Bullish Portfolio

Bullish Portfolio

Introduction to Portfolio Management for Beginners

Portfolio management is the disciplined process of selecting, monitoring, and adjusting a collection of investments to meet your personal financial objectives. For complete beginners, the core pillars are diversification and asset allocation, which together help manage risk while pursuing growth over time. This comprehensive guide explains these ideas in plain language, shows you how to evaluate your own risk tolerance, and walks through a practical 5-step framework you can follow today. You will also find real-world allocation examples, a ready-to-use sample portfolio, checklists for avoiding common mistakes, and guidance on ongoing monitoring. Whether you are investing for retirement, a home purchase, or general wealth building, understanding these fundamentals will give you the confidence to start and stay the course.

What Is Portfolio Management?

Portfolio management combines art and science. It requires deciding which asset classes belong in your mix, how much of each to own, and when to make changes. The goal is never to eliminate risk entirely but to align the level of risk you take with the returns you need and the sleep-at-night comfort you require. Beginners often focus first on two powerful tools: diversification, which spreads risk across many holdings, and asset allocation, which sets the overall balance between growth-oriented and stability-oriented investments.

Understanding Risk Tolerance Assessment

Risk tolerance is your personal capacity and willingness to withstand investment losses. It is shaped by your age, income stability, time horizon, existing savings, and emotional reaction to market swings. A 25-year-old with steady employment and decades until retirement can usually accept more volatility than a 60-year-old who plans to withdraw funds soon. To assess your tolerance, consider free questionnaires offered by major brokerage firms or the nonprofit resource Investor.gov. Revisit the assessment whenever your life circumstances change, such as after a job loss, marriage, or inheritance.

The Power of Diversification and Correlation

Diversification works because not all investments move in the same direction at the same time. Correlation measures the degree to which two assets rise or fall together. Assets with low or negative correlation provide the strongest diversification benefit. For example, stocks and bonds historically show modest positive correlation, while stocks and commodities may show lower correlation. A well-diversified portfolio therefore includes stocks from different sectors and countries, bonds of varying maturities and credit qualities, and a modest cash position. This structure reduces the chance that a single event devastates your entire holdings.

Asset Allocation Explained in Depth

Asset allocation is widely regarded as the most important decision an investor makes. Studies from academic and industry sources consistently show that the mix of stocks, bonds, and cash explains the majority of long-term portfolio return variability. A simple starting rule many beginners adapt is to subtract their age from 110 or 120 to estimate the percentage of equities, then adjust based on risk tolerance. More sophisticated approaches factor in expected returns, inflation, and personal goals. The key is to choose percentages you can stick with through market cycles rather than chasing the highest historical return.

5-Step Process to Build Your Initial Portfolio

- Define clear goals and time horizons. Write down what you are investing for and when you will need the money.

- Determine your risk tolerance using questionnaires and honest self-reflection about past reactions to losses.

- Select an asset allocation that matches both your goals and tolerance. Document the target percentages for stocks, bonds, and cash.

- Implement the allocation with low-cost, broadly diversified vehicles such as total-market index funds or ETFs. Automate contributions where possible.

- Establish a monitoring and rebalancing schedule. Review quarterly but rebalance only when allocations drift beyond preset bands, typically five percentage points.

Real-World Allocation Examples Across Life Stages

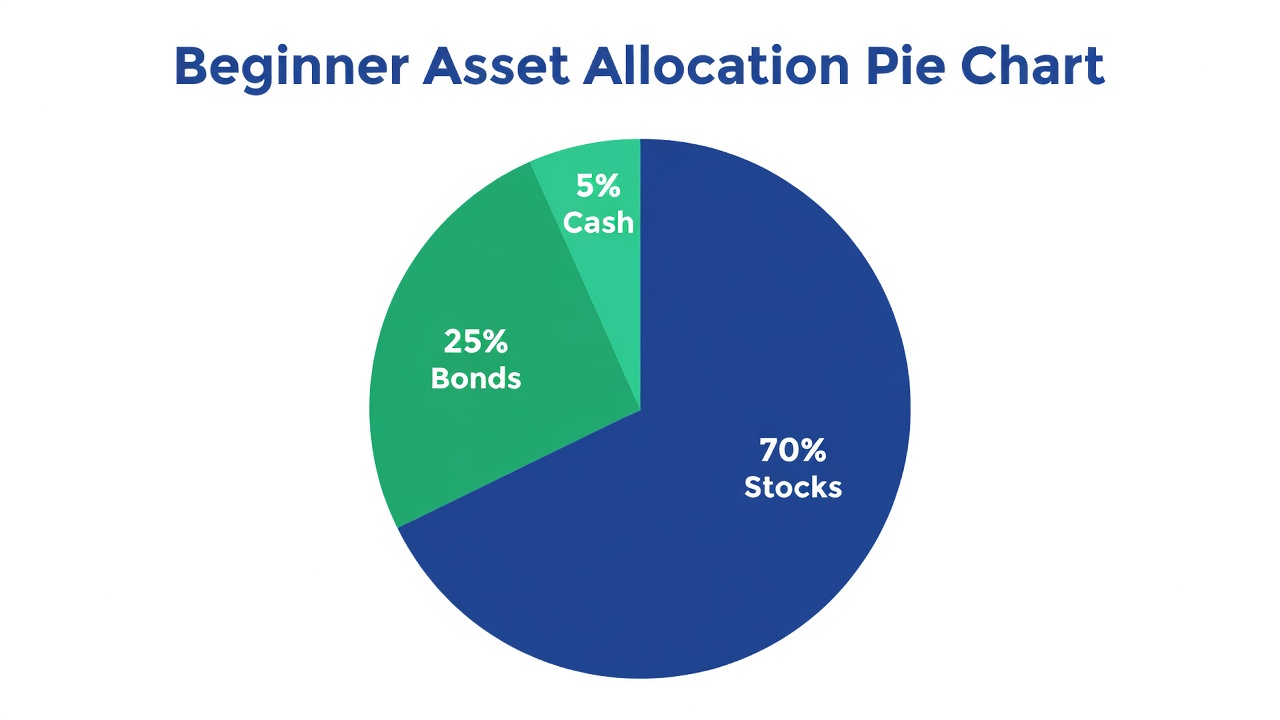

A 30-year-old moderate-risk investor might target 70 percent stocks (40 percent U.S. total market, 20 percent international developed, 10 percent emerging markets), 25 percent bonds, and 5 percent cash equivalents. A 45-year-old with higher risk tolerance could maintain 80 percent stocks and 20 percent bonds. Someone five years from retirement might shift to 50 percent stocks, 40 percent bonds, and 10 percent cash to emphasize capital preservation. These examples illustrate how allocation evolves with age and circumstances while maintaining diversification within each asset class.

Sample Beginner Portfolio Breakdown

Here is a straightforward, globally diversified starter portfolio suitable for many new investors: 40 percent total U.S. stock market index fund, 20 percent international stock index fund, 30 percent total bond market index fund, and 10 percent short-term Treasury or money-market fund. This combination delivers broad equity exposure, geographic diversification, and a meaningful fixed-income cushion. Adjust the percentages after completing your personal risk assessment.

Common Pitfalls to Avoid

- Over-concentration in a single stock or sector, often a company the investor works for.

- Ignoring fees that compound over decades and erode returns.

- Chasing recent performance instead of maintaining target allocations.

- Failing to rebalance after large market moves.

- Letting emotions drive buy or sell decisions during volatility.

- Neglecting international diversification and currency considerations.

- Starting without an emergency cash reserve outside the investment portfolio.

Monitoring Progress and Rebalancing Frequency

Quarterly reviews help you stay informed without overreacting to daily noise. Compare current allocations against targets and rebalance when any major category drifts more than five percentage points. Many investors choose a calendar approach and rebalance once per year. Track progress using free tools from your brokerage or trusted government sites such as SEC.gov. Celebrate milestones like reaching contribution goals rather than short-term performance numbers.

Frequently Asked Questions

How often should I rebalance my portfolio?

Most beginners do well rebalancing once a year or when an asset class moves five or more percentage points away from target. Avoid constant tinkering that increases costs.

What is the difference between diversification and asset allocation?

Asset allocation determines the broad mix of stocks, bonds, and cash. Diversification ensures that each of those categories contains many individual holdings rather than a few concentrated positions.

Can I start investing with a small amount of money?

Yes. Many brokerages and robo-advisors accept accounts with no minimums or very low thresholds, and fractional-share investing lets you own pieces of expensive stocks or funds.

Should I include alternative assets like real estate or commodities early on?

Most beginners achieve sufficient diversification with stocks, bonds, and cash. Add alternatives only after mastering the basics and confirming they fit your risk profile.

How do taxes affect portfolio management?

Place tax-inefficient assets such as bonds inside tax-advantaged accounts when possible. Use tax-loss harvesting strategies in taxable accounts during market downturns.

Conclusion

Portfolio management for beginners rests on two foundational concepts: thoughtful diversification and strategic asset allocation. By assessing your risk tolerance, following the five-step process, and steering clear of common pitfalls, you can construct a resilient portfolio that grows with you. Start today with small, consistent contributions, review periodically, and continue learning from authoritative sources such as Investor.gov and SEC.gov. The discipline you build now will serve you for decades.

No comments yet. Be the first!