Bullish Portfolio

Bullish Portfolio

Introduction to Tax-Efficient Active Value Investing in 2026

Active value investing centers on identifying undervalued stocks with strong fundamentals and actively managing positions to capitalize on market inefficiencies. In 2026, integrating tax efficiency into this approach becomes critical for intermediate investors who seek to maximize after-tax returns. Markets continue to present opportunities in sectors such as financials, energy, and consumer staples where temporary mispricings occur due to macroeconomic shifts. However, frequent trading in taxable accounts can erode gains through short-term capital gains taxes that reach ordinary income rates. This article provides in-depth guidance on blending active tactics with value principles while minimizing tax drag. Readers will find step-by-step implementation guides, multiple real-world portfolio examples, comparisons to standard buy-and-hold methods, and compliance considerations aligned with current IRS frameworks.

Tax-efficient strategies do not require abandoning active management. Instead, they involve deliberate timing of sales, strategic account allocation, and ongoing monitoring of both fundamentals and tax implications. Investors who master these techniques often achieve superior net performance compared to those who focus solely on pre-tax returns.

Understanding Tax-Loss Harvesting in Value Portfolios

Tax-loss harvesting allows investors to sell positions at a loss to offset realized capital gains, thereby reducing current-year tax liability. Within active value portfolios, this technique proves especially useful because undervalued holdings can experience short-term price declines even when long-term prospects remain intact. The key lies in harvesting losses without permanently exiting attractive opportunities.

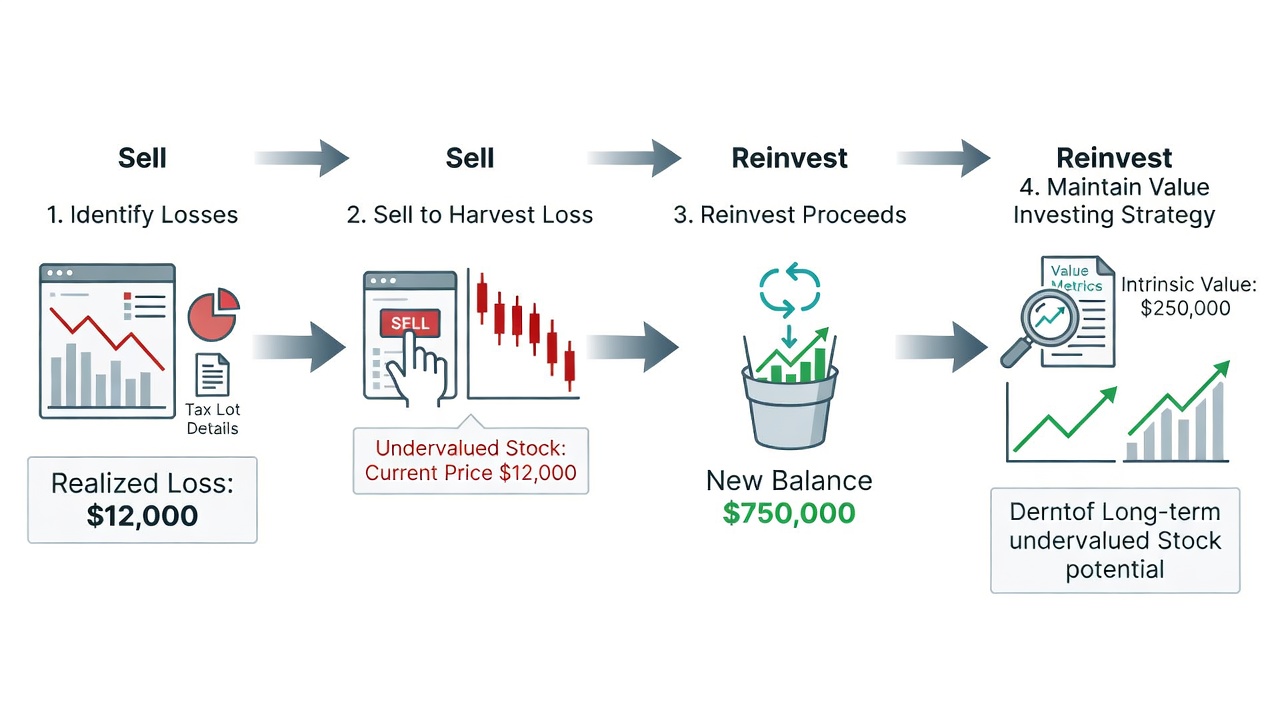

Step-by-step implementation begins with a quarterly portfolio review. Identify holdings where the current market price sits below the cost basis and where the original value thesis has weakened or shifted. Next, confirm that the loss can be realized without violating the wash-sale rule, which disallows the loss if a substantially identical security is repurchased within 30 days before or after the sale. Then, sell the losing position and immediately allocate proceeds to a similar but non-identical security in the same industry or with comparable valuation metrics. Finally, document every transaction with dates, prices, and rationale for future tax reporting.

Consider this detailed example: An investor purchased 500 shares of a regional bank trading at a 30 percent discount to book value. After six months the shares declined another 25 percent due to sector rotation. The investor sells at the lower price, generating a $12,000 loss that offsets gains from another value position sold earlier in the year. Proceeds move into an exchange-traded fund focused on small-cap value stocks that exhibits similar characteristics but avoids direct wash-sale overlap. This adjustment preserves exposure to the value premium while generating a usable tax benefit.

Compared with standard approaches that ignore harvesting opportunities, this method can improve after-tax compounding by several percentage points annually when applied consistently across multiple positions.

Deferring Capital Gains Through Strategic Holding Periods

Long-term capital gains receive preferential tax treatment once an asset has been held longer than one year. Active value investors must balance the desire for tactical adjustments against the tax cost of short-term realizations. Deferral strategies include partial sales after the long-term threshold, using options or collars to hedge exposure without triggering a taxable event, and rotating capital within similar value themes only when fundamentals materially deteriorate.

Real-world comparison: A standard active value approach might sell a position after nine months once it reaches fair value, incurring short-term rates near 37 percent plus state taxes. In contrast, a tax-efficient version waits an additional three months, qualifies for long-term rates around 20 percent, and simultaneously monitors peer valuations to redeploy capital efficiently. This single adjustment can preserve thousands of dollars in net proceeds on a mid-sized position.

Practical monitoring involves setting calendar alerts at the 11-month mark for every new purchase and reviewing earnings transcripts and valuation multiples before deciding on extension or exit.

IRS official guidance outlines exact holding-period calculations and applicable rates.

Selecting Tax-Advantaged Vehicles Like Roth Accounts

Roth IRAs and Roth 401(k)s offer tax-free growth and qualified withdrawals, making them ideal locations for high-turnover active value trades. Because contributions have already been taxed, investors can execute frequent rotations among undervalued securities without creating taxable events inside the account.

Implementation steps include prioritizing the most active portions of a value strategy inside Roth space, reserving taxable accounts for lower-turnover core holdings, and performing annual contribution room analysis to maximize available tax-free capacity. Investors should also consider backdoor Roth contributions if income limits apply and maintain separate cost-basis tracking for any non-deductible contributions.

Real-World Portfolio Adjustments and Comparisons

An investor with a $750,000 taxable account and $250,000 in Roth IRA space might reallocate by moving 60 percent of active value positions into the Roth account over two years. In the taxable account, quarterly harvesting reduces realized gains by 35 percent compared with the prior year. Performance tracking after 18 months shows the tax-efficient portfolio delivering 1.8 percentage points higher after-tax annualized return versus a control portfolio using identical pre-tax selections but without tax optimization. Sources such as SEC investor resources emphasize the cumulative impact of such small edges over multi-year periods.

Common Mistakes to Avoid

- Ignoring wash-sale rules, which can permanently disallow losses and trigger audits when identical securities are repurchased too quickly.

- Over-trading in taxable accounts, leading to excessive short-term gain realizations that outweigh any alpha generated.

- Failing to track specific share lots across multiple accounts, resulting in suboptimal tax-lot selection at sale time.

- Neglecting state and local tax implications that can add several percentage points to the effective rate on short-term gains.

- Concentrating too many high-risk value bets inside retirement accounts without considering overall asset allocation and contribution limits.

Conclusion

Tax-efficient active value investing in 2026 requires disciplined processes rather than complex products. By combining targeted loss harvesting, deliberate holding-period management, and strategic use of tax-advantaged accounts, intermediate investors can meaningfully improve net returns while maintaining the core discipline of buying undervalued securities.

FAQ on IRS Rules and Compliance

What are the 2026 wash-sale rules for value investors?

The IRS continues to disallow losses when substantially identical securities are acquired within the 30-day window surrounding the sale. Using sector ETFs or correlated but distinct stocks satisfies the requirement.

Can I use Roth accounts for frequent active trades?

Yes. Roth IRAs permit unlimited trading activity with all growth and qualified distributions remaining tax-free, making them suitable for value rotation strategies.

How do holding periods affect active value investing?

Assets held longer than one year qualify for long-term capital gains rates. Investors should monitor Treasury Department updates for any legislative changes.

What documentation is required for tax-loss harvesting?

Detailed records of purchase dates, sale prices, reinvestment details, and rationale must be retained for at least seven years to support potential audits.

Are there limits on contributions to Roth accounts in 2026?

Contribution limits adjust annually for inflation. Investors should verify current limits directly with the IRS or their plan administrator before making contributions.

No comments yet. Be the first!