Bullish Portfolio

Bullish Portfolio

Introduction to Advanced Risk Management in Bullish Markets

As 2026 unfolds with continued market volatility driven by evolving economic policies and global events, experienced investors focused on bullish stock picks must prioritize advanced risk management to protect gains. This comprehensive guide explores sophisticated techniques including portfolio hedging strategies, precise position sizing formulas, and optimized stop-loss placement using real market data and scenarios. Investors seeking to safeguard top stocks in 2026 will find practical examples, decision frameworks, and adaptation methods for sudden sector shifts. The goal is to balance aggressive growth pursuit with disciplined downside protection.

Understanding 2026 Market Volatility for Bullish Picks

Bullish stock selection in 2026 demands deep awareness of macroeconomic influences such as fluctuating interest rates, supply chain disruptions, and geopolitical developments. Investors should examine historical volatility patterns from the prior year to forecast potential swings and identify resilient opportunities. High-conviction stocks often emerge in technology, renewable energy, and healthcare sectors where strong fundamentals persist despite broader uncertainty. Understanding correlation changes between assets helps anticipate how one sector's movement might influence others, enabling proactive adjustments before volatility spikes impact portfolio value.

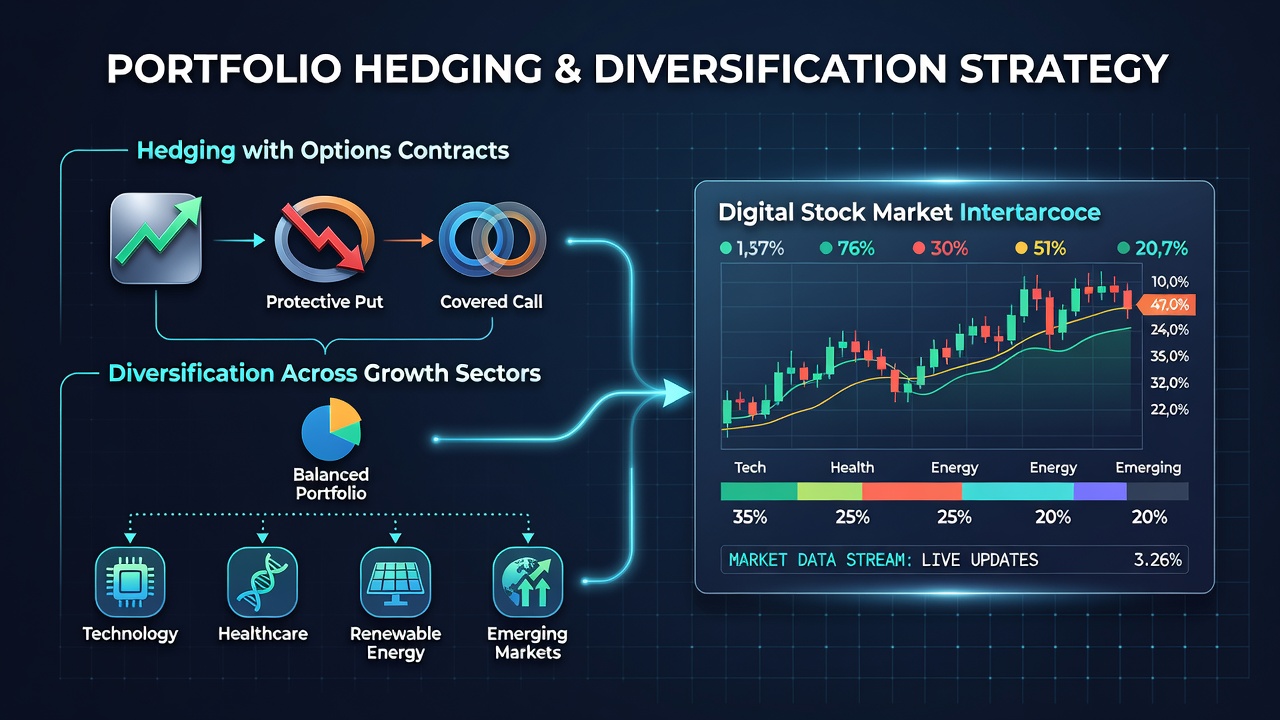

Portfolio Hedging Strategies for Protection

Hedging forms a foundational defense mechanism for maintaining bullish positions without forced liquidation. Advanced approaches include layering index options to counter broad market declines while preserving core holdings. For instance, acquiring protective puts on major indices can cap losses during unexpected corrections, allowing continued participation in upward trends. Investopedia offers detailed resources on derivatives mechanics for investors refining these tactics.

Diversification across uncorrelated growth sectors provides another layer of resilience. Allocating capital among AI-focused technology, innovative healthcare, and sustainable energy companies mitigates single-sector concentration risks. When comparing options-based protection to diversification, options deliver precise, time-bound insurance but incur ongoing costs and require monitoring. Diversification supports steady upside capture yet may reduce peak returns during sector-specific rallies. A blended approach often proves optimal, using modest option overlays alongside sector spreading for balanced 2026 portfolios.

Additional hedging instruments such as collars and inverse ETFs can further customize protection levels. Collars involve selling calls to offset put purchase costs, creating a defined risk range. Inverse ETFs serve as tactical short-term hedges during anticipated downturns. Regular portfolio stress testing against historical volatility episodes helps validate hedge effectiveness before market stress materializes.

Position Sizing Formulas with Practical Examples

Accurate position sizing prevents any single holding from jeopardizing overall portfolio stability. The Kelly Criterion, adapted for equities, calculates optimal allocation as Position Size = (Win Probability × Reward Ratio - Loss Probability) / Reward Ratio. In a bullish scenario with a 60 percent estimated success rate and 2-to-1 reward-to-risk profile, the formula suggests allocating approximately 20 percent of available capital. Investors should cross-reference this with current volatility readings and personal risk tolerance before finalizing sizes.

Step-by-Step Risk-Reward Ratio Calculation

- Establish the entry price and projected target exit based on fundamental analysis and technical targets for the chosen bullish stock.

- Define a stop-loss threshold anchored to key support levels or volatility measures to quantify maximum acceptable loss.

- Calculate the ratio by dividing potential reward distance by potential loss distance to ensure favorable asymmetry.

- Scale position size downward so that any triggered stop results in no more than 1 to 2 percent portfolio drawdown.

- Re-evaluate the ratio after major news events or earnings releases that could alter price dynamics.

Additional formulas incorporate volatility adjustments, such as scaling positions inversely to the stock's beta relative to the broader market. This ensures higher-volatility names receive smaller allocations while stable growth stocks can command larger weights without elevating overall risk.

Stop-Loss Optimization Techniques

Traditional fixed stop-loss orders frequently trigger prematurely amid normal market noise. Advanced methods employ trailing stops calibrated to average true range indicators, allowing positions breathing room during healthy advances. Setting the stop at 1.5 times the current ATR below price accommodates typical fluctuations while locking in gains as momentum builds. Periodic recalibration based on evolving volatility ensures stops remain relevant throughout the holding period.

Time-based stops can complement price-based rules by exiting positions after predetermined holding periods if targets remain unmet. Combining multiple stop types creates layered protection that adapts to both gradual trends and abrupt reversals common in 2026 markets.

Comparing Options Protection Versus Sector Diversification

Options strategies provide concentrated, adjustable coverage ideal for short-term volatility events but demand active oversight and can erode returns through premium decay. Sector diversification delivers passive, low-maintenance resilience across economic cycles yet may underperform when one favored sector dominates. Hybrid implementations that pair selective options coverage with diversified sector buckets frequently deliver superior risk-adjusted outcomes for bullish investors navigating 2026 conditions.

Practical Checklists for Implementation

- Assess overall portfolio beta against major benchmarks on a weekly schedule to detect unintended leverage buildup.

- Rebalance any position exceeding 15 percent of total capital to restore diversification discipline.

- Conduct quarterly stress tests incorporating volatility data from 2022 through 2025 downturn scenarios.

- Document entry criteria, risk parameters, and exit rules for every new bullish position before capital deployment.

- Review correlation matrices monthly to identify emerging concentrations across seemingly unrelated holdings.

Common Pitfalls to Avoid

Frequent mistakes include increasing exposure during strong rallies without corresponding risk controls, overlooking shifting correlations between sectors, and depending on informal mental stops instead of executable orders. Emotional interference with preset stop levels often leads to larger losses, while neglecting liquidity analysis in smaller-capitalization bullish names can trap capital during rapid exits. Maintaining a trading journal helps identify recurring behavioral patterns that undermine disciplined execution.

FAQ: Adapting Risk Methods to Sector Shifts

How do I adjust hedges during sudden sector rotations?

Track leading economic indicators and policy announcements to identify rotation signals early. Shift protective option coverage toward newly favored sectors while preserving core diversification across multiple growth areas for continued resilience.

What stop-loss strategy works best for high-volatility growth stocks?

ATR-based trailing stops offer necessary flexibility, permitting normal price oscillations around strong momentum trends while automatically tightening protection as gains accumulate and volatility moderates.

Can these techniques apply to ETF-based bullish exposure?

Absolutely. Scale position sizing formulas proportionally to ETF holdings and overlay broad index options for efficient, low-cost portfolio-level protection during uncertain periods.

How frequently should risk parameters be reviewed?

Conduct formal reviews at least monthly or immediately following significant market-moving events such as Federal Reserve announcements or major earnings seasons to keep strategies aligned with current conditions.

Conclusion

Mastering advanced risk management elevates bullish stock strategies throughout 2026's dynamic environment. Integrating hedging instruments, disciplined position sizing, adaptive stop techniques, and proactive sector monitoring allows investors to pursue meaningful growth while systematically limiting downside exposure. Continuous refinement grounded in live market feedback builds durable portfolio resilience capable of withstanding volatility while capturing upside opportunities.

No comments yet. Be the first!