Bullish Portfolio

Bullish Portfolio

Introduction to Advanced Asset Allocation

Advanced asset allocation represents a sophisticated evolution beyond basic diversification, emphasizing dynamic methods that maximize the exponential power of compounding returns. For intermediate investors aiming to reach financial independence sooner, these strategies integrate risk-adjusted growth tactics with precise portfolio management. By moving past static models, investors can capture market opportunities while mitigating downside exposure, ultimately accelerating long-term wealth accumulation through disciplined rebalancing and multi-asset exposure.

The core idea centers on understanding how small, consistent optimizations in allocation can lead to dramatically different outcomes over decades. Compounding works most effectively when volatility is controlled and capital is redeployed efficiently across asset classes that exhibit varying correlations during different economic cycles.

Core Principles of Dynamic Rebalancing

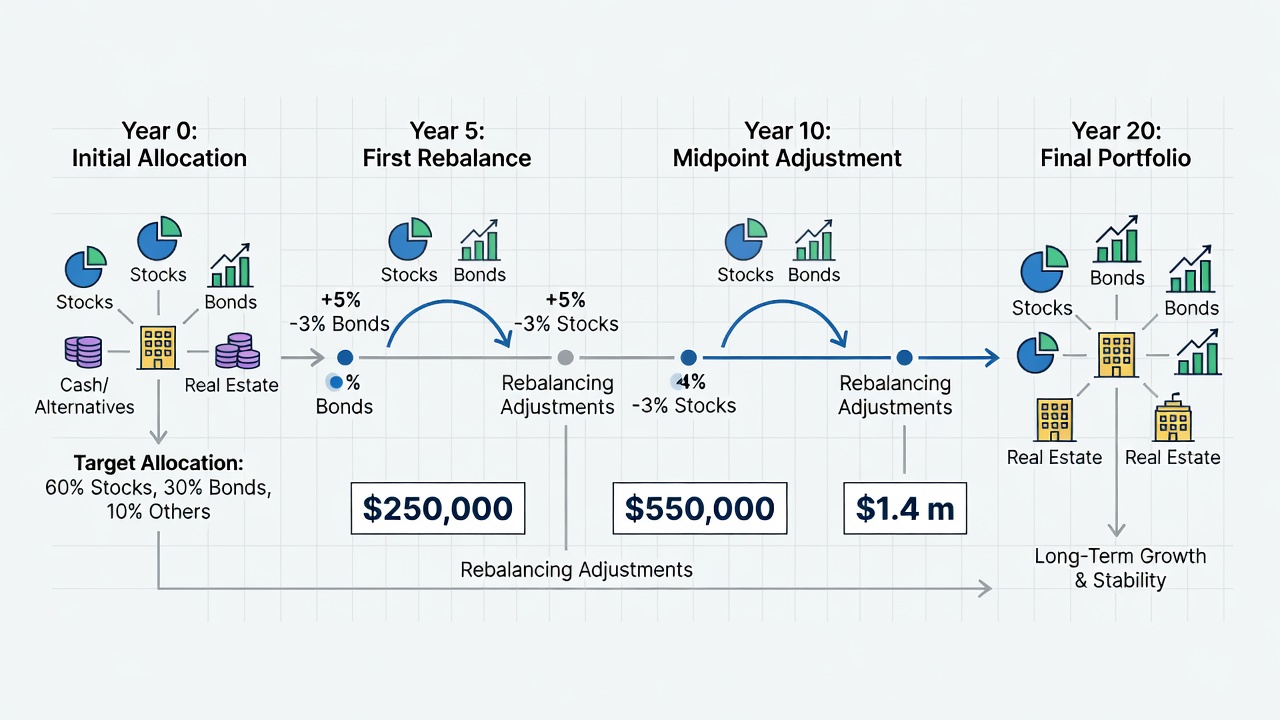

Dynamic rebalancing differs from calendar-based methods by responding to real-time market conditions and portfolio drift. When one asset class outperforms significantly, its weight increases, prompting partial sales to restore target allocations and lock in gains. This process reduces volatility drag and frees capital for underweighted areas poised for recovery. Investors benefit from predefined tolerance bands, such as 5% deviations, that trigger adjustments only when meaningful shifts occur, preserving compounding momentum without excessive transaction costs.

Implementing this requires clear rules based on volatility metrics and correlation analysis. For instance, during equity rallies, reducing stock exposure slightly while increasing alternatives maintains balance. The result is smoother growth curves that compound more reliably than buy-and-hold approaches.

Step-by-Step Multi-Asset Portfolio Construction

Constructing an advanced portfolio begins with a thorough assessment of personal risk tolerance, investment horizon, and liquidity needs. Start by categorizing assets into equities for growth, fixed income for stability, real assets for inflation protection, and international securities for diversification. Assign initial weights using forward-looking expected returns derived from historical data adjusted for current valuations.

Next, incorporate tactical overlays that allow modest deviations from strategic targets based on economic indicators like yield curves or earnings growth. Build in automatic rebalancing triggers using spreadsheet formulas that monitor daily or weekly price changes. Test the allocation against multiple scenarios, including inflation spikes and recessionary periods, to ensure resilience. Finally, document the entire framework in a written investment policy statement to maintain discipline over time.

Real-World Numerical Projections

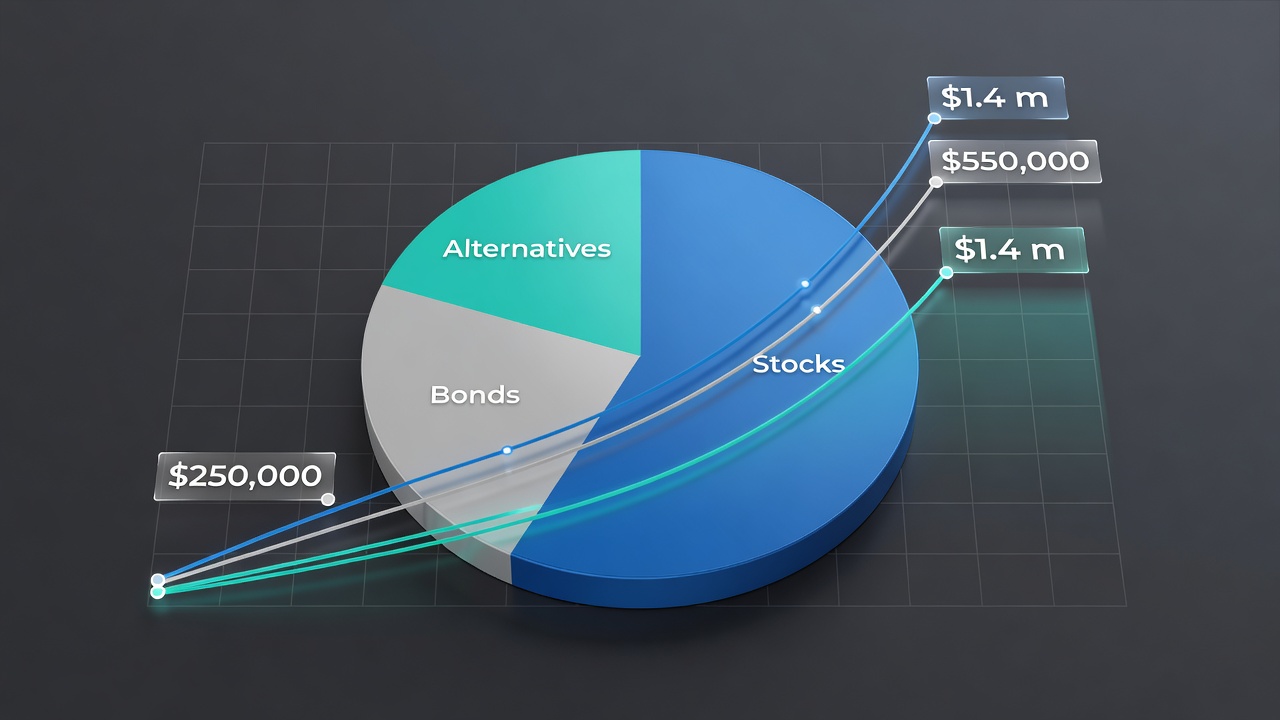

Consider a hypothetical starting portfolio of $250,000 allocated across U.S. equities, international stocks, bonds, and alternatives. Using a dynamic rebalancing approach that adjusts quarterly within 5% bands, the portfolio might achieve an annualized return of approximately 8.2% with reduced standard deviation compared to a static 60/40 mix. Over 10 years, this could translate into an ending value exceeding $550,000 due to minimized drawdowns allowing more capital to remain invested during recoveries.

Extending the projection to 20 years highlights the exponential effect: the same strategy might grow the portfolio beyond $1.4 million, assuming average market conditions. These outcomes stem from capturing gains systematically and redeploying them into assets temporarily out of favor, amplifying the compounding rate beyond what static allocation delivers.

Static Versus Tactical Allocation Approaches

Static allocation maintains fixed percentages through simple periodic resets, offering ease of implementation and lower cognitive load. However, it often underperforms in shifting regimes because it ignores valuation signals and economic cycles. Tactical allocation introduces flexibility by permitting targeted shifts, such as increasing defensive holdings when equity multiples expand rapidly. While this can enhance returns, it demands rigorous rules to prevent behavioral errors like chasing recent performance.

Comparative analysis shows tactical methods outperforming static ones in backtests spanning multiple decades, particularly when volatility is high. The key differentiator lies in execution discipline rather than prediction accuracy.

Practical Tools for Tracking and Analysis

A comprehensive tracking spreadsheet serves as the operational backbone for advanced allocation. Include columns for current market values, target weights, actual weights, and deviation percentages. Add formulas that automatically flag rebalancing opportunities and calculate projected future values using compound growth functions. Incorporate correlation matrices across asset classes and Monte Carlo simulation tabs that run thousands of market scenarios to estimate probability distributions of outcomes. Update inputs monthly with fresh price data to keep projections relevant and actionable.

Common Pitfalls to Avoid

- Overreacting to short-term volatility without adhering to predefined tolerance bands, which disrupts compounding by incurring unnecessary costs and taxes.

- Ignoring tax implications during frequent rebalancing, leading to erosion of net returns in taxable accounts rather than using tax-advantaged vehicles strategically.

- Neglecting to account for evolving personal circumstances such as changing income needs or risk capacity as life events occur.

- Relying solely on historical data without incorporating forward-looking adjustments for regime changes in inflation or interest rates.

- Failing to maintain a written policy statement, allowing emotional decisions to override the systematic process.

FAQ Section

How do tax implications affect advanced allocation strategies?

Tax-efficient implementation prioritizes high-turnover tactics within retirement accounts while favoring low-turnover holdings and municipal bonds in taxable portfolios to minimize annual drag on compounding.

What happens during periods of high market volatility?

Dynamic frameworks incorporate volatility buffers and automatic rebalancing bands that prevent panic selling, allowing the portfolio to stay invested and benefit from eventual recoveries that fuel long-term compounding.

How should investors adjust allocations near retirement?

Gradual shifts toward income-generating assets become appropriate while retaining some growth exposure to combat longevity risk, with dynamic rules scaling the pace based on portfolio size and spending needs.

Conclusion

Mastering advanced asset allocation equips investors with the tools to accelerate wealth building through optimized compounding. By combining dynamic rebalancing, rigorous multi-asset construction, and disciplined tracking mechanisms, individuals can navigate market complexities with greater precision and move steadily toward financial independence. For additional regulatory guidance and educational materials, consult resources from SEC and Investor.gov.

No comments yet. Be the first!