Bullish Portfolio

Bullish Portfolio

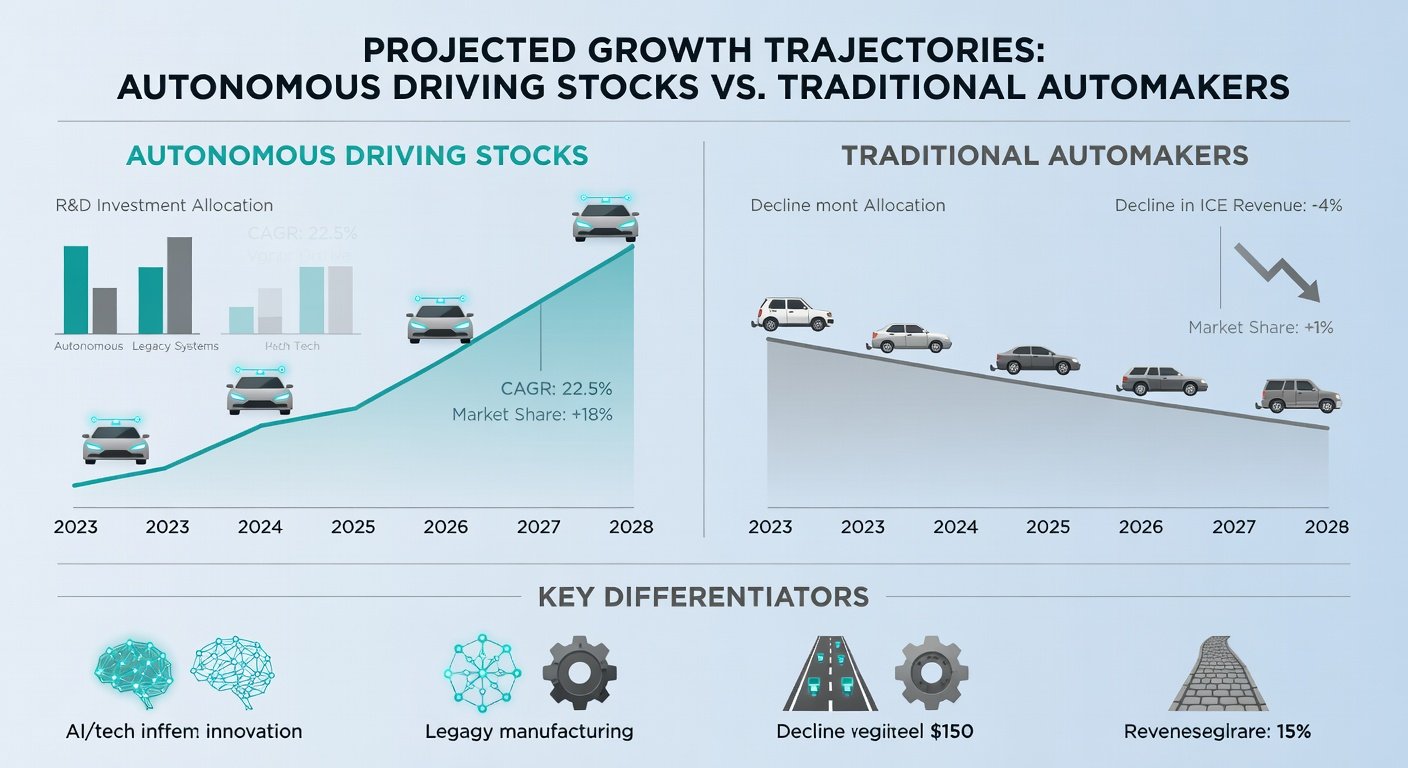

Introduction: Why Autonomous Driving Stocks Are Poised for Growth in 2026

The autonomous driving sector is accelerating toward a major inflection point. Technological breakthroughs in AI, sensor fusion, and regulatory support are creating tailwinds for companies leading the charge. Investors seeking high-potential opportunities should examine stocks like Tesla, Alphabet’s Waymo, and GM’s Cruise division. These firms combine revenue growth potential with competitive moats in a market projected to expand rapidly through the decade. As consumer demand for safer and more efficient transportation rises, early leaders in autonomy stand to benefit from network effects where more data leads to better algorithms and faster market dominance.

Market expansion is driven by falling hardware costs, improved machine learning models, and increasing consumer acceptance of robotaxis and advanced driver-assistance systems. As fleets scale, companies with strong data advantages are expected to capture outsized returns compared to traditional automakers still reliant on internal combustion engines. This shift represents not just incremental improvement but a fundamental reimagining of mobility, with implications for urban planning, insurance, and logistics industries worldwide.

Technological Advancements Fueling the Sector

Recent progress in lidar, radar, and camera-based perception systems has dramatically improved vehicle reliability in diverse weather and traffic conditions. Companies are now integrating foundation models similar to those used in large language processing to interpret complex driving scenarios in real time. For example, Tesla’s end-to-end neural network approach allows vehicles to learn directly from millions of miles of driving data collected daily, reducing the need for hand-coded rules. Waymo has refined its simulation environments to test millions of edge cases virtually before deploying updates on public roads. These advancements lower operational costs and accelerate the path to unsupervised autonomy, which is critical for achieving profitability in ride-hailing applications.

Regulatory Tailwinds and Government Support

Regulatory frameworks are evolving to support commercial deployment while maintaining safety standards. The National Highway Traffic Safety Administration has issued updated guidelines that clarify testing and deployment requirements for automated vehicles. Similarly, the U.S. Department of Transportation continues to promote consistent state-level policies that reduce fragmentation. These tailwinds reduce legal uncertainty and encourage long-term capital investment from both public markets and strategic partners. In several states, pilot programs have already transitioned into permanent commercial operations, demonstrating that regulators are increasingly comfortable with proven safety records.

Leading Company Profiles and Competitive Edges

Tesla: Full Self-Driving Leadership

Tesla remains the most prominent player thanks to its vertically integrated approach and vast real-world driving data. Its Full Self-Driving software continues to iterate through over-the-air updates, giving it an edge in both consumer vehicles and potential robotaxi networks. Tesla’s competitive advantage lies in its ability to collect and process data at massive scale while controlling the entire hardware and software stack. This integration allows rapid iteration that competitors relying on third-party suppliers cannot easily match. Real-world examples include Tesla’s unsupervised FSD demonstrations in select cities, which highlight the company’s progress toward hands-free, eyes-off operation.

Alphabet (Waymo): Robotaxi Pioneer

Waymo, Alphabet’s autonomous subsidiary, operates commercial robotaxi services in multiple U.S. cities. Its focus on safety validation and partnerships with automakers provides a diversified path to commercialization. Waymo’s early regulatory approvals position it well for scaled operations by 2026. The company has logged millions of autonomous miles and maintains detailed safety reports that build public and regulatory confidence. Strategic alliances with vehicle manufacturers enable Waymo to focus on software while leveraging established production capabilities for its custom sensor suite.

General Motors (Cruise): Scaling with Institutional Backing

GM’s Cruise unit benefits from substantial capital investment and integration with GM’s vehicle platforms. Recent software and hardware upgrades aim to improve reliability in complex urban environments. Cruise’s strategy emphasizes both personal vehicles and dedicated robotaxi fleets, creating multiple revenue channels. By combining GM’s manufacturing expertise with advanced mapping and perception technology, Cruise can deploy vehicles at lower marginal cost than pure-play startups. Examples of operational success include expanded service areas in major metros where rider feedback has informed iterative improvements.

Revenue Growth Forecasts and Valuation Metrics

While specific price targets fluctuate, qualitative trends show accelerating adoption. Tesla’s autonomy-related revenue is expected to grow significantly as regulatory clarity improves. Waymo continues to expand paid ride volumes, while Cruise targets broader geographic coverage. Investors should monitor P/E ratios relative to growth rates, comparing these metrics against legacy automakers with slower EV and autonomy transitions. Companies that successfully transition from development to commercial revenue streams typically see multiple expansion as profitability becomes visible. Practical analysis involves tracking metrics such as cost per mile, utilization rates, and geographic expansion speed to gauge execution quality.

Comparison: Projected Returns vs Traditional Auto Stocks

| Metric | AV-Focused Stocks | Traditional Auto Stocks |

|---|---|---|

| Growth Drivers | Software, data, robotaxis | Vehicle sales, legacy models |

| Risk Profile | High volatility, tech execution | Lower but cyclical |

| 2026 Outlook | Explosive potential | Steady but limited upside |

| Competitive Moat | Data networks and AI | Brand and manufacturing scale |

AV leaders generally offer higher upside potential but require tolerance for regulatory and safety-related swings. Traditional automakers may provide dividend stability yet face margin pressure from the ongoing shift to electrification and software-defined vehicles.

Potential Risks and How to Mitigate Them

Safety incidents remain a primary concern that could trigger temporary regulatory halts or negative publicity. High capital requirements for scaling fleets can strain balance sheets during periods of rapid expansion. Competition from both tech giants and nimble startups adds execution risk. Public trust and adoption timelines may also vary by region, affecting revenue forecasts. Investors can mitigate these risks by maintaining diversified holdings, staying informed through official safety reports, and avoiding over-concentration in any single name. Real-world examples of past incidents have shown that transparent communication and swift corrective action help companies recover market confidence over time.

Step-by-Step Guide to Adding AV Stocks to Your Portfolio

- Assess your risk tolerance and time horizon for tech-driven volatility, considering how much allocation fits within your overall investment policy statement.

- Research current financials and autonomy roadmaps for each company by reviewing quarterly earnings transcripts and technology updates.

- Consider dollar-cost averaging to manage entry points and reduce the impact of short-term market swings.

- Diversify across multiple AV names rather than concentrating in one, balancing exposure between hardware, software, and fleet operators.

- Monitor regulatory news and quarterly autonomy updates from sources such as the SAE International to stay ahead of policy changes.

- Rebalance periodically as market conditions evolve and new competitors enter the space.

- Consult tax implications and consider holding periods that align with long-term capital gains treatment where applicable.

Frequently Asked Questions

When will widespread AV adoption occur?

Most forecasts point to meaningful commercial robotaxi expansion between 2026 and 2030, with regulatory milestones acting as key catalysts. Adoption will likely begin in dense urban corridors before spreading to suburban and highway applications.

How should investors diversify AV exposure?

Combine direct stock holdings with thematic ETFs, maintain position sizes under 5-10% of total portfolio, and pair with broader market diversification. This approach balances growth potential against the inherent uncertainties of emerging technology.

What role does data play in competitive advantage?

Companies that accumulate the largest and most diverse driving datasets can train superior AI models, creating a self-reinforcing moat that becomes harder for newcomers to overcome as scale increases.

Autonomous driving represents one of the most transformative investment themes of the coming years. By focusing on companies with clear technological leadership, monitoring both opportunities and risks, and following a disciplined portfolio construction process, investors can position themselves for the anticipated 2026 bull run while managing downside exposure effectively.

No comments yet. Be the first!