Bullish Portfolio

Bullish Portfolio

What is the Mega Backdoor Roth Strategy?

The mega backdoor Roth is a powerful retirement savings hack that allows high-income earners to supercharge their Roth IRA contributions far beyond standard limits. Unlike traditional Roth IRA contributions, which cap at $7,000 annually ($8,000 if 50+ in 2025, likely similar in 2026), this strategy leverages after-tax contributions to your 401(k) plan, followed by an in-plan conversion or rollover to a Roth IRA.

Named 'mega' because it can enable contributions up to $46,500 or more in after-tax dollars (based on projected 2026 401(k) limits), it's ideal for those phased out of direct Roth IRA eligibility due to high income. With Roth assets growing tax-free forever and qualifying withdrawals tax-free in retirement, this hack is a game-changer for wealth building.

In 2026, expect the employee deferral limit to rise—potentially to $24,000 from 2025's $23,500—pushing total 401(k) contributions (including employer match and after-tax) even higher. This makes now the time to plan ahead.

Why Focus on 2026? Key Updates and Projections

Retirement plan limits adjust annually for inflation. For 2025, the total 401(k) contribution limit is $70,000 ($77,500 if 50+). In 2026, analysts project around $72,000–$75,000 total, with employee deferrals at $24,000+. After maxing pre-tax/Roth deferrals ($24,000) and employer match (say $10,000), you could add $38,000+ in after-tax contributions for mega backdoor conversion.

Recent laws like SECURE 2.0 expand Roth options, including automatic Roth treatment for employer contributions starting in 2026 for some plans. This enhances the strategy's appeal amid rising tax brackets and potential future tax hikes.

Eligibility Requirements for the Mega Backdoor Roth

Not every 401(k) plan supports this. Key criteria:

- Your Plan Allows After-Tax Contributions: Beyond pre-tax/Roth deferrals and employer contributions.

- In-Plan Roth Conversion Option: Immediate conversion within the 401(k) to a Roth bucket, avoiding pro-rata rule complications.

- Or In-Service Withdrawals: Permission to roll after-tax funds directly to a Roth IRA while still employed.

- Income Level: Best for those over Roth IRA phase-out ($161,000–$176,000 MAGI single in 2025; similar 2026), but anyone with eligible plan can use it.

- Age and Employment: Typically under 59½; must be employed with the plan sponsor.

Check your plan document or call HR. About 70% of large employer plans allow after-tax contributions per Vanguard data, but conversion features vary.

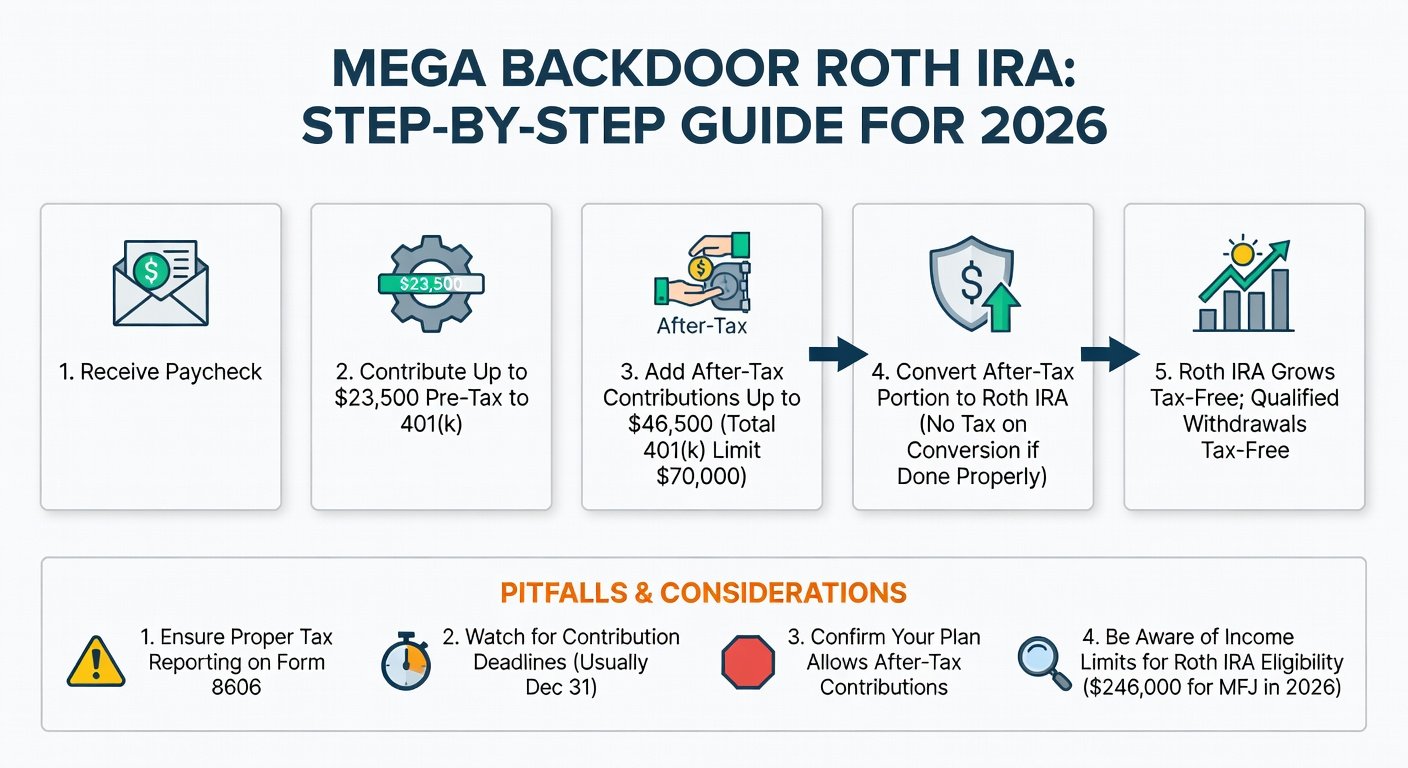

Step-by-Step Guide to Executing the Mega Backdoor Roth in 2026

Follow these precise steps for seamless execution:

- Verify Plan Features: Log into your 401(k) portal or contact administrator. Confirm after-tax contributions and Roth conversion/in-service withdrawal allowances. Reference IRS 401(k) guidance for rules.

- Max Out Pre-Tax/Roth Deferrals: Contribute up to $24,000 (projected 2026) via payroll. Include employer match.

- Initiate After-Tax Contributions: Elect after-tax via payroll—up to the total limit minus prior contributions. Example: $75,000 total limit - $24,000 deferral - $10,000 match = $41,000 after-tax.

- Convert Promptly: Quarterly or immediately if allowed. For in-plan: Convert to Roth 401(k). For rollover: Request in-service distribution of after-tax + earnings (minimal if quick).

- Handle Earnings: Small earnings on after-tax are taxable upon conversion. Convert frequently to minimize.

- Roll to Roth IRA (Optional): Once in Roth 401(k), roll to IRA for better investment choices upon job change or eligibility.

- Paperwork and Forms: Use plan forms; track basis on Form 8606 for taxes. Consult a tax pro.

Tax Advantages and Long-Term Growth Potential

The magic is tax-free compounding. After-tax contributions are post-tax dollars, but conversion basis is nontaxable (pro-rata applies if mixing). Earnings convert at ordinary rates but grow tax-free thereafter.

Key Benefits:

- No Income Limits: Bypass Roth IRA MAGI caps.

- Higher Limits: $40,000+ vs. $7,000 direct Roth.

- Tax Diversification: Balance taxable accounts with Roth.

- Flexibility: Roth withdrawals anytime tax/penalty-free after 59½ and 5-year rule.

See IRS Roth IRA details for rules. For high earners in 37% bracket, converting now locks in growth outside future hikes.

Real-World Examples: Crunching the Numbers for 2026

Example 1: Single Earner, $200k Salary

2026 Projections: Deferral $24,000 pre-tax; Employer match $12,000 (6%); After-tax $39,000 (to $75,000 total).

Convert $39,000 after-tax to Roth IRA. At 7% annual return, over 20 years: ~$150,000 tax-free.

Grows to millionaire status with consistency.

Example 2: Married Couple, Dual Incomes

One spouse: $45,000 after-tax mega. Other: Similar. Combined $90,000 Roth boost annually. In 10 years at 8%: Over $1.3M tax-free.

Use calculators from providers like Fidelity, but model conservatively. Compare to traditional 401(k): Roth wins if future rates rise.

Pros, Cons, and Common Mistakes to Avoid

Pros:

- Massive Roth conversion power.

- Investment freedom in IRAs.

- Hedge against tax increases.

Cons:

- Plan restrictions limit access.

- Upfront cash flow strain (after-tax).

- Illiquid until conversion.

Mistakes to Dodge:

- Pro-Rata Trap: Mixing pre-tax/after-tax without separate conversion. Solution: In-plan Roth only.

- Double Taxation: Forgetting to track basis. File Form 8606 yearly.

- Delayed Conversion: Earnings taxable; convert monthly/quarterly.

- Plan Change Risk: Job switch may block. Roll over promptly.

- Overlooking Fees: Check plan costs vs. IRA.

Consult a fiduciary advisor; review IRS Publication 590-A for contributions.

FAQs: Mega Backdoor Roth Answered

Q: Can self-employed use it? Solo 401(k)s often allow; check provider like Vanguard.

Q: What if my plan lacks features? Shop employers or advocate for changes.

Q: Impact on financial aid? Roth hurts less than taxable accounts.

Q: 2026 Limit Confirmation? Announced late 2025; adjust accordingly.

Conclusion: Supercharge Your Retirement in 2026

The mega backdoor Roth isn't for everyone, but for eligible high earners, it's a tax-efficient powerhouse. Start verifying your plan today, model scenarios, and position for limit increases. With disciplined execution, you'll harvest tax-free millions in retirement. Act now—consult professionals to tailor this hack to your situation and watch your wealth explode.

No comments yet. Be the first!