Bullish Portfolio

Bullish Portfolio

Introduction: Planning for Healthcare in Retirement

Rising medical expenses represent one of the largest financial challenges for retirees. Effective use of Roth IRA and 401(k) accounts can help manage these costs while preserving tax advantages and account growth. This guide explores practical approaches for 2026, focusing on tax-efficient strategies that align with Medicare and out-of-pocket needs. Healthcare costs often increase with age due to chronic conditions, prescriptions, and long-term care. Strategic planning involves projecting lifetime needs, timing withdrawals, and leveraging tax-free distributions where possible. Retirees who fail to plan adequately may face depleted savings or forced lifestyle changes. By integrating Roth and traditional accounts thoughtfully, individuals can create a resilient financial buffer against unpredictable medical bills.

Projecting Lifetime Healthcare Needs

Estimating future medical expenses starts with reviewing personal health history, family medical background, and expected longevity. Tools from government agencies provide benchmarks for planning. Consider factors like inflation in medical costs and potential gaps in coverage. A step-by-step approach includes assessing current insurance, factoring in Medicare premiums and deductibles, and modeling scenarios for unexpected expenses. This projection informs how much to allocate from retirement accounts versus other sources. Variables such as geographic location, lifestyle choices, and genetic predispositions also play significant roles. For instance, individuals with a family history of heart disease may need to budget higher amounts for cardiology-related care. Regular updates to these projections every few years ensure the plan remains realistic as health and regulations evolve.

Tax-Efficient Withdrawal Sequences

Coordinating withdrawals from traditional 401(k)s, Roth IRAs, and taxable accounts minimizes tax impact. A common sequence begins with required minimum distributions from pre-tax accounts, followed by strategic Roth conversions in lower-income years, and finally tax-free Roth distributions for healthcare. This method helps manage Medicare premium surcharges tied to income. Delaying Social Security can also create a window for tax-efficient conversions. Additional considerations include the impact of capital gains on taxable accounts and the timing of qualified charitable distributions. Retirees should map out multi-year cash flow projections to avoid bracket creep. Working with a tax professional can reveal opportunities to bunch deductions or time large medical payments strategically.

Using Roth Tax-Free Distributions Strategively

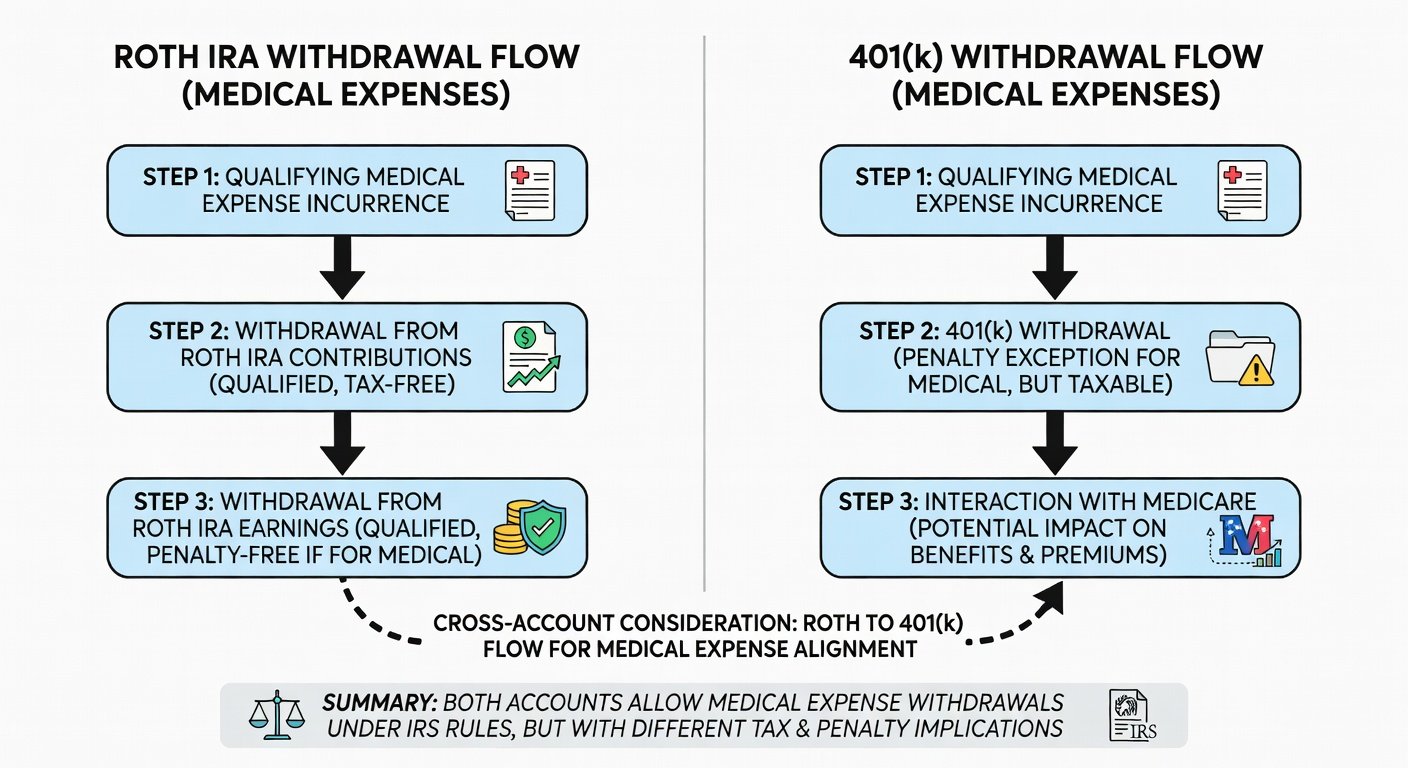

Roth IRA qualified distributions for medical expenses offer flexibility since they are tax-free. Withdrawals can cover premiums, deductibles, copays, and even certain long-term care costs without increasing taxable income. Unlike traditional accounts, Roth contributions can be withdrawn penalty-free at any time, providing liquidity for immediate healthcare needs while earnings grow tax-free. This feature proves especially valuable during the early retirement years before Medicare eligibility. Account owners should maintain detailed records of contributions versus earnings to optimize tax-free access. Roth accounts also serve as powerful inheritance vehicles, allowing heirs to receive tax-free distributions for their own medical needs.

401(k) Hardship Provisions for Medical Costs

Many 401(k) plans allow hardship withdrawals for medical expenses exceeding 7.5% of adjusted gross income. These distributions may avoid the 10% early withdrawal penalty if used for qualified medical costs, though income taxes still apply. Review plan documents carefully, as not all plans permit hardship distributions. Alternatives like plan loans should be considered first to avoid permanent account reduction. When hardship withdrawals become necessary, retirees must document expenses thoroughly to satisfy IRS requirements. Some plans impose additional restrictions or waiting periods that can affect timing. Exploring rollover options into an IRA before withdrawal may provide greater flexibility in certain situations.

Medicare Coordination and Account Strategies

Medicare Parts A, B, and D interact with retirement account withdrawals through income-related monthly adjustment amounts. Keeping modified adjusted gross income below certain thresholds preserves lower premiums. Health Savings Accounts paired with high-deductible plans can bridge to Medicare, offering triple tax advantages that complement Roth strategies.

2026 Contribution Tactics to Preserve Growth

Maximizing contributions to Roth accounts when eligible allows tax-free growth for future healthcare needs. Catch-up contributions for those age 50 and older further accelerate savings. Consider backdoor Roth strategies if income limits apply. Rebalancing portfolios within these accounts toward conservative allocations as retirement nears helps protect against market volatility that could impact healthcare funding. Spousal IRA contributions and employer matching opportunities should be fully utilized before focusing on after-tax savings vehicles. Annual reviews of contribution limits and eligibility rules prevent missed opportunities.

Real-Life Case Studies

Consider a couple in their early 60s who used Roth conversions during a low-income period to fund future medical expenses tax-free. They converted just enough each year to stay below Medicare surcharge thresholds, building a substantial Roth balance that later covered assisted living costs without tax consequences. Another example involves a retiree leveraging 401(k) hardship withdrawals to cover unexpected surgery costs while maintaining Medicare coordination. This individual documented all expenses meticulously and combined the withdrawal with HSA funds to minimize overall tax impact. Both cases demonstrate the value of proactive planning and professional guidance tailored to specific health and financial profiles.

Step-by-Step Calculators and Planning Tools

Begin by estimating annual healthcare needs using online calculators from authoritative sources. Next, model withdrawal impacts on taxes and Medicare premiums. Finally, adjust contribution levels annually based on updated limits and personal goals. Useful steps include reviewing current account balances and projected growth rates, simulating different withdrawal sequences over 20-30 years, factoring in inflation and potential healthcare cost increases, and consulting tax software or advisors for personalized projections. Spreadsheet templates that incorporate Medicare brackets and Roth ordering rules can simplify the process significantly.

Mistakes to Avoid in Healthcare-Focused Retirement Planning

Common errors include ignoring the long-term effects of required minimum distributions on Medicare premiums and overlooking the value of Roth conversions in early retirement years. Another frequent mistake is failing to maintain adequate liquidity outside retirement accounts, forcing taxable withdrawals during high-medical-cost periods. Retirees should also avoid over-concentrating in employer stock within 401(k)s, which increases both market and healthcare funding risk.

Frequently Asked Questions

When should I start Roth conversions for healthcare planning?

Many begin in the years between retirement and claiming Social Security to take advantage of lower tax brackets and avoid future Medicare surcharges.

Can I use 401(k) funds for long-term care?

Yes, but consider tax implications and explore whether Roth conversions or HSA funds provide better outcomes before tapping pre-tax accounts.

What pitfalls should I avoid with timing?

Withdrawing too early can trigger penalties and reduce compound growth; delaying too long may increase Medicare costs and limit flexibility.

How do HSAs fit into a Roth and 401(k) strategy?

HSAs offer tax-free withdrawals for medical expenses and can serve as a bridge account until Medicare begins, complementing Roth tax-free growth.

Conclusion

Integrating Roth IRA and 401(k) strategies with Medicare planning provides a robust framework for managing 2026 healthcare costs in retirement. Start with detailed projections, implement tax-efficient sequences, and review plans regularly with qualified professionals. Authoritative resources such as the IRS, Medicare.gov, and Social Security Administration offer additional guidance to refine your approach and ensure long-term financial security.

No comments yet. Be the first!