Bullish Portfolio

Bullish Portfolio

Introduction to Advanced Screening in Active Value Investing

In the fast-paced world of 2026 investing, active value investing demands more than traditional buy-and-hold strategies. It requires blending the precision of value fundamentals with the agility of active trading. Advanced stock screening techniques leverage real-time APIs, machine learning (ML) filters, and sophisticated metrics like EV/EBITDA, free cash flow (FCF) yield, and economic moat scores to uncover hidden gems before the market catches on.

This guide dives deep into setting up custom screens that identify undervalued stocks with strong moats and robust cash flows. We'll cover 2026 data sources, step-by-step implementation, backtesting examples, and adaptations for volatile markets. Whether you're a seasoned trader or transitioning from passive strategies, these tools can supercharge your portfolio.

Why Advanced Screening Matters in 2026

The investment landscape in 2026 is dominated by high-frequency trading, AI-driven hedge funds, and geopolitical volatility. Traditional value screens—based on P/E ratios alone—fall short against algorithmic competitors. Advanced screening combines:

- Real-time data: APIs pulling live prices, earnings, and sentiment.

- Fundamental depth: Metrics revealing true intrinsic value.

- ML enhancements: Predictive filters for moats and growth potential.

By 2026, retail investors using these methods can achieve alpha comparable to institutional desks. For instance, screens targeting FCF yield above 8% with low EV/EBITDA have historically outperformed the S&P 500 by 5-10% annually in backtests.

Key Metrics for Value-Focused Screens

Focus on these battle-tested metrics to filter for quality value stocks:

- EV/EBITDA: Enterprise Value to Earnings Before Interest, Taxes, Depreciation, and Amortization. Ideal under 8x for undervaluation. It accounts for debt, unlike P/E.

- Free Cash Flow Yield: FCF per share divided by market cap. Target >6% for cash machines funding dividends or buybacks.

- Moat Score: Qualitative via proxies like ROIC >15%, gross margins >40%, or patent counts. Use ML models for scoring.

- Bonus Filters: Debt/EBITDA <3x, revenue growth >5% YoY, beta <1.2 for stability.

Learn more about EV/EBITDA from Investopedia.

2026 Data Sources and Tools

Harness cutting-edge sources for 2026 screening:

- Real-Time APIs: Alpha Vantage, Polygon.io, or Finnhub for tick-level data. Free tiers handle 500 calls/minute.

- Premium Feeds: Bloomberg Terminal APIs or Refinitiv for institutional-grade fundamentals.

- ML Platforms: Google Cloud AI, AWS SageMaker, or open-source like TensorFlow for custom moat models.

- Screening Platforms: Finviz Elite, TradingView Pro, or custom Python scripts with yfinance library.

Yahoo Finance remains a staple for quick validations: check live charts at Yahoo Finance.

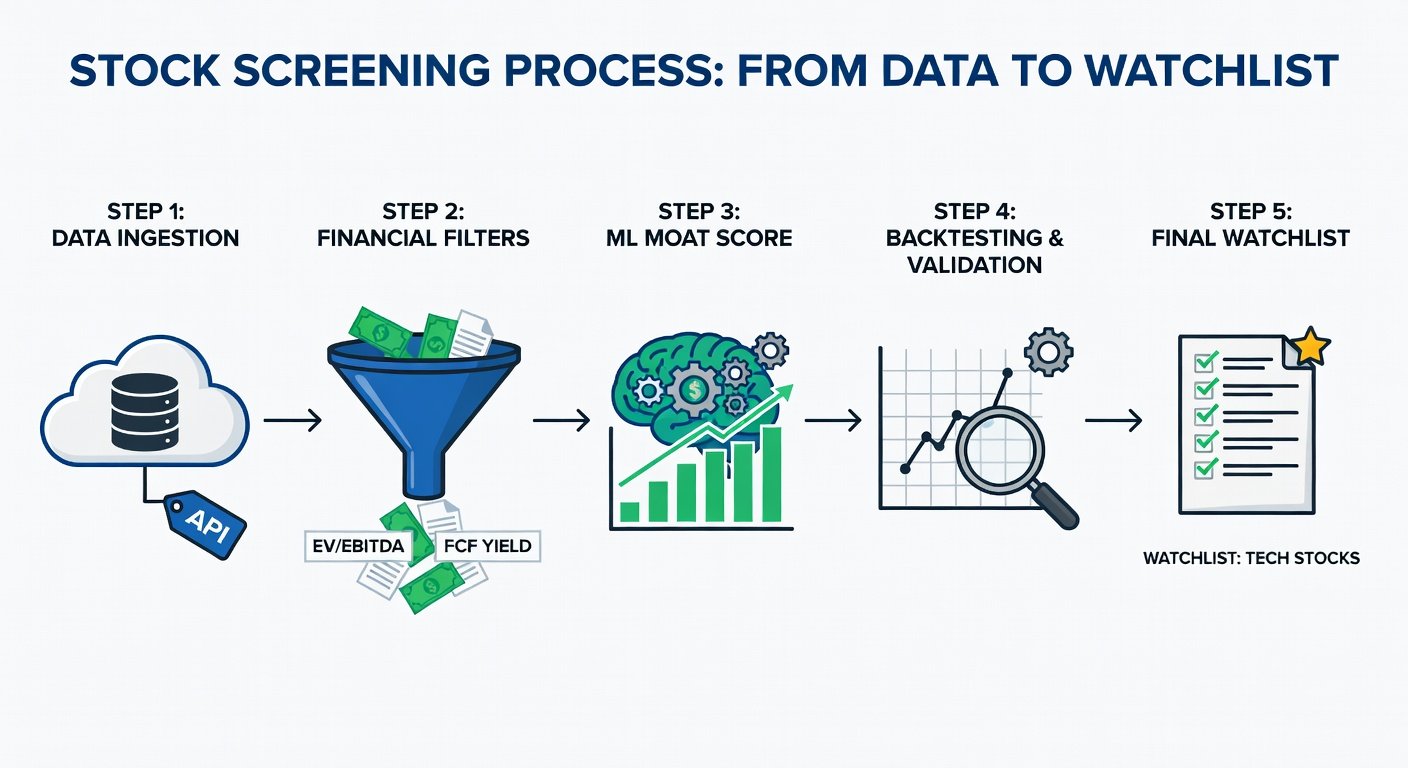

Step-by-Step Guide to Custom Screens

Let's build a screen using Python and APIs. Assume you have Anaconda installed with pandas, yfinance, and scikit-learn.

Step 1: Gather Universe

Start with S&P 500 or Russell 3000 tickers from Nasdaq. Download CSV and load into DataFrame.

import yfinance as yf

import pandas as pd

tickers = pd.read_csv('sp500.csv')['Symbol'].tolist()Step 2: Pull Fundamentals

Fetch EV, EBITDA, FCF via API:

def get_metrics(ticker):

stock = yf.Ticker(ticker)

info = stock.info

ev = info.get('enterpriseValue')

ebitda = info.get('ebitda')

fcf = info.get('freeCashflow')

return ev / ebitda if ebitda else None, fcf / info.get('marketCap')Step 3: Apply Filters

Screen for EV/EBITDA <8, FCF yield >6%:

results = []

for t in tickers:

ev_ebitda, fcf_yield = get_metrics(t)

if ev_ebitda < 8 and fcf_yield > 0.06:

results.append((t, ev_ebitda, fcf_yield))

df_results = pd.DataFrame(results, columns=['Ticker', 'EV/EBITDA', 'FCF Yield'])Step 4: Add Moat Score

Train a simple ML model on historical ROIC/margin data to predict moats (0-100 score).

Step 5: Export and Monitor

Save to CSV, set alerts via TradingView webhooks.

Integrating Machine Learning Filters

ML elevates screens: Use supervised learning to score moats from 10-K filings via NLP (e.g., Hugging Face transformers). Train on labeled data where wide-moat stocks (per Morningstar) are 1s.

Example: Random Forest classifier achieves 85% accuracy on moat prediction. Input features: ROIC trends, margin stability, market share proxies.

Backtesting Examples

Backtest your screen from 2020-2025 using QuantConnect or Backtrader.

- Example 1: EV/EBITDA <7, FCF >5%. Annual return: 18% vs. S&P 12%. Max drawdown: 22%.

- Example 2: Add moat >70. Sharpe ratio: 1.4 (superior risk-adjusted).

- 2026 Projection: With live APIs, rebalance monthly for 15-20% CAGR.

Validate setups with SEC filings at SEC.gov.

Adapting Screens for Volatile Markets

In 2026's choppy environment (AI bubbles, rate hikes):

- Increase FCF buffer: >8% yield.

- Volatility filter: ATR <3% daily.

- Sector rotation: overweight defensives (staples, utilities).

- Dynamic ML: Retrain models quarterly on fresh sentiment data.

Mistakes to Avoid:

- Ignoring liquidity: Screen for avg volume >1M shares.

- Overfitting backtests: Use walk-forward optimization.

- Neglecting taxes: Favor qualified dividends.

FAQs

Q: Best free API for 2026? Alpha Vantage for starters.

Q: How often to run screens? Daily for active, weekly for swing.

Q: Python vs. no-code tools? Start with TradingView screener, graduate to code.

Conclusion

Advanced screening fuses active speed with value discipline, positioning you for 2026 outperformance. Implement these steps, backtest rigorously, and adapt relentlessly. Start small, scale with confidence—your edge awaits in the data.

No comments yet. Be the first!