Bullish Portfolio

Bullish Portfolio

Introduction to Space Tech as a Growth Sector in 2026

The space industry continues to attract significant attention from investors seeking opportunities beyond traditional technology or energy sectors. With expanding private investment and government contracts fueling innovation, space tech stocks offer compelling potential for growth-oriented portfolios. This guide examines satellite operators, rocket manufacturers, and component suppliers as key areas of interest for 2026 positioning. Market drivers include rising demand for satellite broadband, national security initiatives, and commercial space tourism. Public companies benefit from contracts that provide revenue visibility while private capital accelerates technological breakthroughs. Investors new to this sector can benefit from understanding how these elements combine to create bullish scenarios for carefully selected stocks.

Key Market Drivers Shaping 2026 Opportunities

Government spending on space programs remains a primary catalyst. Agencies continue to award multi-year contracts for launch services and satellite deployment. Private sector participation has increased dramatically, lowering costs and expanding addressable markets in communications and Earth observation. Technological advancements in reusable launch vehicles and miniaturization of satellites further support scalability. Investors should monitor regulatory developments that influence market access and competition. Additional drivers include growing commercial demand for low-Earth orbit services, international collaborations on lunar exploration programs, and the proliferation of small satellite constellations for data analytics and global connectivity. These factors collectively point to sustained revenue growth potential across the value chain.

For deeper context on government initiatives, review resources from NASA.

Evaluating Financials and Growth Metrics for Space Stocks

Begin by reviewing revenue growth from contract backlogs and commercial sales. Examine gross margins, which can improve as manufacturing scales. Cash flow analysis is critical because many firms reinvest heavily in research and development. Key ratios include price-to-sales for high-growth names and debt-to-equity to assess balance sheet strength. Compare year-over-year increases in backlog and new order announcements to gauge momentum. Additional metrics worth tracking encompass operating expenses relative to revenue, free cash flow trends, and customer concentration risks. Qualitative factors such as intellectual property portfolios and partnerships with established aerospace primes also provide insight into long-term viability. By combining quantitative screens with qualitative review, investors can identify companies demonstrating both current traction and scalable business models.

Practical Steps for Screening Space Tech Candidates

- Define investment criteria such as minimum market capitalization and revenue growth thresholds to focus research efforts efficiently.

- Use financial databases to filter companies with exposure to aerospace or satellite segments, paying close attention to primary business descriptions in filings.

- Analyze SEC filings for contract details and risk disclosures, cross-referencing with earnings transcripts for management commentary on execution timelines.

- Review analyst reports and earnings call transcripts for forward guidance, noting any updates on launch schedules or regulatory milestones.

- Assess competitive positioning relative to peers in launch services versus hardware supply, including barriers to entry and differentiation factors.

- Monitor industry news for merger activity or new entrants that could reshape market dynamics over the coming quarters.

These steps help narrow the universe to firms with sustainable business models and reduce the likelihood of overlooking material risks.

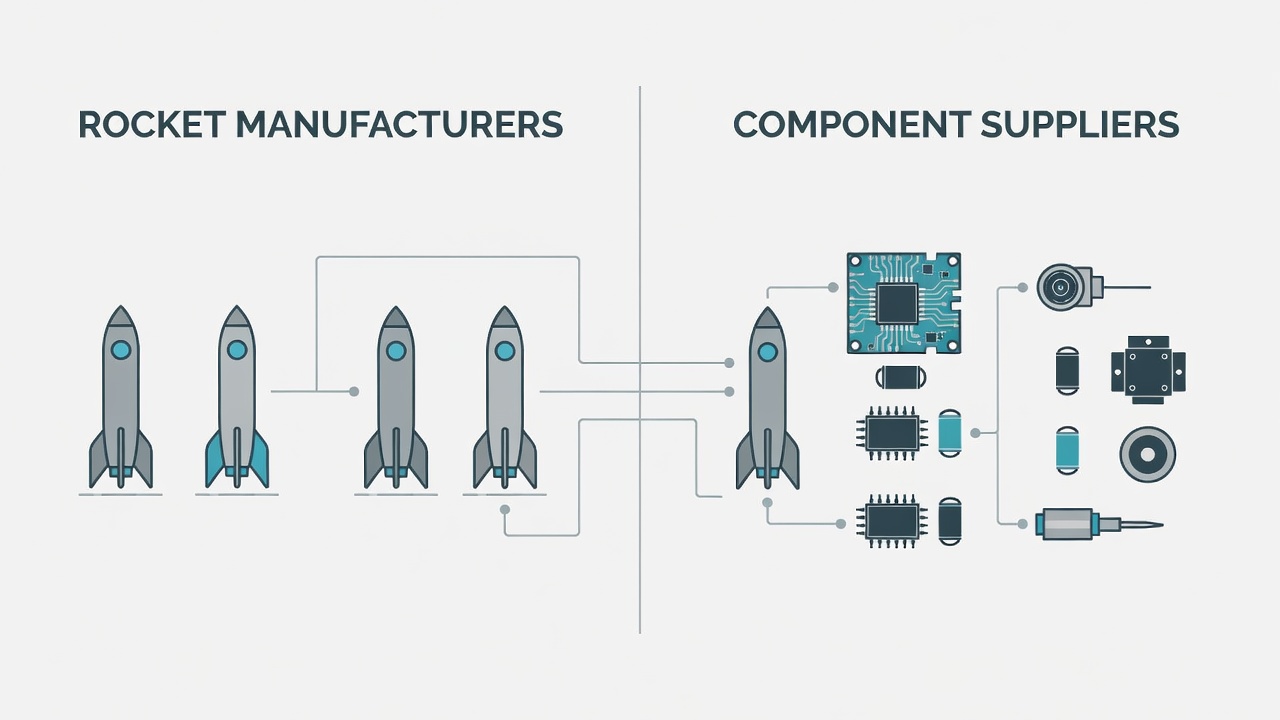

Comparing Rocket Manufacturers and Component Suppliers

Rocket manufacturers often face higher capital intensity and execution risk but can achieve substantial valuation multiples on successful launches. Component suppliers typically offer more stable revenue streams through long-term supply agreements and lower barriers to scaling production. For example, a launch provider may derive income from both government and commercial missions, while a sensor or propulsion parts maker benefits from broader adoption across multiple vehicle programs. Diversification across both categories can balance risk and reward in a portfolio. Rocket manufacturers must navigate complex testing regimes and insurance requirements, whereas suppliers can leverage existing manufacturing expertise from adjacent industries. Investors evaluating these segments should consider supply chain dependencies, technological obsolescence risks, and the pace of standardization in satellite hardware.

Real-World Examples of Portfolio Allocation

An investor with moderate risk tolerance might allocate 5-8% of a growth sleeve to space holdings. Within that allocation, 60% could target established satellite operators and 40% emerging launch or component firms. Rebalancing annually helps maintain exposure as valuations shift with contract wins or delays. Another approach involves pairing space tech with broader aerospace ETFs for liquidity while maintaining direct equity exposure to high-conviction names. Consider a hypothetical scenario where an investor starts with positions in two satellite service providers and one propulsion component company, then adds a small allocation to a launch services firm after its next successful mission. This staged entry allows for learning while capturing upside from multiple parts of the ecosystem. Regular review of position sizing relative to overall portfolio volatility remains essential.

Understanding Risks Including Regulatory Hurdles and Volatility

Space ventures encounter technical failures, launch delays, and shifting government priorities. Regulatory approvals from agencies such as the FAA can influence timelines. Market volatility often exceeds broader indices due to binary outcomes around major missions. Geopolitical tensions may also affect export controls and international partnerships. Investors should size positions appropriately and maintain a long-term horizon to weather short-term swings. Additional risks include supply chain disruptions for specialized materials, cybersecurity threats to satellite networks, and potential changes in spectrum allocation policies that impact service providers. Mitigation strategies encompass thorough due diligence on management teams, diversification across sub-sectors, and use of stop-loss orders or options for downside protection where appropriate.

Reference official regulatory updates via the SEC for timely disclosures.

Short FAQ on Entry Points for New Investors

When is a good time to enter space tech stocks?

Consider dollar-cost averaging during periods of sector consolidation or after major contract announcements to manage timing risk.

How much should beginners allocate initially?

Start with a small percentage of overall equity exposure and increase only after gaining familiarity with individual company fundamentals.

Are there tax-advantaged ways to gain exposure?

Some investors explore brokerage accounts with commission-free trading or retirement vehicles that permit individual stock selection, depending on their overall plan.

What common mistakes should new investors avoid?

Avoid concentrating too heavily in a single launch provider and always verify contract details rather than relying solely on headlines.

Conclusion

Space tech represents an evolving growth frontier supported by structural demand and innovation. By focusing on financial discipline, diversified exposure, and risk awareness, investors can position portfolios thoughtfully for 2026 and beyond. Continued monitoring of contracts and technological milestones will remain essential for success.

No comments yet. Be the first!