Bullish Portfolio

Bullish Portfolio

Introduction to Sustainable Retirement Planning in 2026

Retirement planning in 2026 increasingly incorporates environmental, social, and governance (ESG) principles alongside traditional financial goals. Environmentally conscious investors can align their Roth IRA and 401k accounts with sustainable funds to pursue long-term growth while supporting positive impact. This approach combines tax advantages with responsible investing, creating portfolios that reflect personal values without sacrificing potential returns. As climate concerns and corporate accountability gain prominence, more individuals are seeking ways to direct retirement savings toward companies demonstrating strong sustainability practices. This shift is supported by growing availability of ESG options across major brokerage platforms and employer-sponsored plans.

ESG integration has gained momentum as more plan sponsors and brokerage platforms expand their offerings. Investors now evaluate funds not only on historical performance but also on criteria like carbon footprint reduction and corporate governance standards. Understanding the mechanics of Roth IRAs and 401k plans is essential before making allocation decisions. Sustainable investing allows participants to address global challenges such as climate change and social equity while building wealth for retirement decades ahead.

Understanding Roth IRA and 401k Accounts for ESG Investing

A Roth IRA allows after-tax contributions with tax-free growth and qualified withdrawals, making it ideal for sustainable investments held over decades. In contrast, traditional 401k plans offer pre-tax contributions and tax-deferred growth, though many employers now provide ESG fund selections within their menus. Both vehicles support sustainable investing when participants choose appropriate options. The Roth structure particularly benefits long-term ESG holdings because qualified distributions avoid taxes on gains generated by responsible companies that may appreciate significantly over time.

Contribution limits and eligibility rules remain consistent regardless of investment style. Investors should verify their income eligibility for Roth contributions and review employer matching policies that may apply to ESG selections within a 401k. Employer matches represent free money that can accelerate portfolio growth when directed into high-quality sustainable funds. Additionally, Roth conversions from traditional accounts can be strategically timed to optimize tax outcomes when ESG assets are expected to perform well.

ESG Criteria and Their Role in Retirement Portfolios

ESG investing evaluates companies across three pillars: environmental factors such as emissions reduction and renewable energy adoption; social factors including labor practices and community engagement; and governance factors like board diversity and ethical leadership. Retirement accounts benefit when funds apply these screens to exclude controversial industries while favoring leaders in sustainability innovation. This methodology helps mitigate long-term risks associated with regulatory changes or reputational issues.

Investors can further refine selections by reviewing fund prospectuses that detail specific ESG methodologies. Some funds use negative screening to avoid fossil fuels, while others employ positive screening to overweight companies advancing clean technology. Combining both approaches within a diversified Roth IRA or 401k creates balanced exposure aligned with impact objectives.

Top Low-Fee ESG Fund Options for Retirement Accounts

Several low-cost ESG funds and ETFs are widely available in brokerage Roth IRAs and many 401k plans. Broad-market options tracking large-cap U.S. companies with strong ESG ratings provide diversification. International ESG funds add geographic exposure while emphasizing sustainability metrics. Investors often compare expense ratios and fund holdings before selecting. Platforms frequently highlight funds with expense ratios below industry averages, enabling more capital to compound over time. Reviewing the underlying index methodology helps ensure alignment with personal impact priorities.

Popular choices include ESG versions of total market or S&P 500 index funds that maintain broad diversification at minimal cost. Thematic funds focused on clean energy or water sustainability offer targeted impact but should be limited to smaller allocations to manage concentration risk. Always confirm share class availability within your specific plan to access the lowest-cost institutional versions.

Performance Comparisons: ESG vs Traditional Funds

Historical data shows that well-constructed ESG funds can deliver competitive returns relative to traditional benchmarks, though results vary by sector exposure and market conditions. In recent periods, certain ESG strategies have outperformed in technology and renewable energy sectors while lagging in traditional energy during commodity booms. Risk metrics such as volatility and drawdowns are often similar or slightly lower for ESG portfolios due to quality-oriented stock selection processes.

Long-term investors benefit from focusing on risk-adjusted metrics rather than short-term outperformance. Diversification across multiple ESG funds within Roth IRA and 401k accounts helps mitigate volatility associated with any single investment style. Comparing rolling returns over five- and ten-year periods provides clearer insight into consistency than single-year snapshots.

Allocation Strategies for Sustainable Retirement Portfolios

Effective allocation begins with assessing risk tolerance, time horizon, and impact objectives. Younger investors may tilt toward growth-oriented ESG equity funds, while those nearing retirement increase exposure to sustainable bond funds for income stability. A common framework involves core holdings in broad ESG index funds supplemented by satellite positions in thematic areas such as clean energy or gender-diversity leaders. Rebalancing annually maintains target allocations as market values fluctuate.

Target-date ESG funds offer a simplified glide path that automatically adjusts equity and fixed-income exposure over time while maintaining sustainability screens. For more customization, investors can build custom allocations using individual ETFs. Stress-testing allocations against various economic scenarios helps ensure the portfolio remains resilient through market cycles.

Practical Steps for Switching to ESG Investments

1. Review current account statements to identify existing holdings and their expense ratios.

2. Research ESG fund availability within your Roth IRA brokerage or 401k plan menu, paying close attention to share classes.

3. Compare expense ratios, holdings overlap, and historical tracking error against traditional counterparts.

4. Execute exchanges or contribution changes during open enrollment or at any time in a Roth IRA.

5. Monitor performance and impact reports quarterly, adjusting as needed to stay aligned with goals.

6. Document the rationale for each change to support future tax or performance reviews.

Consulting a fiduciary advisor familiar with sustainable investing can provide personalized guidance during the transition. Many advisors now hold credentials in ESG analysis that enhance their ability to evaluate fund quality.

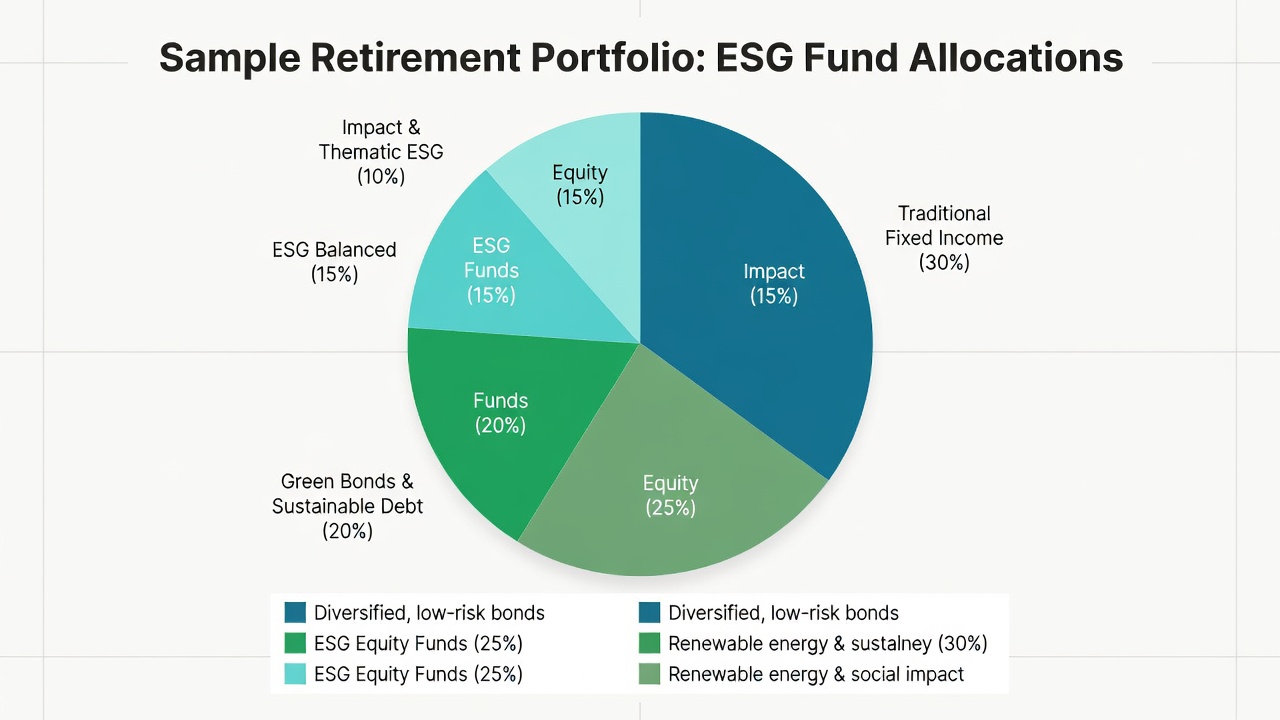

Real-World Portfolio Examples

Consider a 35-year-old investor allocating 70% to a broad U.S. ESG equity ETF, 20% to an international ESG fund, and 10% to a green bond ETF inside a Roth IRA. This mix balances growth potential with income generation and impact focus. Over a 30-year horizon, the equity tilt supports compounding while the bond allocation provides modest stability.

Another example involves a 50-year-old participant directing new 401k contributions 60% into a target-date ESG fund and 40% into an active sustainable large-cap strategy, gradually shifting toward fixed income as retirement approaches. A third scenario features a couple combining spousal Roth IRAs with complementary ESG tilts—one emphasizing climate solutions and the other focusing on social impact—to achieve broader diversification.

Mistakes to Avoid When Implementing ESG Strategies

Common pitfalls include over-concentrating in narrow thematic funds, ignoring fees that erode returns over decades, and failing to rebalance after market movements. Some investors also overlook tax implications of frequent trading within taxable accounts, though retirement vehicles largely avoid this issue. Another mistake is selecting funds based solely on marketing claims without verifying underlying holdings and methodology through independent sources.

Investors should also avoid abandoning traditional diversification principles in pursuit of impact. Maintaining appropriate equity-to-fixed-income ratios remains critical regardless of ESG focus. Regular education on evolving ESG standards prevents portfolios from becoming outdated.

FAQ: Tax Implications and Contribution Limits

What are the tax implications of ESG funds in Roth IRAs?

Qualified withdrawals from Roth IRAs remain tax-free regardless of whether gains come from ESG or traditional holdings, provided IRS rules are followed. Early withdrawals may incur penalties and taxes on earnings.

How do contribution limits apply in 2026?

Annual contribution limits are set by the IRS and apply uniformly across all investment types within Roth IRAs and 401k plans. Check official guidance at irs.gov for current-year details.

Can I transfer existing 401k assets to ESG options?

Most plans permit investment election changes at any time. Some allow in-plan Roth conversions, which carry specific tax consequences. Review plan documents or consult plan administrators for restrictions.

Are there any special tax benefits for ESG investments?

Tax treatment follows standard retirement account rules. ESG funds do not receive additional tax incentives beyond those available to all qualifying investments in Roth IRAs and 401k plans.

What resources can help verify ESG fund quality?

Authoritative sites such as sec.gov provide fund filings, while dol.gov offers guidance on fiduciary responsibilities for 401k plans.

Conclusion

Integrating ESG funds into Roth IRA and 401k accounts represents a forward-looking approach to 2026 retirement planning. By selecting low-fee sustainable options, comparing performance thoughtfully, and following structured allocation and switching processes, environmentally conscious investors can build portfolios that support both financial security and positive global impact. Regular review and adherence to tax guidelines ensure these strategies remain effective over the long term. Starting early with clear objectives maximizes the compounding benefits of sustainable investing aligned with personal values.

No comments yet. Be the first!