Bullish Portfolio

Bullish Portfolio

Introduction: Why 2026 Retirement Rules Demand Extra Vigilance

Mid-career professionals are increasingly anxious about hidden mistakes in Roth IRA and 401(k) accounts that can quietly erode decades of savings. Under 2026 contribution limits and distribution rules, even small oversights compound into major shortfalls. This guide examines eight critical traps, offers step-by-step fixes, and illustrates potential lost gains with realistic examples.

Trap 1: Contribution Limit Oversights

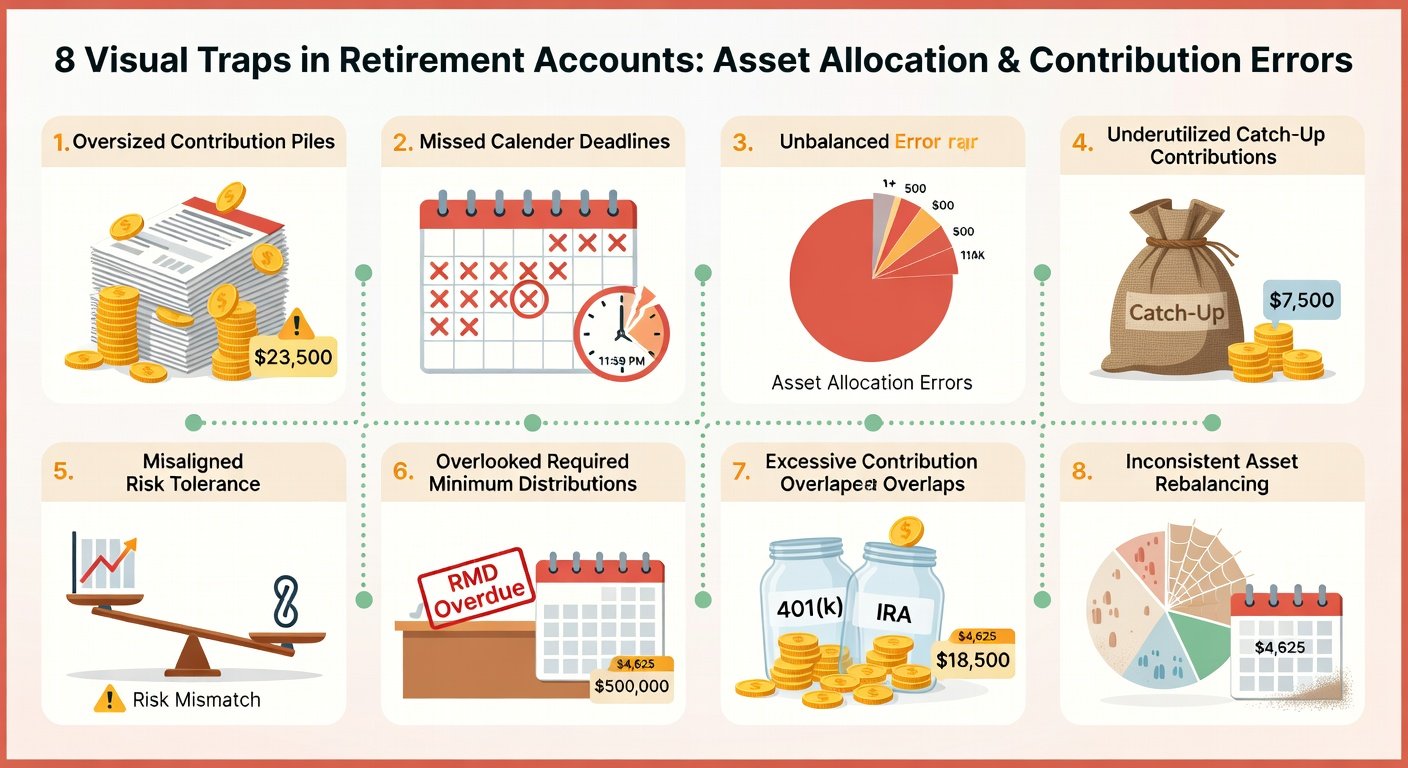

Exceeding annual limits triggers immediate taxes and penalties. For 2026, the employee deferral limit stands at $23,500 with catch-up contributions of $7,500 for those 50 and older. Failing to track employer matches or mega backdoor options often leads to excess contributions.

Actionable Fix

- Review your plan’s summary annually in January.

- Use payroll software alerts to cap contributions at 95% of the limit.

- Recharacterize excess amounts before the tax filing deadline.

Trap 2: Required Minimum Distribution Missteps

Post-2026 SECURE Act updates push the first RMD age to 75 for many savers. Missing deadlines incurs a 25% excise tax on the shortfall.

Hypothetical example: A 76-year-old with a $500,000 traditional 401(k) who skips a $18,500 RMD could lose $4,625 plus future compounding.

Trap 3: Asset Allocation Blunders

Sticking with outdated target-date funds after age 50 often leaves portfolios too aggressive or too conservative. Rebalancing once per year is essential under volatile 2026 market conditions.

Additional Traps 4–8

- Early withdrawal penalties before age 59½ without qualifying exceptions.

- Pro-rata rule violations during backdoor Roth conversions.

- Ignoring QCD rules for charitable giving after age 70½.

- Overlooking spousal beneficiary designations after divorce.

- Failing to update investment elections after job changes.

Pre- vs Post-2026 Penalty Impact Comparison

Before 2026 reforms, excess contribution penalties were 6% per year. After reforms, the IRS streamlined correction windows, reducing effective penalties to 3% if fixed within 60 days of discovery.

Step-by-Step Avoidance Strategies

1. Schedule quarterly account audits.

2. Consult a fiduciary advisor before any conversion.

3. Maintain a contribution calendar tied to paycheck dates.

FAQ: Recovery Options After Mistakes

Q: Can I recover from an RMD penalty? Yes—file Form 5329 and request a waiver with proof of reasonable cause.

Q: How do I fix excess Roth contributions? Withdraw the excess plus earnings by your tax deadline to avoid the 6% penalty.

Conclusion

Staying ahead of 2026 Roth IRA and 401(k) rules protects your retirement nest egg. Implement these preventive steps today to build a secure financial future.

No comments yet. Be the first!