerance. A robo-advisor constructed a portfolio of 50% global equities (divided among U.S., European, and Asian markets), 30% investment-grade bonds, 12% real estate securities, and 8% commodity-linked ETFs. Over 18 months of market turbulence, automated rebalancing kept the equity portion within a narrow band, limiting drawdowns compared to an undiversified stock-heavy approach.

Another example involves a couple approaching retirement who shifted to a conservative mix: 65% bonds across multiple maturities and credit qualities, 25% dividend-focused equities, and 10% short-term alternatives. The platform maintained this balance through periodic small adjustments, providing steady income potential while protecting principal.

Common Mistakes to Avoid When Using Robo-Advisors

- Overriding algorithmic recommendations too frequently based on short-term market noise instead of trusting the long-term diversification model.

- Failing to update personal information such as changes in income or risk tolerance, which can lead to misaligned asset allocations.

- Expecting guaranteed returns rather than understanding that diversification reduces risk but does not eliminate market fluctuations.

- Ignoring tax implications of rebalancing in taxable accounts by not selecting platforms with built-in tax-loss harvesting capabilities.

Frequently Asked Questions

How customizable are robo-advisor portfolios?

Most services permit adjustments to overall risk levels and thematic preferences such as sustainable investing while the underlying algorithms continue enforcing core diversification rules across asset classes.

What are the typical costs involved?

Fees are generally low and based on assets under management, making these services accessible for a wide range of investors without the need for high minimum balances.

Can robo-advisors handle volatile 2026 markets effectively?

Yes, their ability to process real-time data and execute disciplined rebalancing makes them well-suited for periods of heightened uncertainty and rapid price movements.

How do robo-advisors differ from traditional financial advisors?

Robo-advisors focus on scalable, low-cost automation while traditional advisors often provide personalized human guidance for complex situations involving taxes, estates, or behavioral coaching.

Is it possible to combine robo-advisors with other investment accounts?

Many users maintain a robo-advisor for core diversified holdings while using separate accounts for individual stocks or employer-sponsored plans, allowing overall portfolio oversight.

Conclusion

Robo-advisors offer a transformative, technology-driven method for achieving strong portfolio diversification in 2026. Through algorithmic allocation, automated rebalancing, and continuous monitoring, these platforms help beginners and experienced investors alike build resilient holdings capable of withstanding market volatility. Begin exploring reputable services today to align your strategy with modern market realities and pursue sustainable long-term financial growth.

No comments yet. Be the first!