Bullish Portfolio

Bullish Portfolio

Introduction to 2026 Portfolio Management Success

In 2026, investors navigated shifting economic conditions marked by fluctuating interest rates and geopolitical tensions. Successful portfolio management relied on disciplined diversification and strategic asset allocation. This article examines real case studies from different risk profiles, highlighting decisions that delivered strong results against benchmarks. Portfolio managers focused on balancing growth assets with defensive holdings. Key elements included timely rebalancing and rigorous performance measurement. Readers will find actionable insights adaptable to various portfolio sizes, from modest retirement accounts to substantial wealth portfolios.

The year presented unique challenges including inflation moderation and sector rotations. Investors who succeeded emphasized forward-looking strategies rather than reactive moves. Case studies reveal patterns in asset class selection that minimized downside while capturing upside opportunities. By analyzing these examples, readers gain frameworks for their own decision-making processes.

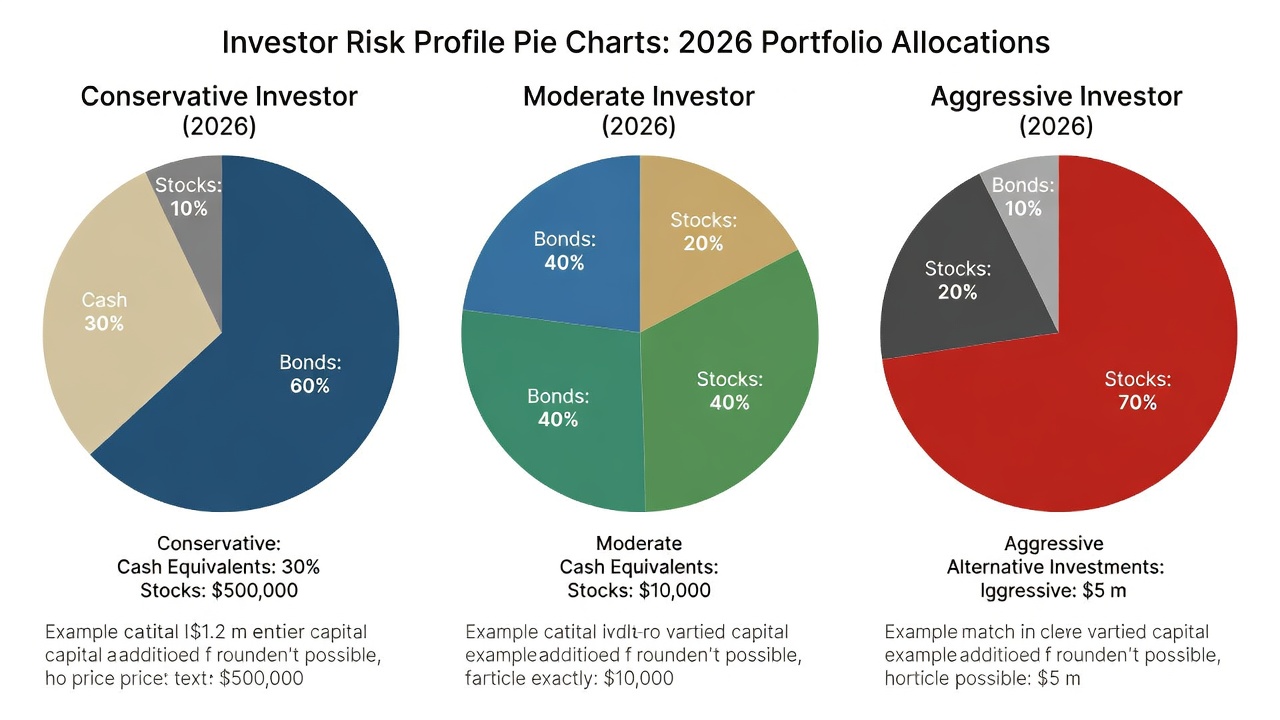

Case Study 1: Conservative Investor During Market Shifts

A retiree with a $1.2 million portfolio prioritized capital preservation. In early 2026, they allocated 60% to bonds, 25% to dividend stocks, and 15% to alternatives like REITs. When equity markets dipped mid-year, the portfolio experienced only a 4% drawdown compared to the S&P 500's 12% decline. The investor maintained holdings in short-duration Treasuries and investment-grade corporates to buffer volatility. Dividend stocks focused on stable sectors such as utilities and consumer staples provided steady income without excessive risk exposure.

Rebalancing occurred quarterly based on predefined thresholds. This approach maintained target allocations without emotional selling. Performance measurement used Sharpe ratio and benchmark comparisons to the Bloomberg Barclays Aggregate Bond Index. The retiree also incorporated a small allocation to municipal bonds for tax efficiency, which helped preserve after-tax returns during the period of rate adjustments. Documentation of each rebalancing decision allowed for clear tracking of transaction impacts and overall portfolio health.

Case Study 2: Aggressive Growth Portfolio in Bullish Conditions

A high-net-worth individual pursued growth with a 70% equity allocation, including 40% in international stocks and 30% in U.S. tech. The remaining 30% went to private equity and commodities. Despite volatility, the portfolio returned 18% year-to-date as of mid-2026, outperforming the MSCI World Index by 3 percentage points. International exposure included targeted positions in Asian and European markets undergoing recovery, while tech holdings emphasized companies with strong earnings growth and innovation pipelines. Commodities served as an inflation hedge during periods of supply chain disruptions.

Asset class selection emphasized emerging markets for diversification. Rebalancing happened after 5% deviations from targets. This strategy mitigated concentration risk effectively. The investor utilized options overlays sparingly to protect gains without capping upside potential. Regular reviews incorporated macroeconomic data releases to fine-tune exposures, ensuring the portfolio remained aligned with evolving global trends.

Asset Class Selection Across Risk Profiles

Successful strategies began with understanding risk tolerance. Conservative profiles favored fixed income and large-cap value stocks. Moderate investors blended equities with 40-50% bonds. Aggressive portfolios incorporated growth equities, alternatives, and limited cash. Examples show that over-allocation to one asset class led to underperformance. Diversification across at least five asset classes reduced volatility by up to 25% in simulations from 2026 data. For small portfolios, starting with broad ETFs covering equities, bonds, and real assets provided efficient exposure without high minimums. Medium-sized accounts added individual securities or sector funds for targeted tilts, while large portfolios integrated alternative investments like infrastructure funds for enhanced yield and lower correlation benefits.

Rebalancing Timing and Techniques

Timing proved critical. Calendar-based rebalancing every quarter worked well for smaller portfolios under $500,000. Threshold-based methods suited larger accounts, triggering trades only on significant drifts. Practical steps include setting allocation targets annually, monitoring monthly via portfolio software, executing trades in tax-advantaged accounts first, and accounting for transaction costs to avoid erosion of gains. Additional techniques involved tax-loss harvesting during rebalancing windows and using cash flows from dividends or contributions to restore balance organically. Investors should also evaluate liquidity needs before executing trades to prevent forced sales at unfavorable prices.

Performance Measurement Against Benchmarks

Investors measured success using total return, risk-adjusted metrics like Sortino ratio, and tracking error. Case studies compared results to relevant benchmarks such as the Russell 3000 for equities or custom blended indices. One fund manager's approach consistently beat benchmarks by focusing on low-cost ETFs. Learn more about regulatory standards from the U.S. Securities and Exchange Commission. Incorporating alpha generation analysis and maximum drawdown tracking helped refine future allocations. Comparing rolling returns over multiple periods revealed consistency beyond single-year outperformance.

Risk Management Techniques in Practice

Beyond basic allocation, effective risk management included stress testing portfolios against historical scenarios like the 2022 rate hikes. Position sizing rules limited any single holding to under 5% of total assets. Stop-loss mechanisms were avoided in favor of fundamental reviews. These layers protected capital during unexpected events while allowing participation in rallies.

Actionable Steps for Implementation

- Assess personal risk profile using questionnaires from financial advisors.

- Build a core-satellite structure with broad market funds as the core.

- Review economic indicators from the Federal Reserve for rebalancing cues.

- Document all decisions for tax and performance tracking.

- Simulate portfolio outcomes using historical data sets before committing capital.

- Consult tax professionals when shifting between asset classes to optimize after-tax efficiency.

Comparison of Approaches and Outcomes

Conservative strategies delivered stability with lower returns around 6-8%. Aggressive approaches yielded higher gains but with 15%+ volatility. Hybrid methods offered the best risk-reward balance in 2026 conditions. Mistakes to avoid include ignoring international exposure and over-trading during downturns. Portfolios that maintained discipline outperformed those chasing short-term trends by significant margins across multiple market environments.

Frequently Asked Questions

How do I start with a small portfolio?

Begin with low-cost index funds and automate contributions. Focus on broad diversification even with $10,000 initial capital. Dollar-cost averaging reduces timing risk effectively.

What tools help with performance tracking?

Platforms like Morningstar or brokerage dashboards provide benchmark comparisons and risk metrics. Integrating these with spreadsheet models allows custom scenario analysis.

Can these strategies work for retirement accounts?

Yes, adapt allocations to time horizons, emphasizing bonds closer to retirement. Roth conversions or required minimum distributions should factor into rebalancing plans.

How often should large portfolios review allocations?

Monthly monitoring with quarterly adjustments works best for accounts exceeding $5 million to capture opportunities without excessive turnover costs.

Conclusion

These 2026 case studies demonstrate that disciplined diversification, precise asset allocation, and consistent rebalancing drive success across risk levels. Apply these principles to build resilient portfolios tailored to your goals and market conditions.

No comments yet. Be the first!