Bullish Portfolio

Bullish Portfolio

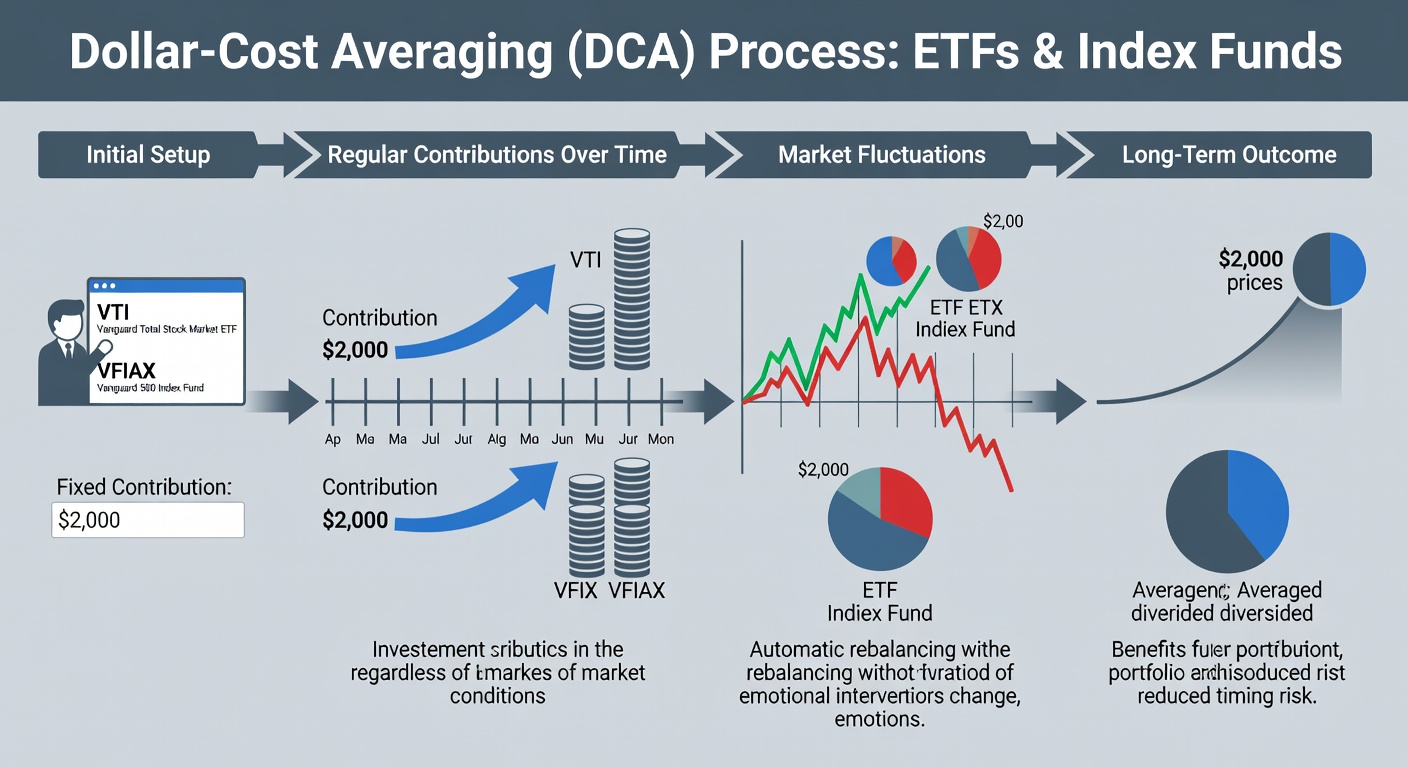

Dollar-Cost Averaging with ETFs & Index Funds: 2026 Strategy

Market volatility in 2026 makes disciplined investing essential. Dollar-cost averaging (DCA) remains one of the most reliable methods for reducing the impact of timing risk when investing in ETFs and index funds. This approach involves investing fixed amounts at regular intervals regardless of price fluctuations, allowing investors to buy more shares when prices are low and fewer when prices are high. In an environment marked by shifting interest rates, geopolitical tensions, and rapid technological advancements, DCA provides a structured way to participate in market growth without attempting to predict short-term movements.

Understanding Dollar-Cost Averaging in Volatile Markets

DCA works by spreading purchases over time, which smooths out the average cost per share. In 2026, with ongoing economic shifts and sector rotations, combining broad-market index funds with targeted sector ETFs creates a balanced strategy that captures growth while limiting downside exposure. Investors benefit from automatic purchases that remove emotional decision-making during downturns or rallies. This method has historically helped individuals stay invested through cycles of uncertainty, turning market swings into opportunities rather than obstacles. By committing to regular investments, participants accumulate shares at varying price points, which can lead to favorable long-term outcomes even when initial entry points appear unfavorable.

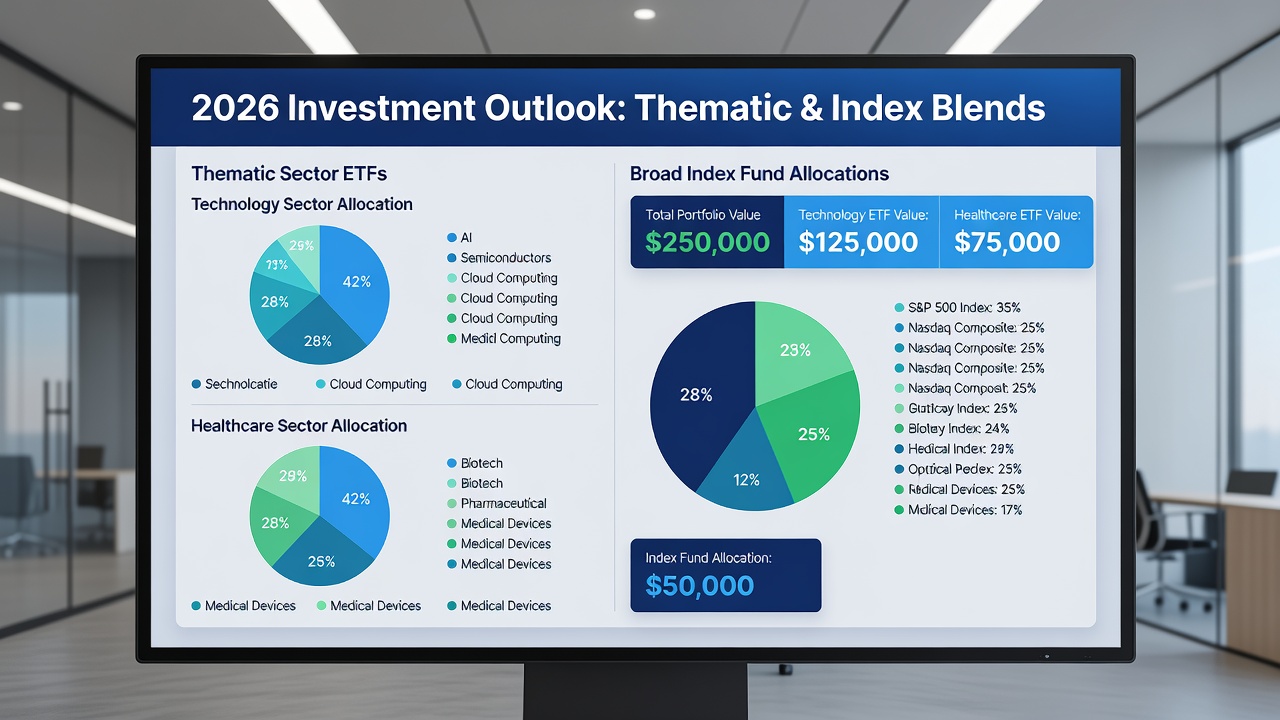

Benefits of Blending Sector ETFs with Broad Index Funds

A core advantage of this 2026 strategy lies in diversification through blending. Broad index funds deliver exposure to the entire market, providing stability and low correlation to single-industry events. Sector ETFs, meanwhile, allow investors to overweight areas like technology, renewable energy, or financial services that may outperform in specific economic conditions. The combination reduces overall portfolio volatility while maintaining upside potential. For instance, during periods of rapid innovation, technology sector ETFs can boost returns, whereas broad funds anchor the portfolio during sector-specific corrections. This blend also supports better risk-adjusted performance over multi-year horizons.

Selecting Low-Cost Vehicles for 2026

Focus on ETFs and index funds with expense ratios below 0.10% where possible. Broad-market options such as total stock market or S&P 500 index funds provide core exposure, while sector ETFs in technology, healthcare, or clean energy allow tactical tilts. Prioritize funds with high liquidity and tight bid-ask spreads to minimize transaction costs over repeated purchases. Key criteria include tracking error, dividend yield consistency, and tax efficiency. Review prospectuses and compare holdings overlap to avoid unintended concentration. Investors should also consider fund size and trading volume to ensure easy entry and exit at consistent prices throughout the DCA schedule.

Setting Contribution Schedules

Establish automated transfers from checking accounts on paydays or the first of each month. Weekly or bi-weekly schedules often work better than monthly ones during high-volatility periods because they increase the number of purchase points. Determine a sustainable dollar amount based on cash flow rather than attempting to maximize every contribution. Align contributions with income cycles for consistency. Adjust amounts annually during portfolio reviews rather than reacting to short-term market moves. Use employer direct deposit features when available for seamless execution. Additionally, consider linking contributions to performance milestones, such as increasing amounts after receiving bonuses, to accelerate portfolio growth without disrupting the core DCA rhythm.

Tracking Allocation Drift

Over time, strong performance in certain sectors can push allocations away from target weights. Quarterly reviews help identify drift exceeding 5 percentage points. Rebalance by directing new contributions toward underweight areas instead of selling assets, preserving the tax advantages of DCA. Tools such as portfolio trackers from major brokerages simplify monitoring. Document target allocations at the start of each year and compare against current weights. This ongoing vigilance prevents any single sector from dominating the portfolio, maintaining the intended risk profile throughout market cycles.

Step-by-Step Implementation Example

Consider an investor starting with $2,000 monthly contributions split 70% broad index fund and 30% sector ETFs. Month one: purchase shares at prevailing prices. Month two: the market dips, resulting in more shares acquired with the same dollar amount. Continue this process for 12 months, then evaluate cumulative share count and average cost basis versus a lump-sum approach. Repeat the process with slight adjustments if new capital becomes available or risk tolerance changes. Maintain records of each purchase date, price, and number of shares. Extend the example over three years to observe compounding effects and how drift adjustments influence final allocation.

Side-by-Side Performance Scenarios

During a hypothetical 15% market decline over six months, DCA investors accumulate shares at progressively lower prices, resulting in a lower average cost than those who invested a lump sum at the start. In a steady upward market, the same strategy still participates in gains while avoiding the regret of missing the bottom. These scenarios highlight how DCA reduces the psychological burden of perfect timing. Further analysis shows that in sideways markets, the strategy often outperforms buy-and-hold by acquiring more units at depressed levels, leading to accelerated recovery once trends resume.

Tax Efficiency and Platform Considerations

DCA pairs well with tax-advantaged accounts such as IRAs or 401(k)s to defer or eliminate capital gains taxes on rebalancing activities. When using taxable brokerage accounts, focus on tax-efficient ETFs that minimize distributions. Choose platforms offering commission-free trading and automatic investment features to reduce friction. Compare brokerage tools for drift alerts and contribution scheduling to streamline execution across multiple accounts.

Handling Market Extremes in 2026

Extreme events, such as sudden policy changes or global supply disruptions, test any DCA plan. Maintain discipline by continuing scheduled purchases rather than pausing or accelerating. Set predefined rules for temporary increases only when personal finances allow, not in reaction to headlines. This measured response preserves the strategy's core benefit of removing emotion from decision-making.

Common Execution Mistakes and How to Avoid Them

Many investors pause contributions during downturns, defeating the purpose of DCA. Others select overly narrow ETFs that increase volatility rather than dampen it. Failing to automate leads to inconsistent execution. Review contributions every six months to ensure automation remains active and aligned with goals. Another frequent error involves ignoring fees on small recurring trades; selecting no-commission platforms mitigates this issue effectively.

FAQ

How often should I review my DCA plan?

Conduct a full review annually or after major life events. Minor tweaks to contribution amounts can occur quarterly without disrupting the core strategy.

Is DCA better than lump-sum investing?

Historical data shows lump-sum investing often outperforms on average, yet DCA significantly reduces regret and behavioral mistakes, making it preferable for most long-term investors navigating uncertain markets.

What happens if I miss a scheduled contribution?

Missing one or two contributions has minimal long-term impact. Simply resume the schedule at the next opportunity without attempting to make up the missed amount in a single large purchase.

For additional foundational reading on investment principles, consult Investopedia and regulatory guidance available at SEC.gov.

Conclusion

Dollar-cost averaging with a blend of ETFs and index funds offers a repeatable framework for 2026 and beyond. By focusing on low costs, consistent schedules, and regular drift monitoring, investors build resilient portfolios that weather market swings without requiring perfect foresight. Start small, automate everything, and let time and discipline compound the results.

No comments yet. Be the first!