Bullish Portfolio

Bullish Portfolio

Introduction to Portfolio Rebalancing in 2026

In 2026's evolving financial landscape, investors face unique challenges from shifting interest rates, geopolitical tensions, and technological advancements that influence asset performance. Portfolio rebalancing serves as a foundational strategy to maintain optimal asset allocation across stocks, bonds, and ETFs. This process ensures your portfolio remains aligned with your risk tolerance and investment objectives, preventing unintended concentration in any single asset class. By systematically adjusting holdings, rebalancing helps preserve the benefits of diversification, which can mitigate losses during market downturns and capture gains in favorable conditions. Whether you are a novice investor or managing a substantial portfolio, understanding rebalancing is critical for long-term success in dynamic markets.

Why Rebalancing Preserves Diversification

Asset classes rarely move in perfect unison, leading to drift over time. For instance, a bull market in equities might push your stock allocation from a target of 60 percent to 75 percent within months. This drift increases overall portfolio risk, exposing you to greater volatility than intended. Rebalancing counters this by selling portions of outperforming assets and reallocating to underperformers, effectively enforcing a disciplined buy-low, sell-high approach. In 2026, with potential fluctuations in bond yields and equity valuations, this practice becomes even more vital. Diversification through rebalancing reduces the impact of sector-specific events, such as tech stock corrections or energy price swings, ensuring your portfolio can weather various economic scenarios. Explore core principles of diversification on Investopedia.

Threshold vs Calendar-Based Rebalancing Methods

Choosing the right rebalancing method depends on your trading preferences, costs, and market outlook. Threshold-based rebalancing activates when an asset deviates by a predetermined percentage, commonly 5 or 10 percent from target weights. Calendar-based rebalancing occurs at regular intervals regardless of drift magnitude.

Pros and Cons Comparison

- Threshold Method Pros: It adapts to actual market movements, allowing timely corrections during rapid shifts like those possible in 2026's tech-driven rallies. This method often results in fewer trades during calm periods, preserving capital.

- Threshold Method Cons: High volatility can trigger frequent adjustments, raising transaction fees and potential tax events if not managed carefully in taxable accounts.

- Calendar Method Pros: It offers predictability, fitting well into annual financial planning routines and reducing the temptation for impulsive decisions based on short-term news.

- Calendar Method Cons: Significant drifts may accumulate between review dates, leaving the portfolio temporarily misaligned with risk goals during unexpected market events.

Hybrid approaches, where calendar checks are combined with threshold alerts, provide flexibility for most investors.

5-Step Rebalancing Process with Examples

Implementing rebalancing requires a clear, repeatable process. Here is a detailed five-step framework illustrated with practical examples involving stocks, bonds, and ETFs.

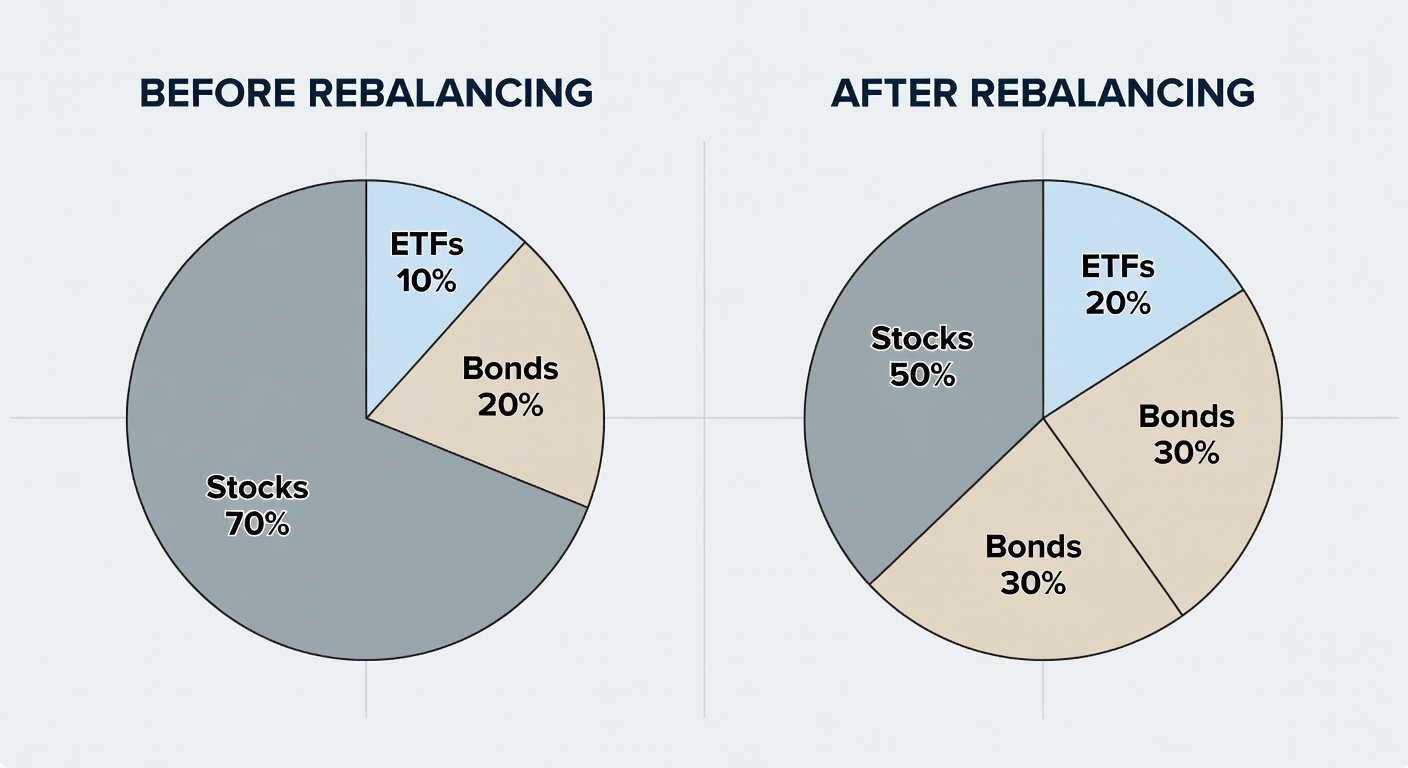

- Assess Current Allocation: Gather data from brokerage statements or portfolio trackers. Calculate percentage weights for each category. For example, review a portfolio showing 65 percent equities, 25 percent fixed income, and 10 percent international ETFs against a 55/35/10 target.

- Quantify the Drift: Determine the gap for each asset. In the example, equities are 10 percent overweight while bonds are 10 percent underweight, signaling the need for adjustment.

- Plan the Trades: Decide on specific actions such as selling equity ETFs and purchasing bond funds or individual bonds to restore targets. Prioritize holdings with the largest deviations first.

- Execute with Efficiency: Use limit orders during low-volatility periods and consider dollar-cost averaging for large adjustments. Execute in tax-advantaged accounts when possible to minimize immediate tax consequences.

- Review and Document: Log all changes, including rationale and dates, for performance tracking and tax preparation. Set reminders for the next review cycle.

This process can be applied quarterly or annually, with real-world adjustments for personal circumstances like upcoming liquidity needs.

Tools Like Robo-Advisors for Automation

Technology simplifies rebalancing through robo-advisors that continuously monitor allocations and automatically execute trades according to your specified parameters. These platforms integrate with major brokerages, offering features like automatic tax-loss harvesting and goal-based projections. For hands-on investors, spreadsheet templates or dedicated portfolio management software provide customizable alerts when thresholds are breached. Automation reduces behavioral biases, ensuring consistency even during emotional market periods in 2026. Review regulatory guidance on automated investment tools from the SEC.

Tax-Efficient Strategies

Effective rebalancing incorporates tax awareness to maximize after-tax returns. Conduct adjustments primarily within retirement accounts such as 401(k)s or IRAs where gains are deferred or tax-free. In taxable accounts, harvest losses to offset realized gains from rebalancing sales. Select tax-efficient vehicles like municipal bond ETFs or index funds with low turnover rates. Timing matters too; align rebalancing with year-end tax planning to utilize available deductions. These strategies help investors retain more wealth while staying diversified.

Common Pitfalls to Avoid

Many investors undermine their efforts through avoidable mistakes. Over-trading in response to minor drifts inflates costs and disrupts compounding. Failing to account for dividends or new contributions can skew allocations unexpectedly. Another frequent error is neglecting international or alternative assets, which limits true diversification. Emotional reactions to news headlines often lead to premature or delayed rebalancing. To avoid these, establish written guidelines and review performance metrics quarterly rather than daily. Consistent adherence to rules outperforms reactive strategies over multi-year horizons.

Case Study: Rebalanced Portfolio Outperforming Benchmarks

Consider a sample investor who began 2026 with a diversified mix of 60 percent U.S. stocks via broad ETFs, 30 percent bonds, and 10 percent international equities. By mid-year, equity outperformance shifted the allocation to 72 percent stocks. Applying the five-step process twice, including targeted sales of growth-oriented ETFs and purchases of bond and international holdings, restored balance. Over the full year, the rebalanced portfolio exhibited lower volatility and achieved steadier growth compared to an unrebalanced version that tracked a concentrated equity benchmark more closely. The disciplined approach captured gains from bonds during equity pullbacks, demonstrating how rebalancing supports resilience across market cycles.

Additional Considerations for 2026 Markets

Selecting initial target allocations requires assessing personal factors such as age, income stability, and time horizon. Younger investors might favor higher equity weights, while those nearing retirement increase bond exposure. In 2026, monitoring macroeconomic indicators like inflation trends and central bank policies aids in fine-tuning these targets. Regular education on new ETF products or bond strategies can further enhance results. Integrating rebalancing with broader financial planning, including estate considerations, creates a holistic approach.

FAQs on Frequency and Impact on Returns

How often should I rebalance in 2026? Annual reviews suffice for most, with threshold checks providing additional responsiveness during heightened volatility periods.

What impact does rebalancing have on returns? It primarily controls risk but can contribute to modest outperformance by enforcing systematic profit-taking and reinvestment.

Are there costs involved? Focus on low-expense platforms and efficient execution to ensure benefits exceed any associated fees or taxes.

Can beginners implement this? Yes, starting with simple calendar methods and robo-advisors builds confidence before advancing to custom thresholds.

No comments yet. Be the first!