Bullish Portfolio

Bullish Portfolio

Introduction to REITs and Dividend Investing for Passive Income

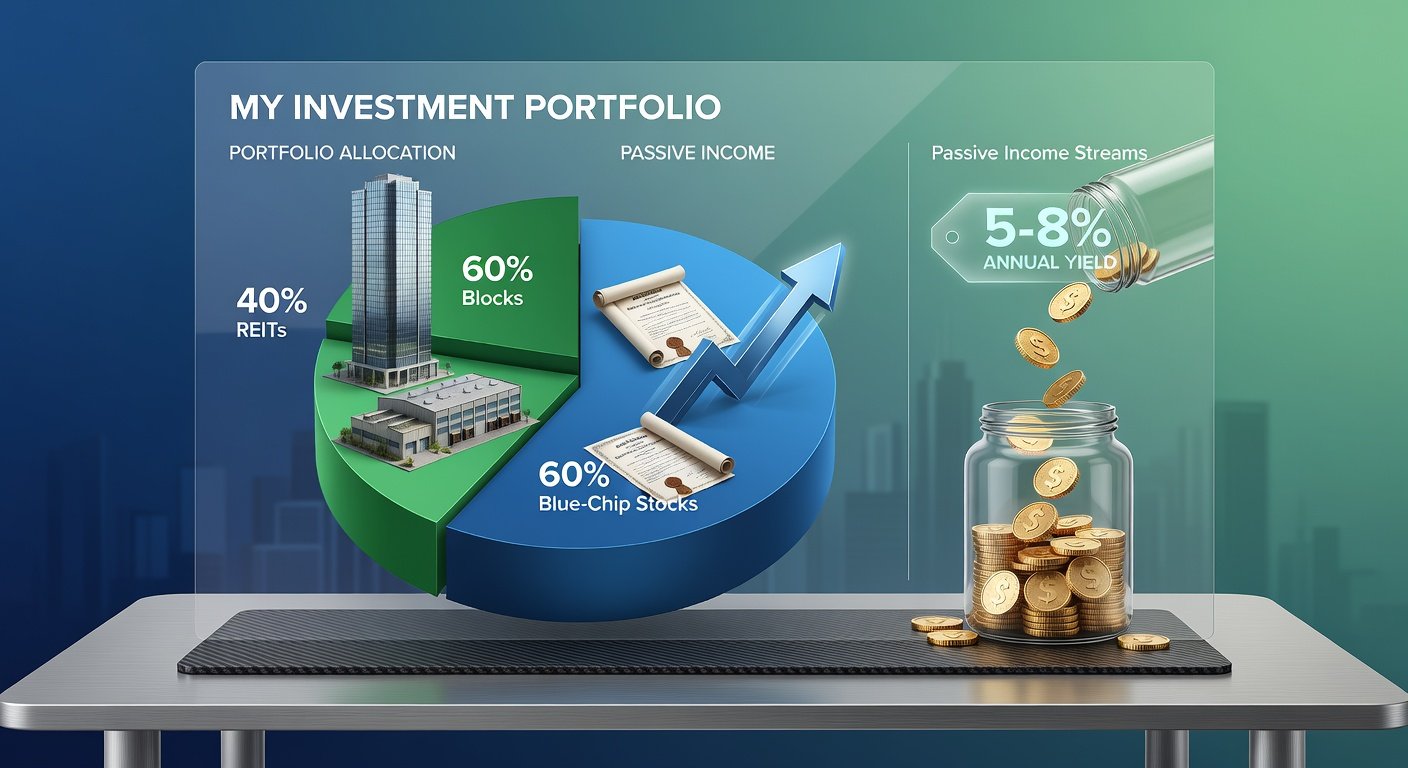

Building diversified passive income streams is a cornerstone of long-term wealth building. By combining Real Estate Investment Trusts (REITs) and dividend-paying stocks, investors can achieve steady cash flow with reduced risk. REITs offer exposure to real estate without property management hassles, while blue-chip dividend stocks provide stability from established companies. Together, they can yield 5-8% annually, ideal for 2026's market outlook.

This guide walks you through portfolio setup, selection criteria, rebalancing, tax advantages, and reinvestment strategies. Whether you're a beginner or optimizing your holdings, these steps will help you compound wealth efficiently.

Understanding REITs and Dividend Stocks

REITs are companies that own, operate, or finance income-generating real estate. They must distribute at least 90% of taxable income as dividends, making them high-yield favorites. Dividend stocks, especially blue-chips, are shares in mature firms like Procter & Gamble or Johnson & Johnson, known for consistent payouts and growth.

Combining them diversifies across asset classes: real estate hedges inflation, while stocks offer corporate earnings growth. A balanced portfolio might allocate 40% to REITs and 60% to dividends for optimal yield and stability.

Selection Criteria for High-Yield REITs

- Yield Threshold: Target REITs with 4-7% yields. Avoid ultra-high yields (>10%) signaling distress.

- Funds from Operations (FFO): Key metric over EPS; seek FFO payout ratios under 80% for sustainability.

- Diversification: Prefer REITs in multiple sectors like industrial, residential, and data centers (e.g., Prologis, Equity Residential).

- Balance Sheet Strength: Low debt-to-equity ratios (<50%) and investment-grade ratings.

- Track Record: 10+ years of dividend growth.

For authoritative REIT data, visit the National Association of REITs (NAREIT) homepage.

Selection Criteria for Blue-Chip Dividend Stocks

- Dividend Yield: 2-5% for safety; higher indicates risk.

- Payout Ratio: Under 60% to ensure reinvestment room.

- Dividend Growth: Aristocrats with 25+ years of increases (e.g., Coca-Cola, 3M).

- Moat and Earnings: Wide economic moats per Morningstar, consistent EPS growth.

- Sector Balance: Consumer staples, utilities, healthcare for defense.

Step-by-Step Portfolio Setup

- Assess Risk Tolerance: Conservative? 30% REITs, 70% dividends. Aggressive? 50/50.

- Open Brokerage Account: Use low-fee platforms like Vanguard or Fidelity.

- Initial Allocation: $100K example: $40K REITs (e.g., VNQ ETF), $60K dividends (e.g., SCHD ETF or VIG).

- Dollar-Cost Average: Invest monthly to mitigate timing risk.

- Monitor Yield: Aim for blended 5-8% (REITs boost, stocks stabilize).

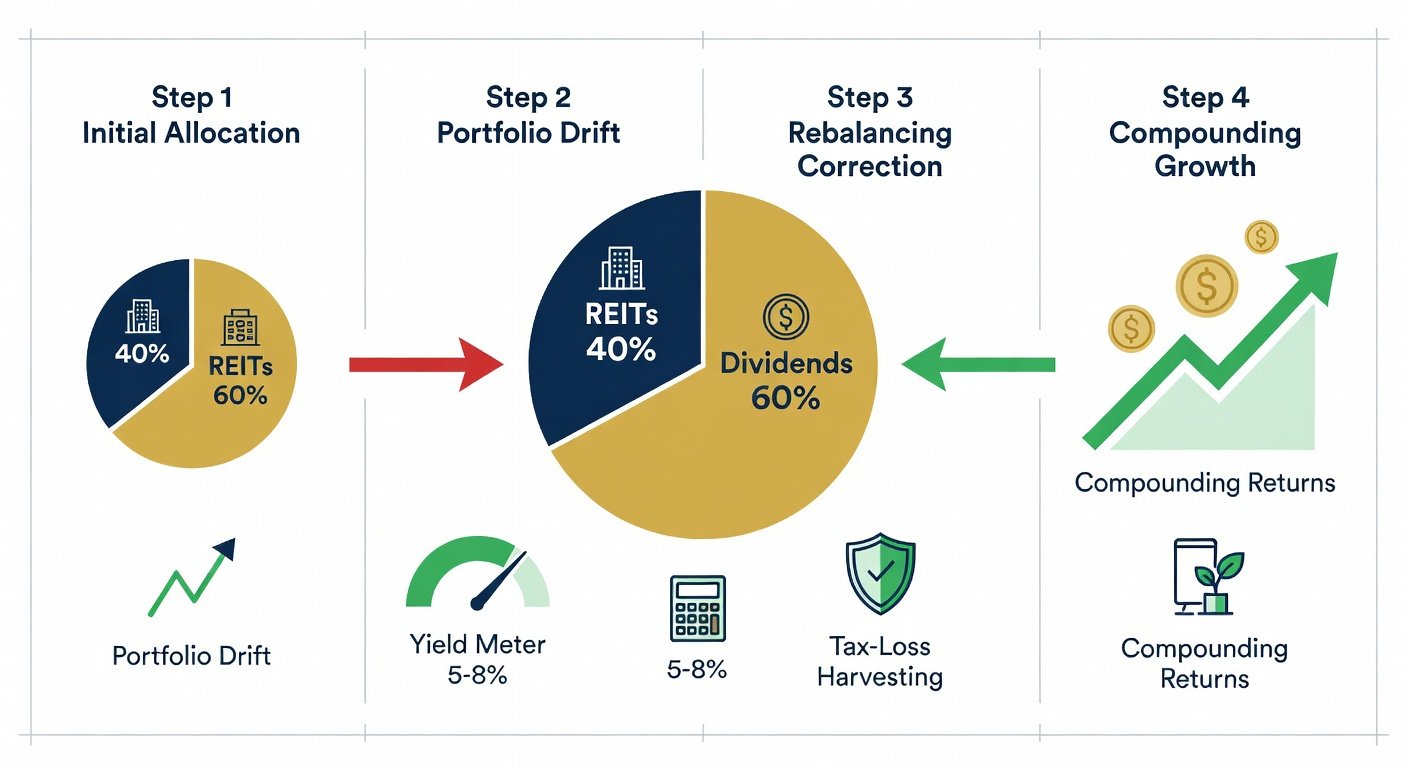

Rebalancing Techniques

Rebalancing maintains your target allocation, capturing gains and buying low. Quarterly or annual checks suffice.

- Threshold Method: Rebalance if any asset drifts >5% from target (e.g., REITs hit 45%, sell to 40%).

- Calendar Method: Annual review on your birthday.

- Tax-Efficient: Use new contributions or tax-advantaged accounts first.

- Tools: Excel spreadsheets or brokerage auto-rebalance features.

Example: If REITs grow to 50% due to property boom, trim 10% and buy dividend laggards.

Tax Advantages in 2026

REIT dividends are taxed as ordinary income but qualify for 20% QBI deduction if eligible. Qualified dividends from stocks get favorable long-term capital gains rates (0-20%). Use Roth IRAs for tax-free growth or 401(k)s for deferral.

Hold >1 year for lower rates. For details, consult the IRS website. In taxable accounts, REITs in MLPs or Opportunity Zones offer extra breaks.

Reinvestment Strategies for Compounding

DRIPs (Dividend Reinvestment Plans) automatically buy more shares, harnessing compounding. At 6% yield, $100K grows to $179K in 10 years (no taxes assumed).

- Full DRIP: 100% reinvest for max growth.

- Partial: Reinvest 70%, harvest 30% for income.

- 2026 Tip: With potential rate cuts, reinvest aggressively pre-hike.

- Track: Use apps like Personal Capital.

Formula: Future Value = P(1 + r/n)^(nt), where r=0.06, n=12 for monthly.

Real-World Portfolio Examples Yielding 5-8%

Example 1: Conservative ($100K)

40% Realty Income (O, 5.5% yield), 20% Prologis (PLD, 3.2%), 40% SCHD ETF (3.5%). Blended yield: 4.2%, total return ~7% historically.

Example 2: Balanced ($250K)

50% VNQ REIT ETF (4%), 30% Nozomi Dividend Achievers (VIG, 2%), 20% Utilities Select (XLU, 3.5%). Yield: 5.8%, low volatility.

Example 3: Growth-Focused ($500K)

30% Data Center REITs (e.g., Equinix, 2.5%), 40% Dividend Kings (e.g., Johnson & Johnson, 3%), 30% High-Yield Divs (e.g., Altria, 8%). Yield: 7.2%, inflation hedge.

Backtested via Portfolio Visualizer: These beat S&P 500 income with less drawdown. For SEC filings on ETFs, see SEC.gov.

Conclusion

Combining REITs and dividends creates resilient passive income for 2026 and beyond. Start small, select wisely, rebalance diligently, and let compounding work. Consult a financial advisor for personalization. Your path to financial freedom starts now.

No comments yet. Be the first!