Bullish Portfolio

Bullish Portfolio

Understanding Static vs. Dynamic Asset Allocation

In modern portfolio management, asset allocation is the cornerstone of risk management and return optimization. With 2026 projections pointing to heightened market volatility driven by rapid AI advancements and escalating geopolitical tensions, investors must choose between static and dynamic strategies. Static allocation maintains fixed percentages across asset classes like stocks, bonds, and alternatives, regardless of market conditions. Dynamic allocation, conversely, adjusts allocations proactively based on economic signals, valuations, and risks.

This comparison explores how each strategy impacts diversification, offering pros, cons, real-world examples, and a practical guide to dynamic implementation for superior risk-adjusted returns.

What is Static Asset Allocation?

Static asset allocation follows a "set-it-and-forget-it" philosophy, often based on an investor's risk tolerance and time horizon. A classic 60/40 portfolio—60% equities and 40% bonds—exemplifies this approach. It's rooted in Modern Portfolio Theory (MPT), popularized by Harry Markowitz, emphasizing broad diversification to mitigate unsystematic risk.

Pros of Static Allocation

- Simplicity: Easy to implement and maintain, ideal for passive investors.

- Lower Costs: Minimal trading reduces fees and taxes.

- Discipline: Prevents emotional decisions during market swings.

- Long-Term Reliability: Historically delivers solid returns through compounding.

Cons of Static Allocation

- Rigid in Volatility: Fails to adapt to regime shifts, like rising interest rates eroding bonds.

- Opportunity Cost: Misses tactical shifts, such as overweighting tech during AI booms.

- Diversification Limits: Fixed weights can lead to unintended concentrations amid correlated assets.

Dynamic Asset Allocation: A Flexible Approach

Dynamic allocation, also known as tactical asset allocation (TAA), involves periodic or rule-based rebalancing to exploit market inefficiencies. It uses indicators like momentum, valuation ratios (e.g., CAPE), yield curves, and volatility indexes (VIX) to tilt portfolios. In 2026, with AI disrupting sectors like semiconductors and biotech while geopolitics (e.g., U.S.-China tensions) fuels energy shocks, dynamic strategies shine by enhancing diversification through timely adjustments.

Pros of Dynamic Allocation

- Adaptability: Responds to volatility, protecting downside while capturing upside.

- Enhanced Returns: Historical backtests show 1-3% annual outperformance over static.

- Better Diversification: Rotates into uncorrelated assets during stress, like commodities amid equity selloffs.

- Risk Control: Reduces drawdowns via systematic signals.

Cons of Dynamic Allocation

- Higher Complexity: Requires monitoring and expertise.

- Increased Costs: More trading elevates expenses.

- Timing Risks: False signals can lead to whipsaws.

- Overfitting Danger: Backtested models may not predict future regimes.

Impact on Diversification Amid 2026 Market Volatility

By 2026, AI could propel a "Magnificent Seven" expansion into broader tech, but overvaluation risks loom. Geopolitics—think Taiwan Strait conflicts or Middle East escalations—may spike inflation and commodities. Static portfolios risk correlation breakdowns, where stocks and bonds fall together, as in 2022's rate-hike era.

Dynamic strategies bolster diversification by dynamically allocating to real assets (gold, TIPS) or alternatives (REITs, crypto). For instance, reducing equities below 60% during high VIX preserves capital. Studies from the CFA Institute highlight TAA's edge in volatile periods, improving Sharpe ratios by 20-30%.

Real-World Examples

During the 2020 COVID crash, static 60/40 portfolios dropped 20-30%, while dynamic funds like AQR's Style Premia shifted to trend-following, limiting losses to 10% and rebounding faster. In 2022's bear market, Bridgewater's All Weather (semi-dynamic) outperformed by favoring inflation-linked bonds.

Looking to 2026, GMO's quarterly asset allocation reports demonstrate dynamic tilts: overweighting emerging markets pre-AI slowdowns. Vanguard's research on adaptive strategies shows dynamic overlays adding 1.5% annualized returns with modest risk.

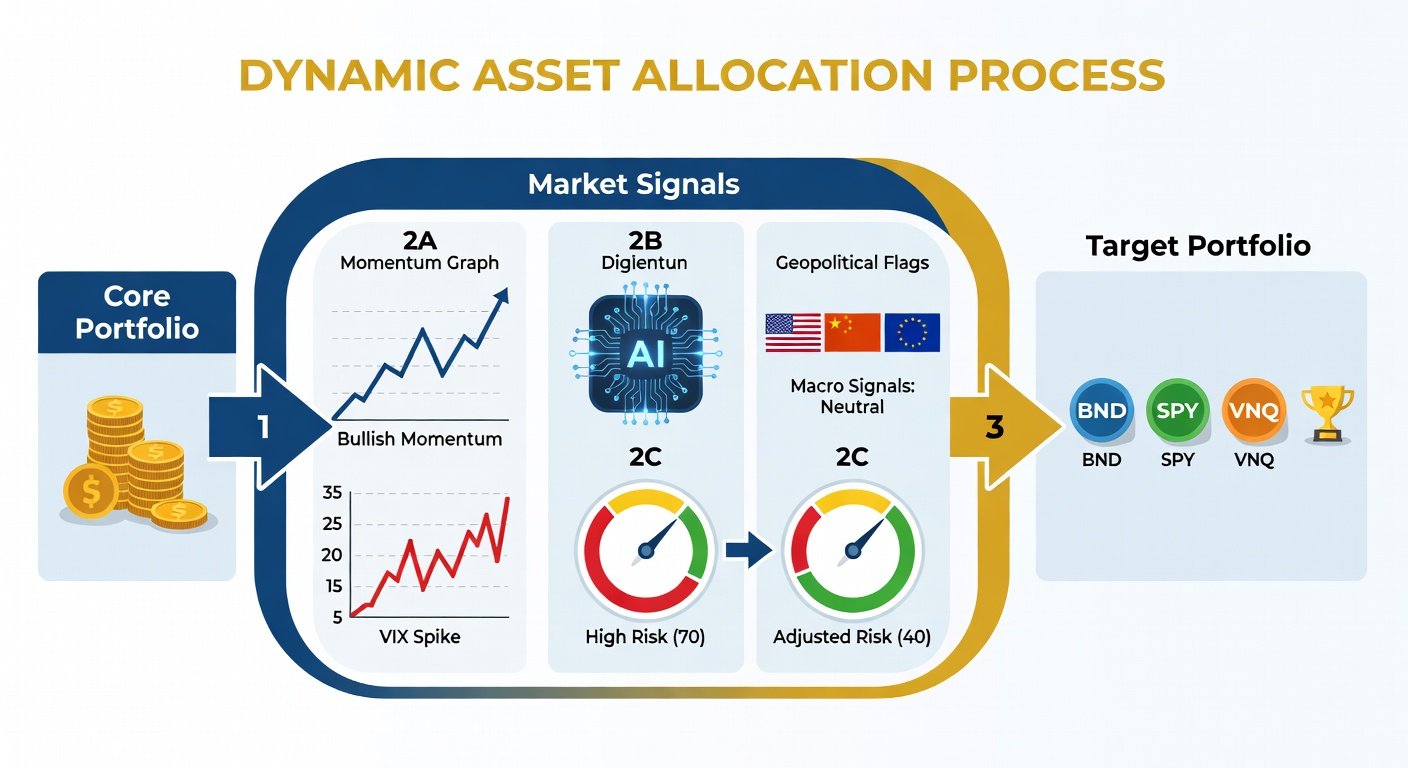

Step-by-Step Guide to Implementing Dynamic Asset Allocation

Transitioning to dynamic allocation doesn't require a hedge fund setup. Here's a practical, rule-based framework for retail investors seeking better risk-adjusted returns:

- Establish Core Static Base: Start with a diversified static portfolio (e.g., 50% global stocks via VTI/VXUS, 30% bonds via BND, 10% commodities, 10% gold).

- Select Signals: Choose 3-5 indicators: Equity momentum (12-month ROC), bond yields vs. trend, VIX >25 threshold, CAPE >30 for de-risking.

- Set Rules: Define tilts: +10% equities on positive momentum; -15% if VIX spikes. Use ETFs for liquidity (e.g., GLD for gold).

- Rebalance Quarterly: Review signals end-of-quarter; execute trades if thresholds breached. Limit turnover to <20% annually.

- Backtest and Paper Trade: Use tools like Portfolio Visualizer to simulate 10+ years, refining rules.

- Monitor and Adjust: Annually review for 2026-specific risks like AI bubbles (via NVDA weight caps) or geopolitics (energy hedges).

- Automate Where Possible: Robo-advisors like Wealthfront offer TAA overlays; or code simple bots on TradingView.

This approach balances discipline with flexibility, targeting Sharpe ratios above 1.0 in volatile environments.

Conclusion: Choose Dynamic for 2026 Resilience

Static allocation suits hands-off investors in stable times, but 2026's AI-geopolitical storm demands dynamic agility. By enhancing diversification and returns, dynamic strategies offer a clear edge. Start small, stay disciplined, and consult a fiduciary advisor. Your portfolio will thank you amid the turbulence.

No comments yet. Be the first!