Bullish Portfolio

Bullish Portfolio

Roth IRA REITs: Tax-Free Dividend Passive Income 2026

Investors seeking reliable, tax-efficient passive income are discovering the powerful combination of Roth IRAs and real estate investment trusts (REITs). This approach leverages the unique tax advantages of Roth accounts to shelter high-yielding REIT dividends and stock payouts from taxes entirely. Whether you are a beginner investor or looking to optimize your retirement strategy, understanding how to use REITs inside a Roth IRA can accelerate your journey toward financial independence. In this in-depth guide, we cover Roth IRA contribution rules for 2026, explain why this vehicle is ideal for tax-free growth, provide a detailed step-by-step setup process, and share concrete examples including popular options like the Vanguard Real Estate ETF (VNQ).

Understanding Roth IRA Rules and 2026 Contribution Limits

A Roth IRA is funded with after-tax dollars, allowing all future growth and qualified withdrawals to remain completely tax-free. There are no required minimum distributions during the account owner's lifetime, offering flexibility for estate planning. For 2026, the annual contribution limit is $7,500 for individuals under age 50 (as of 2026-05-17), plus a $1,000 catch-up contribution for those 50 and older. Income eligibility phases out at higher modified adjusted gross income levels, with single filers able to make full contributions below $146,000 in many cases. Those exceeding the limits can still benefit through backdoor Roth conversions, though careful tax planning is essential. REIT dividends, which frequently consist of ordinary income, capital gains distributions, and return of capital, receive full tax sheltering inside the Roth structure. This eliminates the annual tax reporting and payments that would otherwise reduce compounding power in a taxable brokerage account.

Benefits of Holding REITs and Dividend Stocks in a Roth IRA

REITs must distribute at least 90 percent of their taxable income as dividends, resulting in attractive yields often between 4 and 8 percent. When placed inside a Roth IRA, these distributions grow without annual taxation, dramatically enhancing long-term results. Over a 20- or 30-year horizon, the tax-free compounding can add tens or even hundreds of thousands of dollars compared to holding the same assets in a taxable account where dividends are taxed each year at ordinary income rates. Dividend aristocrats, companies with 25 or more consecutive years of dividend increases, add stability and inflation protection. The combination creates a diversified income stream that supports retirement spending without eroding principal.

Step-by-Step Guide to Opening a Roth IRA for REIT Investing

Follow these practical steps to get started. First, verify your eligibility by checking current income limits and confirming you have earned income at least equal to your planned contribution. Second, select a reputable custodian such as Vanguard, Fidelity, or Charles Schwab that offers no-commission trading on ETFs and individual REITs. Third, complete the online application, providing personal details and linking a bank account for funding. Fourth, make your contribution, ideally automating monthly transfers to stay disciplined. Fifth, research and purchase your initial REIT positions once funds clear. Many platforms provide educational resources and portfolio analysis tools to help beginners select suitable holdings. Be sure to keep records of contributions for future tax-free withdrawal planning.

Choosing Beginner-Friendly REITs and Dividend Aristocrats

Begin with diversified, low-cost options like the Vanguard Real Estate ETF (VNQ), which holds hundreds of commercial, residential, and industrial properties across the United States. For higher yields, consider individual equity REITs such as Realty Income (O), known for its monthly dividend payouts and focus on retail properties. Mortgage REITs can offer even higher yields but carry additional interest-rate risk and should be limited in allocation. Complement these with dividend aristocrats like Procter & Gamble or Johnson & Johnson, which provide lower but more stable payouts and strong total returns. When evaluating REITs, review key metrics including adjusted funds from operations (AFFO), debt-to-equity ratios, occupancy rates, and dividend payout ratios. Avoid over-concentration in any single property sector such as office or retail during economic shifts. Resources at NAREIT.com offer detailed industry data to support informed decisions.

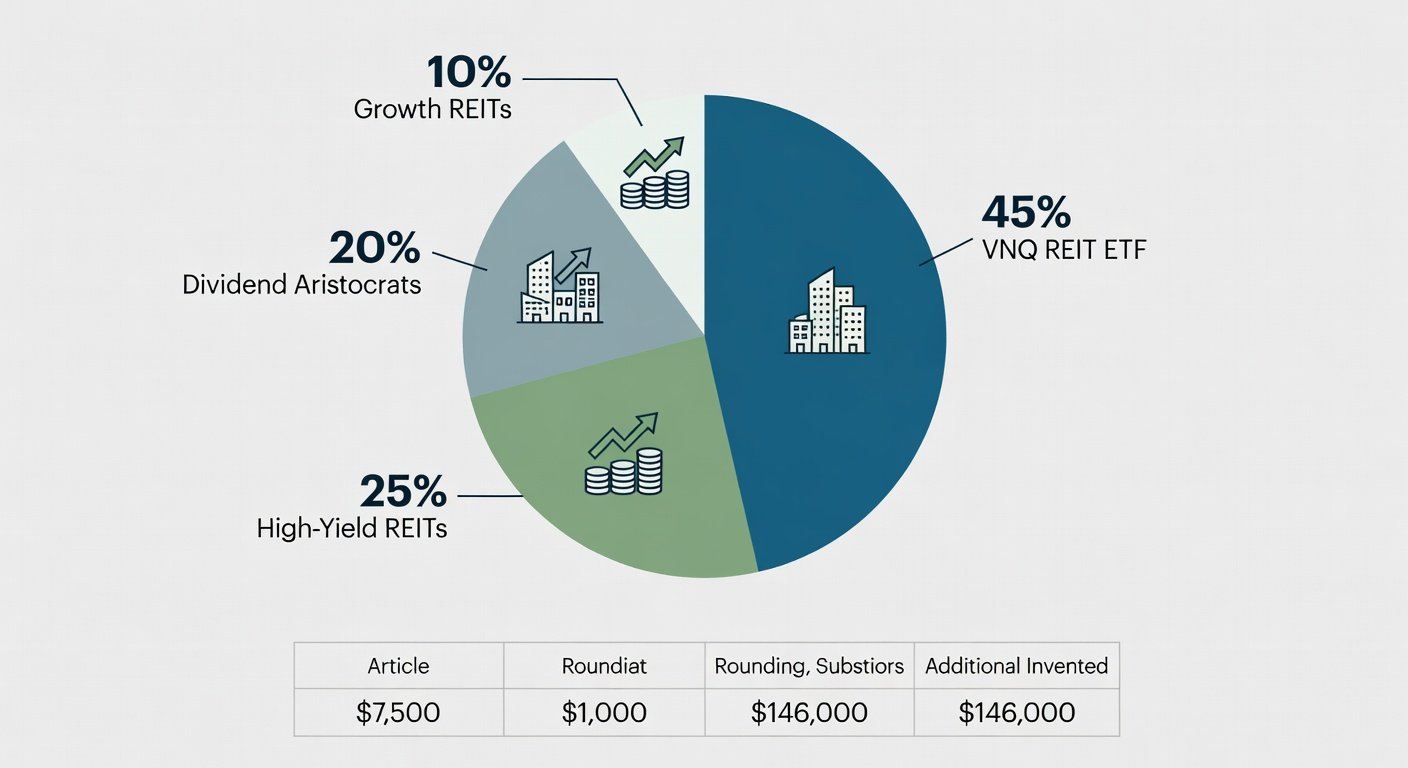

Building a Sample Portfolio Allocation for 6-8% Annual Passive Income

A well-balanced portfolio might allocate 45 percent to broad REIT ETFs like VNQ for diversification, 25 percent to high-yield equity REITs such as Realty Income or healthcare-focused trusts, 20 percent to dividend aristocrats for stability, and 10 percent to a growth-oriented REIT or ETF for capital appreciation. At current average yields, this mix can target an overall portfolio income rate of 6 to 8 percent while maintaining reasonable risk. For example, an investor contributing the maximum $7,500 annually and achieving 7 percent average total return could see the account grow substantially over 25 years through reinvested dividends. Rebalance once per year to maintain target weights and consider dollar-cost averaging new contributions. This structure supports both income generation and long-term growth within the tax-free environment.

Long-Term Compounding Benefits: Roth IRA vs Taxable Accounts

The difference in outcomes becomes pronounced over time. Assume a 6 percent annual yield with all dividends reinvested. In a taxable account, federal taxes at 22-24 percent rates could reduce the effective yield to roughly 4.5 percent. Inside a Roth IRA, the full 6 percent compounds each year. Over 30 years with consistent contributions, this tax advantage can result in 25-40 percent more wealth available for retirement spending. Historical data from broad REIT indexes demonstrates resilience through multiple market cycles when held long term, underscoring the value of the Roth wrapper for patient investors.

Potential Risks and How to Mitigate Them

REITs are sensitive to interest rate changes, economic downturns, and sector-specific issues such as declining retail foot traffic or rising vacancy rates. To mitigate these risks, maintain broad diversification across property types and geographic regions. Limit exposure to higher-risk mortgage REITs and monitor leverage levels. Regularly review holdings using tools from your custodian and consider dollar-cost averaging during market volatility. Pairing REITs with stable dividend aristocrats further reduces portfolio volatility while preserving income goals.

Frequently Asked Questions

Who qualifies to contribute the full amount in 2026?

Eligibility depends on modified adjusted gross income. Single filers typically qualify for full contributions below approximately $146,000, with phase-outs applying at higher levels.

Can I perform a backdoor Roth conversion to hold more REITs?

Yes, but conversions are taxable events. Spreading them over several years and consulting a tax professional helps manage bracket implications.

What penalties apply to early withdrawals?

Earnings withdrawn before age 59½ generally face a 10 percent penalty plus income taxes, although original contributions can be withdrawn tax- and penalty-free at any time.

How do I track cost basis for REITs inside a Roth IRA?

Cost basis tracking is unnecessary for tax purposes since qualified withdrawals are tax-free, but maintaining records still aids in performance monitoring.

Are there any contribution deadlines for 2026?

You can contribute to a 2026 Roth IRA until the tax filing deadline in April 2027, providing flexibility for year-end planning.

For the most current rules and additional guidance, consult official resources at IRS.gov and review SEC filings for individual REITs via SEC.gov. This strategy works best as part of a broader retirement plan tailored to your personal circumstances.

No comments yet. Be the first!