Bullish Portfolio

Bullish Portfolio

Introduction to Tax-Efficient ETF Investing in 2026

Investors seeking growth with minimal tax drag are increasingly turning to exchange-traded funds (ETFs) for their inherent efficiencies. In 2026, understanding the tax differences between sector-specific ETFs and broad-market index funds can significantly impact long-term returns. This guide examines how these vehicles handle capital gains, turnover rates, and distributions while providing actionable strategies to optimize your portfolio.

Understanding ETF Taxation Basics

ETFs are generally more tax-efficient than mutual funds due to their in-kind creation and redemption mechanisms, which minimize taxable events. Both sector ETFs and broad index funds benefit from this structure, but differences arise in turnover and distribution patterns. The IRS treats ETF gains as either short-term or long-term capital gains depending on holding periods, with long-term rates applying after one year.

Sector ETFs vs. Broad Index Funds: Tax Efficiency Comparison

Broad index funds track large benchmarks like the S&P 500 and typically exhibit very low turnover, often below 5% annually. This results in fewer capital gains distributions. Sector ETFs, which focus on areas like technology, healthcare, or energy, may experience slightly higher turnover due to sector-specific rebalancing but still maintain lower turnover than actively managed funds. In 2026, sector ETFs can offer targeted exposure with comparable tax efficiency when selected carefully, especially those using optimized sampling techniques.

Key advantages of sector ETFs include the ability to tilt portfolios toward high-growth areas without triggering frequent sales. However, broad index funds often edge out in pure tax deferral because of their static composition. Investors should review prospectus details on historical distributions to compare performance.

Step-by-Step Strategies for Minimizing Tax Liabilities

Tax-Loss Harvesting

Tax-loss harvesting involves selling investments at a loss to offset gains. For ETF portfolios, implement this by swapping a sector ETF for a similar but not identical one (e.g., replacing a broad tech ETF with a semiconductor-focused alternative). Monitor wash-sale rules carefully to avoid disallowed losses. Perform reviews quarterly to capture opportunities throughout 2026.

Optimal Holding Periods

Hold ETFs for at least one year to qualify for preferential long-term capital gains rates. This strategy works well for both sector and index ETFs, allowing compounding without annual tax hits. Avoid frequent trading that could reclassify gains as short-term.

Account Placement Decisions

Place higher-turnover sector ETFs in tax-advantaged accounts like IRAs or 401(k)s to shield distributions. Reserve broad index funds for taxable brokerage accounts where their low turnover shines. This asset-location approach can reduce overall tax exposure by 15-30% depending on your bracket.

Additional tactics include using ETFs with low expense ratios and avoiding those with high dividend yields in taxable accounts unless offset by losses.

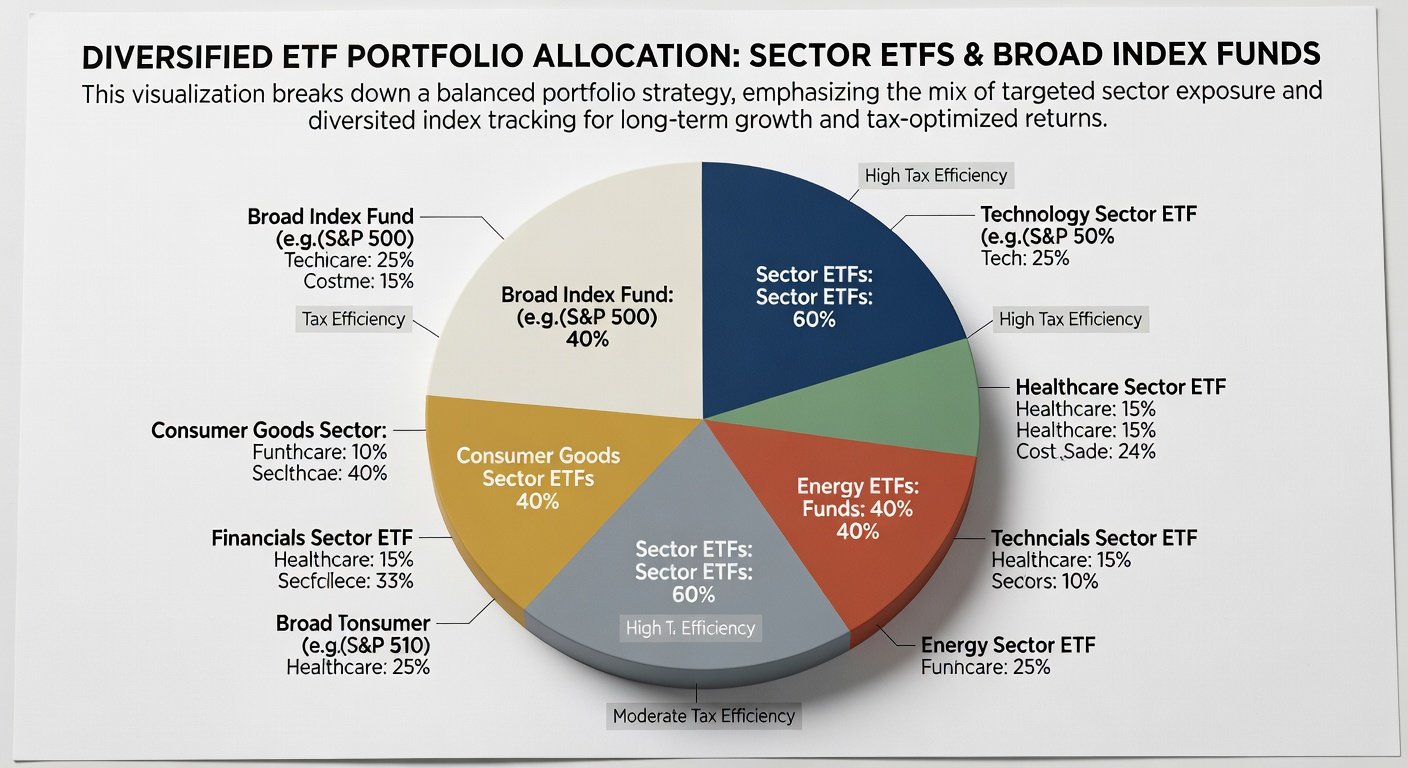

Sample Diversified Portfolio for Tax-Smart Growth

Here's a balanced 2026 example allocation blending sector ETFs and index funds:

- 40% Broad S&P 500 Index ETF – Core low-turnover holding for market exposure

- 20% Technology Sector ETF – Growth tilt with selective rebalancing

- 15% Healthcare Sector ETF – Defensive sector balance

- 15% Total International Index ETF – Global diversification

- 10% Energy Sector ETF – Inflation hedge component

Rebalance annually using new contributions rather than selling to minimize triggers. This mix targets growth while prioritizing tax efficiency through strategic placement.

Common Mistakes to Avoid

- Over-trading sector ETFs, which increases short-term gains exposure.

- Ignoring expense ratios that erode after-tax returns over time.

- Failing to coordinate harvesting across multiple accounts.

Conclusion

Tax-efficient ETF investing in 2026 requires deliberate choices between sector and index vehicles. By applying tax-loss harvesting, respecting holding periods, and optimizing account placement, investors can build resilient portfolios that grow with reduced IRS impact. Consult a tax professional for personalized implementation tailored to your situation.

No comments yet. Be the first!